Rule 86A survives because fake-credit fraud is real. But recent courts are insisting that electronic credit ledger blocks rest on recorded material, temporal discipline, and statutory limits.

The freeze that changes the cash cycle

Rule 86A blocking of ITC has become one of GST’s sharpest revenue tools because it bites before final adjudication does. A search, a failed verification, a suspicious supplier trail, and the taxpayer’s electronic credit ledger can suddenly become unusable for output tax or refund claims. For enforcement officers, that speed matters. For business, it means working capital is repriced overnight. The Delhi High Court in Best Crop Science noted that blocking ITC materially reduces working capital and is not a recovery provision in the ordinary assessment architecture. That is why the present judicial trend matters. The dispute is no longer about whether Rule 86A can exist. It is about whether a preventive power can be used as a substitute for proof.

Why the State still wants Rule 86A

The enforcement backdrop is real, not performative. Recent official releases continue to show large fake-invoice and fraudulent ITC cases, including a March 2026 Delhi South case involving alleged fraudulent ITC of Rs 60.59 crore through bogus invoices of Rs 397.23 crore, and a November 2025 DGGI Delhi case alleging fraudulent ITC of Rs 645 crore through dummy firms. Rule 86A sits inside that anti-fraud logic. Inserted in December 2019, it allows the Commissioner or an authorised officer not below Assistant Commissioner rank to disallow debit of an amount equivalent to credit available in the electronic credit ledger where there are reasons to believe that the credit has been fraudulently availed or is ineligible on specified grounds. The 2021 Board guidelines preserve that power, but they also narrow its proper use: it is extraordinary, it must not be exercised mechanically, and it must rest on material evidence.

The move from suspicion to record

That last point is where courts are pushing hardest. The 2021 guidelines say the officer must apply his mind, record reasons in writing, and use the remedy with utmost circumspection. They also recognise that a block affects working capital and urge investigation and adjudication to be completed within the restriction period. Once the administration has written that much into its own framework, a template-driven Rule 86A order becomes difficult to defend. Taxpayers are not winning merely by objecting to a ledger freeze. They are winning when they show that the file does not disclose a real nexus between the material gathered and the debit restriction imposed.

Where the courts have tightened fastest

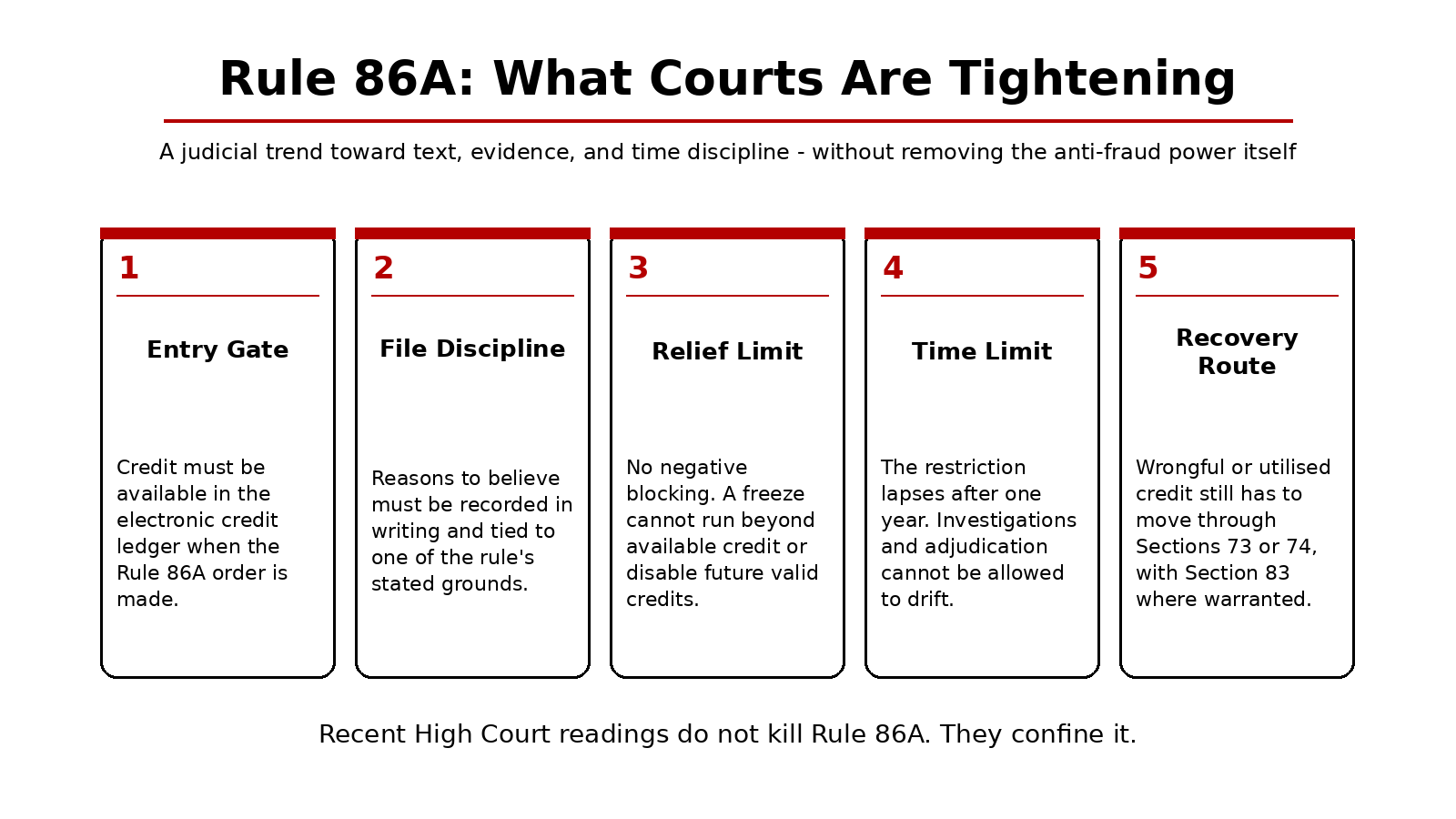

The sharpest restraint has come on so-called negative blocking. In September 2024, the Delhi High Court in Best Crop Science held that Rule 86A is an emergent measure and does not require a prior show-cause notice, but it can operate only against ITC actually available in the electronic credit ledger at the time of the blocking order. It is not a machinery provision for recovery, and it cannot be stretched to force a taxpayer to replenish past credit by disabling future valid credits. If tainted credit has already been used, the recovery route lies through adjudication under Sections 73 or 74, and where needed, provisional attachment under Section 83. In October 2025, the Bombay High Court repeated the same textual discipline, calling the power “extremely harsh in nature” and stressing that strict statutory language must govern its use. The same judgment records that the Supreme Court, on 9 July 2025, declined to interfere with the Delhi High Court’s Karuna Rajendra Ringshia order, while leaving other recovery remedies open.

But restraint is not repeal

The jurisprudence is still not perfectly uniform, and that should temper the confidence of both taxpayers and officers. The Bombay High Court itself noted that the Calcutta High Court had taken a different view in Basanta Kumar Shaw. In July 2025, the Madhya Pradesh High Court also refused to treat Rule 86A as constitutionally suspect. It accepted the logic that the rule authorises immediate protective action and that sub-rule (2) provides a post-decisional route for objections. That is the balanced reading of the present moment. Courts are narrowing abuse, not disarming the administration in genuine fraud cases. Where the record points to non-existent suppliers, paper-only transactions, or missing primary documents, writ courts remain cautious.

The one-year sunset now matters

Sub-rule (3), which says the restriction ceases after one year, is no longer a drafting footnote. The Delhi High Court read that limit seriously. So do the 2021 guidelines, which urge investigation and adjudication to be completed well within the restriction period. That changes the economics of administration. Rule 86A works best as a short-burst protective device, not as a lazy substitute for a completed case file. Once the one-year discipline is taken seriously, departments have to move from portal control to evidentiary closure. That is healthy for GST’s self-assessment architecture. Exceptional freezes cannot become a quasi-permanent fiscal instrument.

What a stronger Rule 86A case now looks like

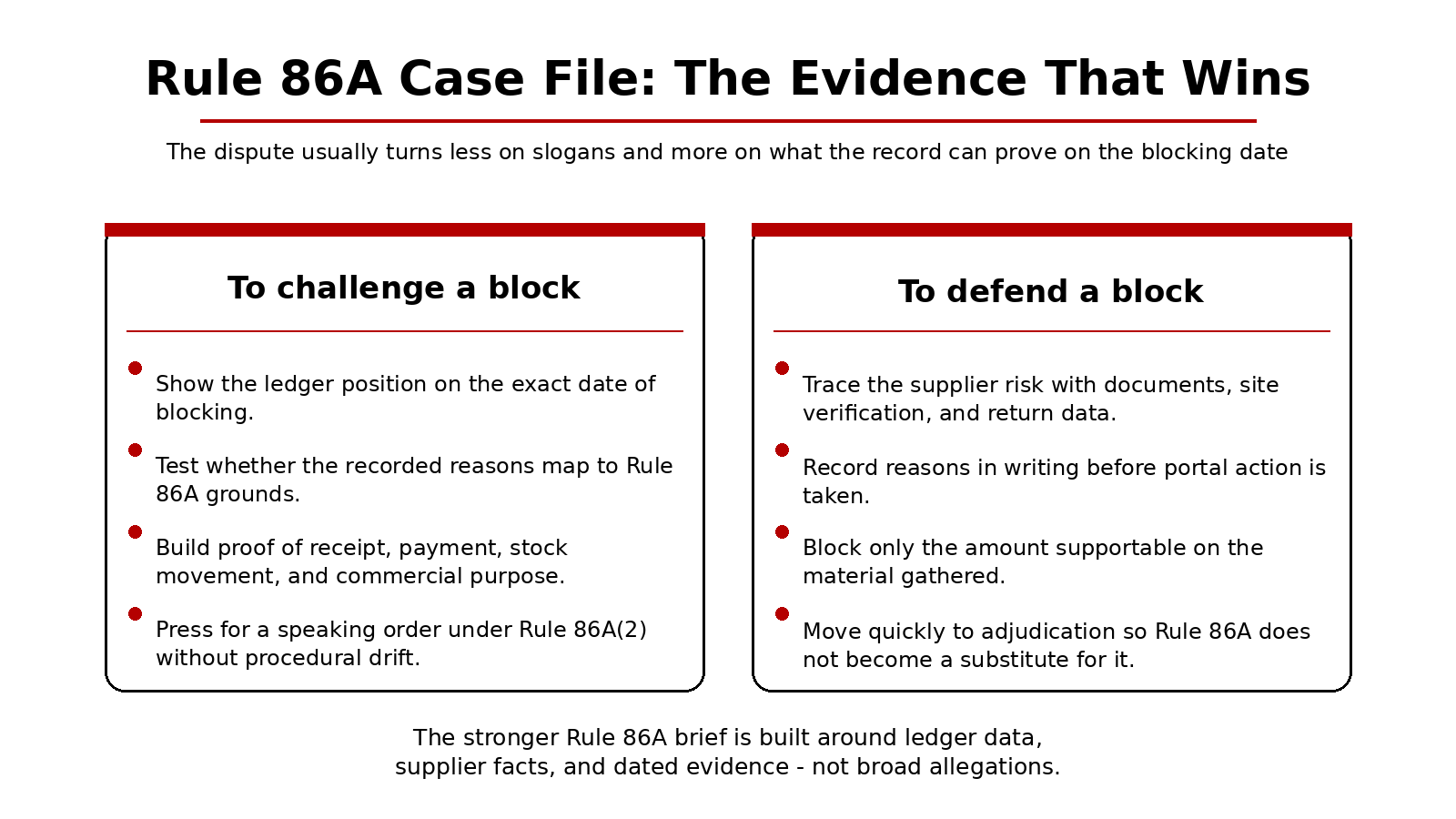

For taxpayers and counsel, the better Rule 86A challenge in 2026 is evidentiary, not rhetorical. What exact material existed on the date of blocking? Did that material map onto one of Rule 86A’s stated grounds, or was it merely ecosystem suspicion around a supplier? How much credit was actually available in the ledger when the order was made? Were objections under Rule 86A(2) decided through a speaking order, or did the matter just drift while working capital stayed frozen? This is where GST litigation now overlaps with documentation discipline: proof of receipt, payment trail, stock movement, GSTR-2B reconciliation, vendor verification, and commercial correspondence.

Why finance teams should care

The second-order effects run beyond the litigating taxpayer. A blocked ledger raises compliance friction for the entire supply chain. Treasury has to fund tax in cash where credit was expected to do the job. Smaller vendors face delayed settlements because the recipient’s cash cycle worsens. Advisers must spend more time on supplier hygiene and fast-response representations. For the middle class, the effect is indirect but real: higher operating costs, delayed projects, and thinner margins being pushed into prices where market power allows. Rule 86A therefore sits at an uncomfortable junction of anti-fraud policy and tax incidence. If used well, it protects the base. If used badly, it taxes liquidity before liability is determined.

The judicial message

The most sensible reading of the recent trend is that Rule 86A will survive precisely because courts are forcing it back into a narrower lane. The administration has enough statutory weapons against fake credit. What courts appear unwilling to tolerate is a ledger freeze unsupported by recorded reasons, disconnected from the amount actually available, or left hanging without adjudicatory follow-through. That is not judicial softness. It is institutional discipline. For a tax built on input-credit continuity and self-reporting trust, that restraint is not a concession to taxpayers. It is the condition for the system’s legitimacy.

Sources & Data Points

- Rule 86A, Central Goods and Services Tax Rules, 2017 (official CBIC tax repository). Official link

- Guidelines for disallowing debit of electronic credit ledger under Rule 86A, GST Policy Wing, 2 November 2021. Official PDF

- Instruction No. 02/2024-GST dated 12 August 2024 on action against non-existent or suspicious GST registrations. Official PDF

- Best Crop Science Pvt Ltd through Authorised Representative v. Principal Commissioner, CGST Commissionerate, Meerut & Ors., Delhi High Court, 24 September 2024. Official judgment link

- Rawman Metal & Alloys v. Deputy Commissioner of State Tax, Bombay High Court, 7 October 2025. Official judgment link

- M/s Steel Centre v. Union of India & Others, Madhya Pradesh High Court, 25 July 2025. Official judgment link

- PIB release: CGST Delhi South Commissionerate arrests director for alleged fraudulent ITC of Rs 60.59 crore through bogus invoices of Rs 397.23 crore, 9 March 2026. Official release

- PIB release: DGGI Delhi Zonal Unit uncovers alleged fraudulent ITC of Rs 645 crore through dummy firms, 13 November 2025. Official release

Note: No article claim here relies on unpublished aggregate data for Rule 86A blocks; the piece stays within officially available rule text, instructions, judgments, and government releases.