A 30-day IRP cutoff promises cleaner invoice trails and faster fraud detection, but it also turns delayed approvals, credit-note timing and ERP gaps into genuine tax risk.

Why the e-invoice 30 day rule is tighter than it first looks

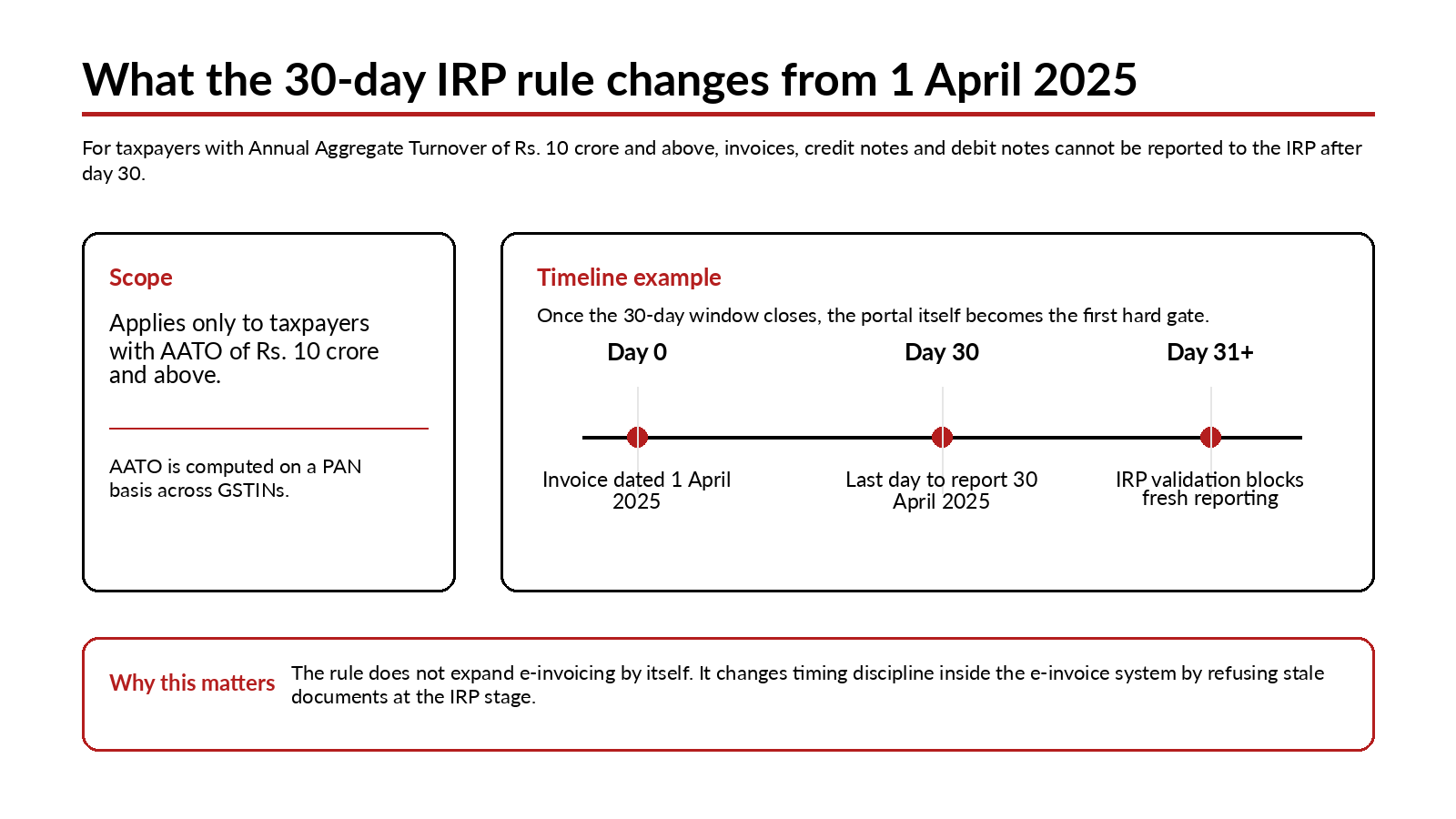

e-invoice 30 day rule has turned what used to be an untidy back-office habit into a hard tax deadline. In many firms, invoices do not fail because tax teams do not know the law. They fail because dispatch confirmations, customer sign-offs, rate approvals or credit-note mapping arrive late. From 1 April 2025, that lag stopped being administrative slack for businesses with Annual Aggregate Turnover, or AATO, of Rs. 10 crore and above. Once day 30 passes, the IRP itself refuses registration of the document. That changes the economics of delay.

The design point matters. Mandatory e-invoicing itself already reaches businesses with turnover above Rs. 5 crore from 1 August 2023, but the 30-day reporting lock is narrower: it applies only to taxpayers with AATO of Rs. 10 crore and above, and it covers invoices, credit notes and debit notes for which an IRN is required. AATO is computed on a PAN basis across GSTINs using return data. So this is not a broad expansion of the e-invoice net. It is a timeliness intervention inside an already digitalised segment.

Why the state wants a faster IRP clock

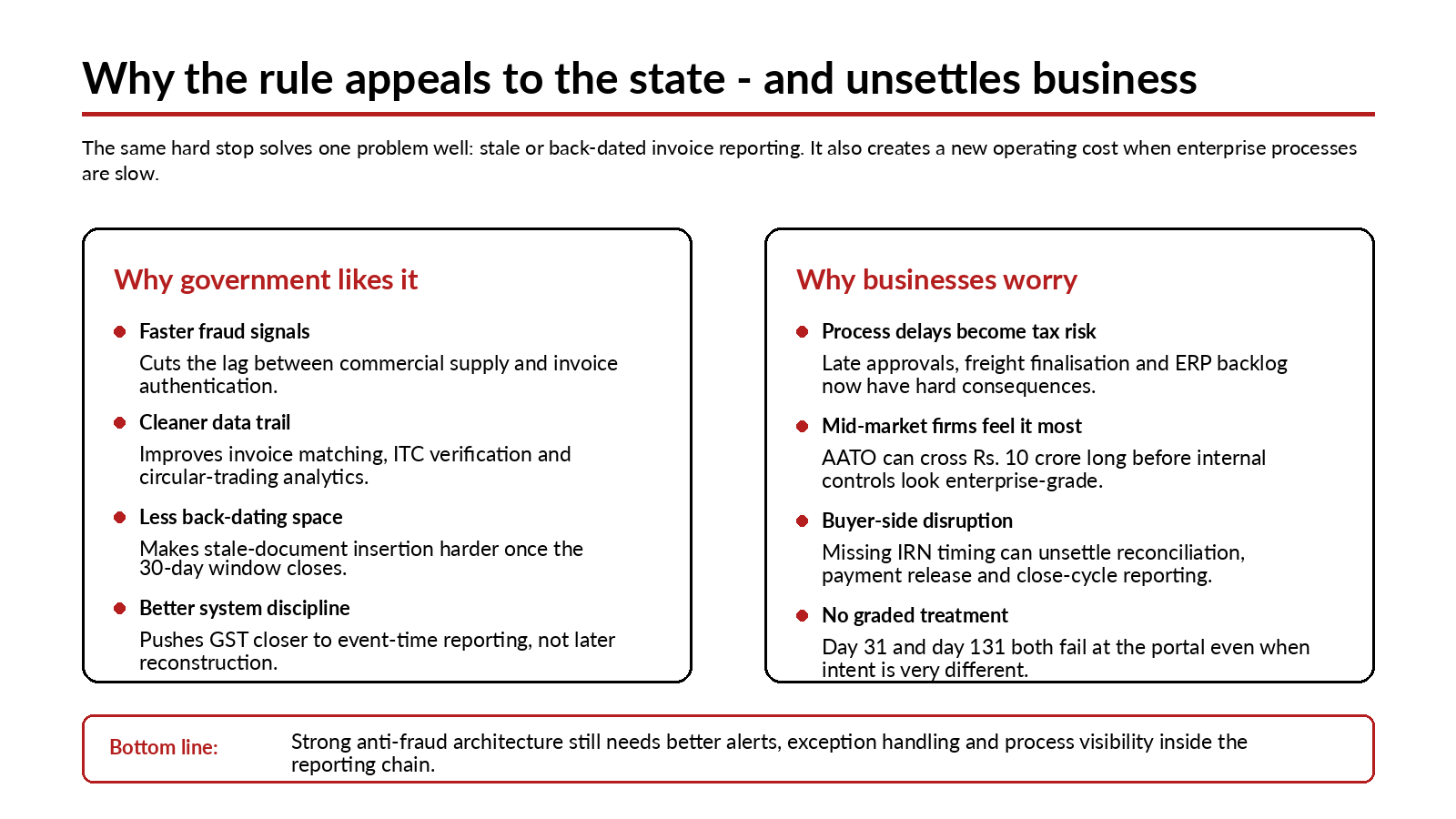

That intervention is not hard to understand. GST has been moving away from return-era compliance toward transaction-era controls. E-invoice data feeds outward supply reporting, recipient visibility and, where relevant, e-way bill generation. GSTN’s own architecture has steadily deepened this linkage, and the administration now uses e-invoice and bill-system data for invoice ITC verification, supply-chain analysis and detection of circular trading. In a system built to authenticate business events close to the time they occur, stale invoice reporting is more than clerical disorder. It is a blind spot.

Scale sharpens the state’s incentive. Gross GST collections touched a record Rs. 22.08 lakh crore in 2024-25, while the Economic Survey reported Rs. 17.4 lakh crore of GST collections in April-December 2025 and a 21 percent year-on-year rise in cumulative e-way bill volumes over the same period. At that volume, tax administration values early signal capture over later explanation. A 30-day IRP window is therefore best read as an anti-fraud filter and a data-discipline measure: it compresses the gap between supply, invoice authentication and downstream compliance. The policy intent is rational, even if the execution remains blunt.

It also fits a broader administrative instinct. Once invoice data is meant to auto-flow into returns and analytics, the marginal utility of late reporting falls fast. A document uploaded weeks after the commercial event may still satisfy bookkeeping, but it is less useful as a live compliance signal. That is the core shift. GST is no longer content with accurate records alone; it increasingly demands timely records. For corporate finance teams, that means the tax function has to sit much closer to dispatch, billing and collections than it did in the early GST years.

Where the operational rigidity shows up

Where the rule bites is in the ordinary Indian enterprise, not only in the obvious bad actor. Mid-market manufacturers, engineering contractors, logistics groups, pharma distributors and multi-state dealer networks often issue the commercial invoice promptly but complete the e-invoice process only after internal checks, customer references, freight allocation or ERP batch posting. The firms now directly exposed are not just blue-chip corporations with industrial-scale controls. A business can cross the Rs. 10 crore AATO threshold quickly on a PAN basis and still run with fragmented systems, outsourced accounting and month-end firefighting. For them, the IRP cutoff creates compliance friction that is operational before it is legal.

The second-order effects travel beyond the seller. GSTN’s own material makes clear that successful IRP reporting auto-populates GSTR-1 and GSTR-2A, and can feed e-way bill generation when transport details are provided. When a supplier misses the 30-day window, the problem is no longer confined to a delayed document number. It spills into buyer reconciliation, vendor payment holds, audit trail gaps and credit-timing anxiety inside the recipient’s finance team. Tax professionals are forced out of the relatively familiar work of return repair and into preventive process engineering: approval hierarchies, maker-checker discipline, exception logs and aging dashboards. That is not trivial. It changes where advisory value sits.

For consultants and in-house tax heads, this alters the advisory brief. The old model rewarded after-the-fact clean-up: amendment strategies, disclosure repair and explanatory drafting once the return cycle caught up. The new model rewards control design. Teams now need invoice-aging reports, ownership matrices, escalation triggers and exception reviews before the portal shuts the door. That may sound procedural, but it is where real tax incidence now sits for the corporate sector: in internal process quality, not only in interpretative debate.

There is also a quiet middle-class angle. Compliance friction eventually shows up in working-capital cycles, especially in sectors where smaller vendors supply larger enterprises and payment release depends on clean invoice acceptance. A tax rule rarely lands on household budgets in a neat, visible line item. But when vendor payments slow, financing costs rise, and documentation risk is repriced into contracts, some of that burden travels through margins and prices. The marginal utility of a hard stop may still be positive for the state if fraud falls. Yet the private cost of rigidity is real, and it is diffused across supply chains rather than concentrated in one balance sheet.

Necessary, but not yet a finished design

That is why the present design feels necessary but incomplete. The strongest case for the e-invoice 30 day rule is that it attacks backdating and stale-document insertion at the system gate instead of leaving everything to audit, scrutiny and retrospective dispute. The weakest case is that day 31 and day 131 are treated almost alike: both fail at the portal. A modern compliance architecture should distinguish chronic evasion from provable process breakdown. Right now, the rule is better at refusing late invoices than at separating intent from error.

A smarter version of the policy would not abandon rigidity; it would target it better. Pre-deadline nudges inside GSTN and ERP ecosystems, document-aging alerts at GSTIN and PAN level, role-based escalation for unresolved drafts, and a tightly ring-fenced exception channel for demonstrable contingencies would preserve anti-fraud value without normalising slippage. The state has already expanded infrastructure – six portals are authorised to generate IRNs – so the remaining weakness is less portal capacity than enterprise governance. That is a solvable problem, but only if policy recognises it.

The larger story is that GST is maturing into a system that expects tax events to be reported almost as they happen, not reconstructed weeks later. In that world, the e-invoice 30 day rule is not an isolated irritant. It is a signal about where administration is headed. Companies above the Rs. 10 crore line should read it that way. The question is no longer whether digitisation has arrived. It is whether internal commercial clocks, tax controls and self-assessment architecture are finally moving in the same direction.

Sources & Data Points

- Advisory: Time Limit for Reporting e-Invoice on the IRP Portal – Lowering of Threshold to AATO 10 Crores and Above (27 Mar 2025) – Used for the 1 April 2025 effective date, the 30-day bar, document coverage and the clarification that taxpayers below Rs. 10 crore AATO are outside the restriction for now.

- Advisory on New Time limit for Reporting of Invoices on the IRP Portal (8 Sep 2023) – Used for the earlier 30-day reporting cap that applied to taxpayers with AATO of Rs. 100 crore and above.

- Notification No. 10/2023 – Central Tax dated 10 May 2023 – Used for the current e-invoicing threshold of more than Rs. 5 crore from 1 August 2023.

- Notification No. 17/2022 – Central Tax dated 1 Aug 2022 – Used for the earlier threshold shift to more than Rs. 10 crore from 1 October 2022.

- Notification No. 01/2022 – Central Tax dated 24 Feb 2022 – Used for the earlier threshold shift to more than Rs. 20 crore from 1 April 2022.

- Notification No. 05/2021 – Central Tax dated 8 Mar 2021 – Used for the earlier threshold shift to more than Rs. 50 crore from 1 April 2021.

- CGST Tax Notification listing for Notification No. 13/2020 – Central Tax dated 21 Mar 2020 – Used for the principal notification trail under Rule 48(4).

- GSTN e-Invoice Glossary leaflet – Used for the definitions of e-invoicing, IRP, IRN, AATO and the statement that six portals are authorised to generate IRNs.

- GSTN e-invoicing – At a Glance – Used for auto-population into GSTR-1 and GSTR-2A and for the e-way bill linkage.

- GSTN Annual Report 2023-24 – Used for GST Prime’s use of e-invoice data in invoice ITC verification, supply-chain analysis and circular-trading detection.

- PIB Press Note: Record Gross GST collection in 2024-25 (30 Jun 2025) – Used for the record gross GST collection figure of Rs. 22.08 lakh crore in 2024-25.

- Economic Survey 2025-26 highlights / PIB release – Used for the April-December 2025 gross GST collections of Rs. 17.4 lakh crore and the 21 percent year-on-year rise in cumulative e-way bill volumes.

- Circular No. 237/31/2024-GST dated 15 Oct 2024 – Used for the current statutory language around section 16(4) timing for input tax credit.