It isn’t India’s non-event anymore: once foreign parent and backstop rules switch on, Indian groups face real cash-tax, reporting, and capital-allocation consequences even without a domestic statute.

Pillar Two India is still being discussed in too many boardrooms as a deferred legislative story: no Indian statute, no immediate risk, no need to mobilise scarce tax bandwidth. That reading was shaky in 2024. In 2026, it is wrong. The OECD’s architecture was designed to prevent a large multinational group from escaping minimum tax simply because one jurisdiction has not legislated yet. Once other jurisdictions in the group have switched on qualified rules, the practical question stops being whether India has implemented Pillar Two and becomes far more commercial: where in the chain can top-up tax be collected, who bears the cash cost, and how much compliance friction gets imported into the group’s reporting cycle anyway?

Why Pillar Two India isn’t insulated by non-implementation

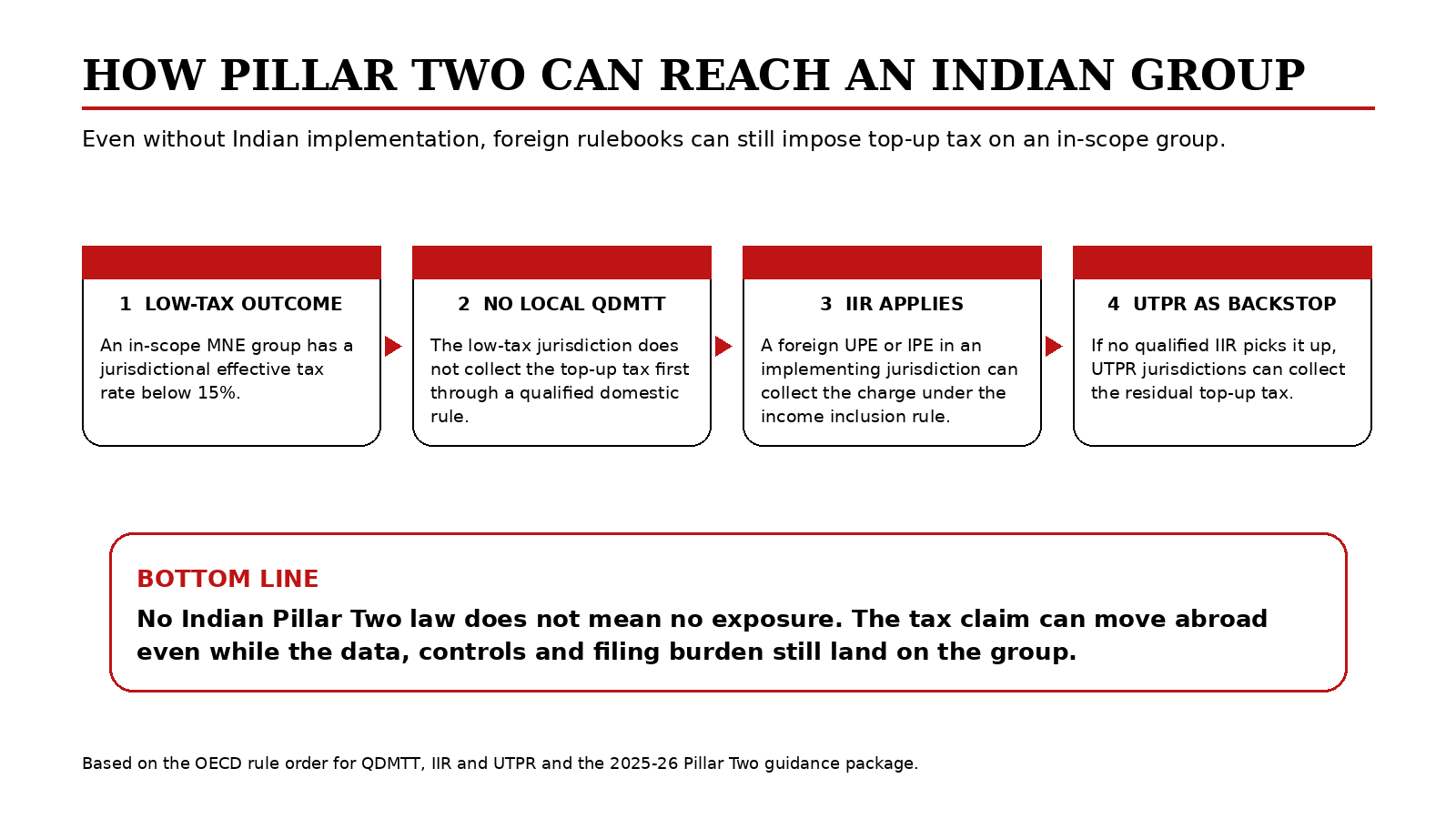

That is the first trap in the Indian debate. The GloBE rules operate as a common approach, not as a treaty that binds every country to enact the same law on the same day. Jurisdictions are not compelled to adopt the rules. They are, however, expected to accept the agreed rule order when other members do. A qualified domestic minimum top-up tax, or QDMTT, gives the low-tax jurisdiction the first bite. If that jurisdiction has no QDMTT, the income inclusion rule can let the parent jurisdiction collect the top-up. If the ultimate parent sits in a non-implementing jurisdiction, the charge can move up to an intermediate parent. If no qualified IIR picks it up, the undertaxed profits rule sits behind it as the backstop. Waiting in India doesn’t create a vacuum. It can simply re-route the tax claim abroad.

That is why Indian groups above the EUR 750 million threshold can’t treat Pillar Two as a memo for the international tax team alone. Indian-headquartered groups with subsidiaries in implementing jurisdictions may find that foreign parent-level or intermediate-parent rules are doing the work that an Indian law has not yet done. Foreign-parent groups with Indian operations face the mirror image: the Indian entity’s numbers can still shape the jurisdictional effective tax rate and the group’s global top-up tax outcome even if India has not enacted a domestic regime. The risk isn’t limited to exotic structures. It can arise from incentive-driven low-tax outcomes, deferred tax timing, entity classification differences, permanent establishment mismatches, and the messy edges where book income and taxable income stop resembling one another. The real issue is whether the group can defend its effective rate calculation under live foreign rules.

The 2025-26 guidance changed the compliance map

The 2025-26 OECD package has made that defence exercise more immediate and more technical. In May 2025, the OECD published a consolidated commentary incorporating agreed administrative guidance through March 2025. In January 2026, the Inclusive Framework followed with a side-by-side package that does more than tidy drafting. It introduces a Simplified ETR Safe Harbour, extends the transitional CbCR safe harbour to fiscal years beginning on or before 31 December 2027, and rolls out new safe harbours such as the SbS Safe Harbour and the UPE Safe Harbour from 1 January 2026 for qualifying regimes. Add the GloBE Information Return schema and the first exchanges scheduled for 2026, and Pillar Two stops looking like a conceptual reform. It starts looking like an annual reporting system with real filing, data and control consequences.

Pillar Two India and the revenue question

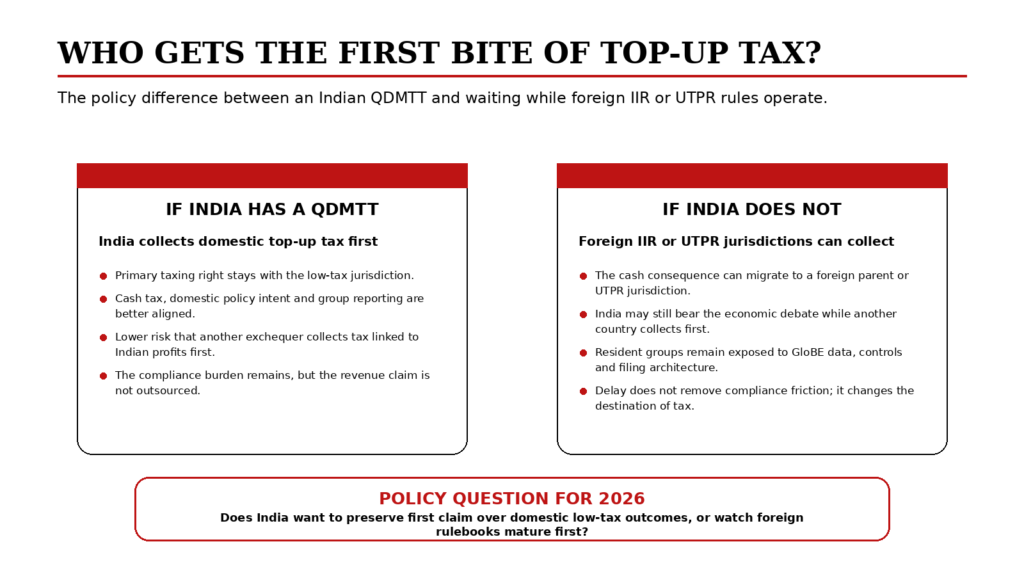

For India, the policy tension is becoming harder to ignore. The OECD’s own framework is clear that the low-tax jurisdiction has the primary right to collect top-up tax under a QDMTT. If India does not create that first-claim instrument, the economics do not disappear; the right to collect can migrate to jurisdictions applying an IIR or, failing that, a UTPR. That has a sovereignty angle, but it also has a revenue-design angle. A country that forgoes a QDMTT may be giving up tax buoyancy on profits arising within its own market or operating base while still leaving its resident groups fully exposed to the compliance architecture. As of the Union Budget 2026 cycle, India’s Finance Bill materials do not set out a Pillar Two implementation chapter. That may reflect caution. It should not be mistaken for insulation.

The boardroom effect is larger than the tax line

The corporate second-order effects are already visible in how finance teams are re-pricing tax incentives and cross-border structures. A tax holiday, credit, or special rate doesn’t vanish under Pillar Two, but its marginal utility can fall sharply if the benefit is clawed back elsewhere through a foreign top-up tax. That changes capital allocation, internal hurdle rates, and the valuation of intellectual property hubs, procurement centres, treasury companies and contract-risk allocations built for a pre-GloBE world. It also changes M&A. Buyers now need to ask not only what the target’s historical tax rate was, but whether that rate survives a GloBE calculation, whether safe harbours are genuinely available, and whether data quality is strong enough to support the self-assessment architecture the regime assumes.

A new workload for Indian tax professionals

For Indian tax professionals, that means the work is moving away from elegant position papers and toward operating discipline. The scarce skill is no longer just knowing the rule order. It is building a defensible data chain from consolidation systems to country-by-country reporting, deferred tax registers, entity classification, ownership mapping and GIR-ready disclosures. That is where compliance friction lives. Groups need to reconcile what the CFO signs off in financial statements with what the tax department says in CbCR and what the group will eventually report under the GIR. Any break in that chain can be expensive. The advisory market will reward firms that can combine international tax, transfer pricing, accounting and systems controls. In India, that opens a serious lane for practitioners willing to move beyond litigation reflexes and into implementation architecture.

Why this matters beyond tax departments

The middle class is not going to see Pillar Two as a line item in a salary slip, and claims of immediate consumer pain would be overstated. But the regime still matters outside the tax bar. When multinational groups lose some of the arbitrage value of locating profits in low-tax pockets, they reassess where to hire, where to warehouse functions, how to price intra-group services and how much of a tax-driven structure is worth preserving. Over time, part of that tax incidence can show up in wages, pricing, dividend policy and investment pacing. The effect will be uneven and often indirect. Still, it would be naive to think a global minimum tax that changes post-tax returns leaves the wider economy untouched.

The choice India is really making

The real Indian choice in 2026 is not between action and safety. It is between collecting first and calculating late, or calculating now while letting someone else collect first. Indian groups that are potentially in scope should already be running threshold tests, jurisdictional ETR diagnostics, safe-harbour eligibility reviews and GIR-readiness checks. Policymakers, for their part, need to decide whether India wants to preserve primary taxing rights over domestic low-tax outcomes or continue watching the international system mature from the sidelines. Pillar Two India is no longer a question of legislative curiosity. It is a question of who gets the cash, who carries the systems burden, and whether Indian business chooses to react before foreign rulebooks do it for them.

Sources & Data Points

1.OECD — Global Minimum Tax overview — https://www.oecd.org/en/topics/global-minimum-tax.html | Used for the agreed rule order: QDMTT first, then IIR, then UTPR.

- OECD — Global Anti-Base Erosion Model Rules (Pillar Two) — https://www.oecd.org/en/topics/sub-issues/global-minimum-tax/global-anti-base-erosion-model-rules-pillar-two.html | Used for the May 2025 consolidated commentary release and the overall Pillar Two framework.

- OECD — Consolidated Commentary to the Global Anti-Base Erosion Model Rules (2025) — https://www.oecd.org/en/publications/tax-challenges-arising-from-the-digitalisation-of-the-economy-consolidated-commentary-to-the-global-anti-base-erosion-model-rules-2025_a551b351-en.html | Used for the statement that the consolidated commentary incorporates agreed administrative guidance through March 2025.

- OECD — Side-by-Side Package (January 2026) — https://www.oecd.org/content/dam/oecd/en/topics/policy-sub-issues/global-minimum-tax/side-by-side-package.pdf | Used for the Simplified ETR Safe Harbour, the extension of the Transitional CbCR Safe Harbour through fiscal years beginning on or before 31 December 2027, and the 1 January 2026 effective date for the SbS and UPE Safe Harbours.

- OECD — Administrative Guidance on Article 9.1 of the GloBE Model Rules (January 2025) — https://www.oecd.org/content/dam/oecd/en/topics/policy-sub-issues/global-minimum-tax/administrative-guidance-article-9-1-globe-rules-pillar-two-january-2025.pdf | Used for the statement that Pillar Two remains a common approach and for January 2025 interpretive guidance.

- OECD — Questions and Answers on the Qualified Status under the Global Minimum Tax — https://www.oecd.org/content/dam/oecd/en/topics/policy-sub-issues/global-minimum-tax/qualified-status-under-the-global-minimum-tax-questions-and-answers.pdf | Used for the central-record explanation and the status of transitional qualified legislation.

- OECD — Announcement on qualified legislation and GIR tools (15 January 2025) — https://www.oecd.org/en/about/news/announcements/2025/01/global-minimum-tax-release-of-compilation-of-qualified-legislation-and-information-filing-and-exchange-tools.html | Used for the release of the central record, updated GIR and related exchange tools.

- OECD — GloBE Information Return XML Schema — https://www.oecd.org/en/publications/globe-information-return-pillar-two-xml-schema_c594935a-en.html | Used for the standardised GIR filing architecture.

- OECD — GloBE Information Return Status Message XML Schema — https://www.oecd.org/content/dam/oecd/en/publications/reports/2025/07/globe-information-return-pillar-two-status-message-xml-schema_eb7bc5ca/449e3cc3-en.pdf | Used for the statement that the first GIR exchanges are scheduled for 2026.

- OECD — Understanding the Side-by-Side Package webinar page — https://www.oecd.org/en/events/2026/01/global-minimum-tax-understanding-the-side-by-side-package.html | Used for the 147 countries and jurisdictions reference around the Inclusive Framework’s January 2026 package.

- Government of India — Finance Bill, 2026 — https://www.indiabudget.gov.in/doc/Finance_Bill.pdf | Reviewed to verify that the Budget 2026 direct-tax papers do not set out a Pillar Two implementation chapter.

- Government of India — Memorandum explaining the Finance Bill, 2026 — https://www.indiabudget.gov.in/doc/memo.pdf | Reviewed alongside the Bill for the same point on the absence of Pillar Two legislation in the 2026 budget cycle.