India’s MAP regime is no longer too peripheral to matter. The sharper 2026 question is whether advisers still treat competent authority relief as a late-stage rescue.

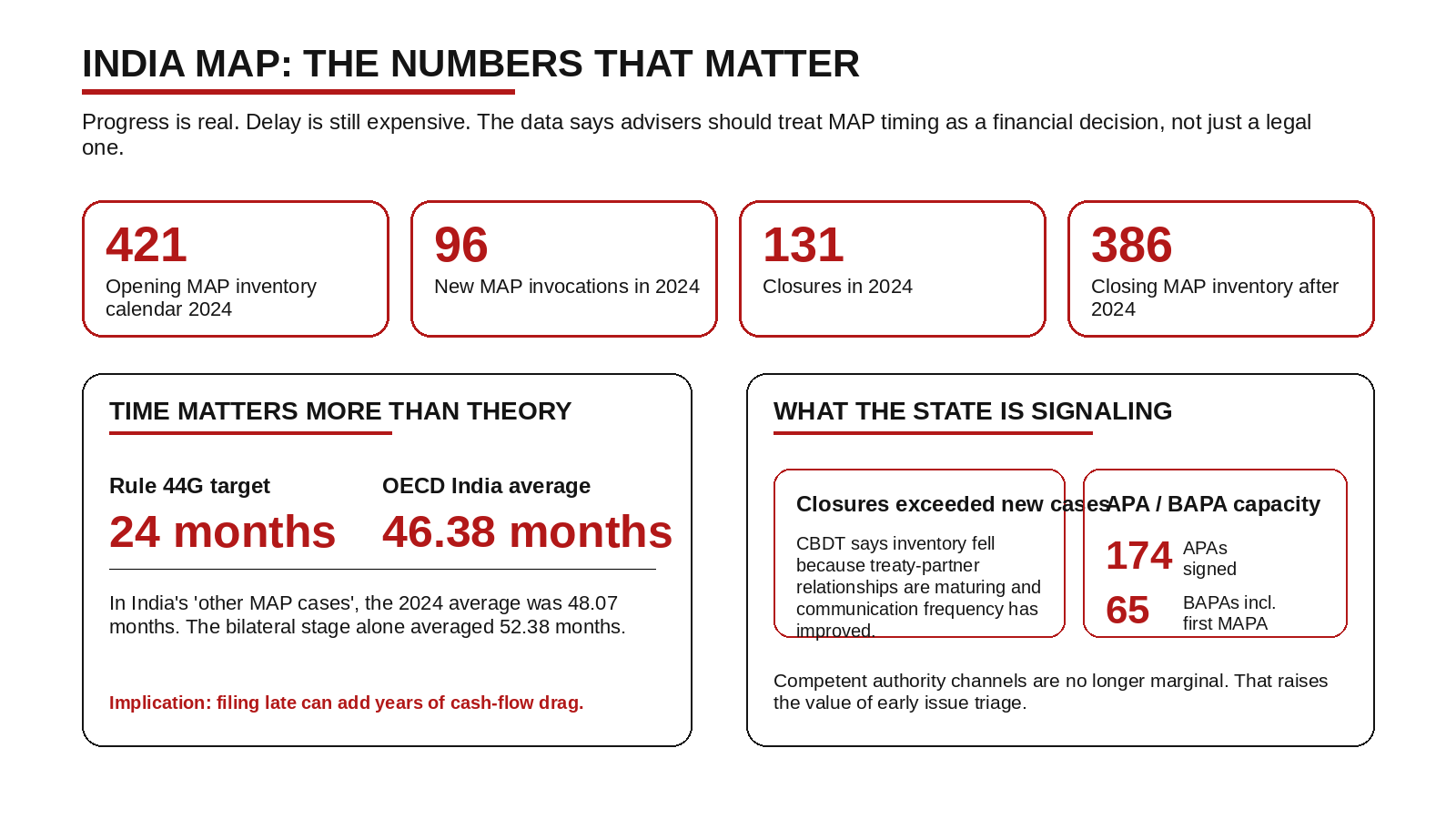

Mutual Agreement Procedure is often treated in India as the emergency exit after draft assessment, DRP, and appellate posture have already hardened. That habit made sense when competent authority engagement felt slow, opaque and secondary to domestic remedy. It makes less sense now. CBDT’s own recent reporting shows MAP closures in calendar 2024 exceeded fresh invocations, pulling inventory down from 421 to 386, while the same institutional machinery signed a record 65 bilateral APAs, including India’s first multilateral APA, in FY 2024-25. The signal is plain: competent authority work is no longer peripheral administration. It is part of the state’s tax-certainty strategy. The real strategic error is not that advisers use MAP too often. It is that they often frame it too late, after litigation psychology has already taken over.

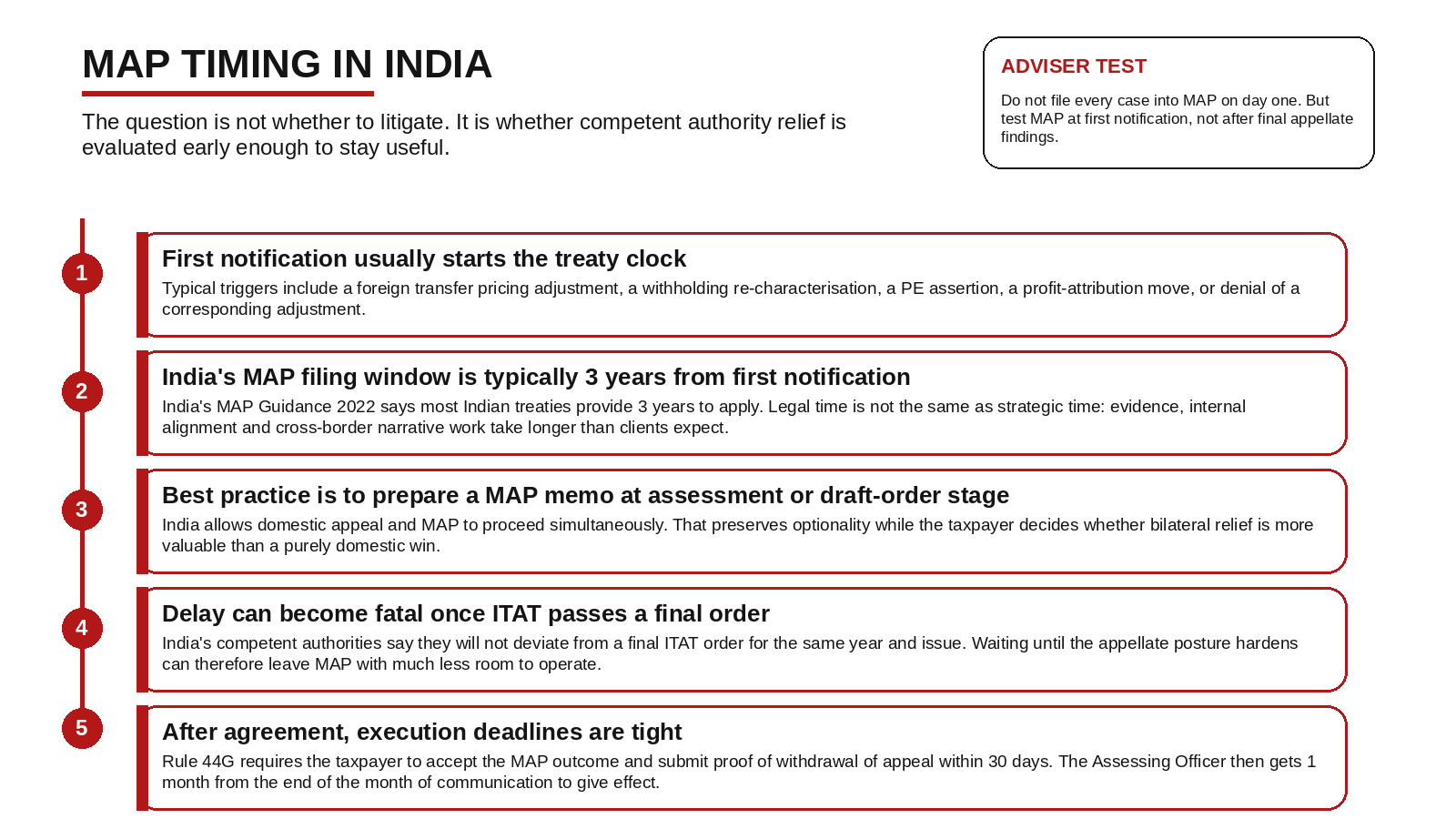

The treaty clock starts earlier than the client thinks

Under India’s MAP guidance, most treaties give taxpayers three years from the first notification of the action that leads to taxation not in accordance with the treaty. That sounds roomy. In practice it is not. The first foreign adjustment, withholding re-characterisation, PE assertion, corresponding adjustment denial, or profit-attribution move usually arrives long before the case file is commercially mature. By the time finance teams gather inter-company agreements, functional analyses, board minutes, emails, and position papers, a meaningful part of that clock has already been spent. Treating MAP as a filing that can wait until after domestic arguments are tested confuses legal limitation with strategic readiness. The marginal utility of waiting is often low. The cost of lost optionality can be very high.

India also gives taxpayers more flexibility than many treaty partners by allowing domestic appeals and MAP to proceed simultaneously. That is a major strategic advantage, not a minor procedural footnote. It lets taxpayers preserve domestic rights while opening a cross-border channel that can actually remove double taxation. But the same guidance contains the hard edge that many advisers underweight: once the ITAT has passed a final order, India’s competent authorities will not deviate from it, and the MAP file is effectively shut on the Indian side. In other words, the system is liberal at the front end and unforgiving at the back end. A case that enters MAP early can keep leverage. A case that waits until final appellate findings may keep principle, but lose relief.

Why late MAP filings destroy leverage, not just time

This is not only about legal timing. It is about bargaining architecture. Competent authority relief works best when facts are still being assembled, transfer pricing narratives are still coherent, and the taxpayer’s global position is internally consistent across both jurisdictions. Late MAP invocation usually means the file has already been optimised for domestic litigation. That is a different craft. Litigation rewards sharp issue selection, aggressive factual contest, and jurisdiction-specific argument. MAP rewards full disclosure, symmetry of narrative and credible room for bilateral compromise. A file built exclusively for one theatre often travels badly to the other. The result is more compliance friction, more duplicated work, and a higher risk that the taxpayer spends years paying advisers to defend a position that competent authorities could have reframed much earlier.

There is also a cash-flow problem. Rule 44G, as amended in 2020, says India’s competent authority should endeavour to resolve MAP disputes within an average of 24 months. Yet OECD data for 2024 shows India’s total average time for post-2015 MAP cases at 46.38 months, and 48.07 months for other MAP cases, with the bilateral stage alone averaging 52.38 months in that category. The gap matters. If the real-world process already runs long, pushing the decision to invoke MAP deeper into the dispute cycle only compounds the working-capital drag. For the corporate sector that means larger provisions, slower release of management bandwidth and weaker capital allocation discipline. For professional firms it means a heavier premium on early case triage rather than heroic late-stage drafting.

India’s MAP machine is moving, but not quickly enough

None of this means MAP has become a silver bullet. India’s latest public numbers are encouraging, but they do not justify complacency. CBDT says 131 MAP cases were closed in 2024 against 96 new invocations, and attributes the declining inventory to maturing treaty-partner relationships and more frequent communication. That is genuine progress. But seen against OECD’s 2024 global average MAP resolution time of 27.4 months, India still has a distance problem. The state is investing in tax certainty, yet the user experience remains stretched. That makes front-end timing more important, not less. In a slow system, the penalty for entering late is magnified. The adviser’s job is to compress avoidable delay before the competent authorities ever pick up the file.

The new operational message from CBDT

Recent administration has also become more explicit about implementation mechanics. In October 2025, CBDT issued an office memorandum to deal with MAP outcomes where an appeal is pending before the Commissioner of Income-tax (Appeals), clarifying that the CIT(A)’s intimation accepting withdrawal can serve as proof of withdrawal for Rule 44G purposes. That sounds technical. It is actually revealing. It tells taxpayers that the department is trying to remove operational choke points after MAP resolution, not merely publish broad policy intent. When administration starts fixing the plumbing, advisers should stop treating MAP as exotic relief. They should treat it as a real process with real execution dependencies – filing discipline, appeal mapping, document control, and internal governance.

Where MAP should sit in the advisory playbook

The better advisory model in 2026 is not ‘litigate first, MAP later.’ It is a forked strategy memo prepared at first notification. One branch tests whether the dispute is genuinely treaty-driven – transfer pricing, PE, attribution, income characterisation, withholding mismatch, corresponding adjustment denial. The other tests whether a domestic court win would still leave unrelieved double taxation abroad. If the answer to both is yes, MAP should be evaluated immediately, even if no filing is made that day. That changes client behaviour. Finance teams start preserving cross-border evidence earlier. Foreign affiliates align narratives sooner. Counsel stop drafting as though the only audience is the domestic appellate chain. The result is not softness. It is better case design.

Mutual Agreement Procedure is not surrender

There will still be disputes where MAP is the wrong lead instrument. Purely domestic computational issues, thin treaty questions, or cases where the commercial objective is precedent rather than relief may justify a harder appellate posture. But advisers should be honest about what clients usually need. Most businesses do not buy principle for its own sake. They buy certainty, cash-flow visibility and an end to duplicated taxation. That has downstream effects well beyond the tax department. It reduces the tax incidence of uncertainty embedded in prices, preserves investment appetite, and spares even middle-class consumers some of the invisible costs created when multinational disputes become a standing overhead. Mutual Agreement Procedure, used early enough, is not capitulation. It is disciplined corporate finance wearing a treaty law suit.

SOURCES & DATA POINTS

- Mutual Agreement Procedure (MAP) Guidance 2022, Income Tax Department, Government of India

Official MAP guidance on filing windows, simultaneous appeal and MAP, ITAT final-order position, and implementation framework. Open source

- Notification No. 23/2020 [G.S.R. 282(E)] amending Rule 44G and Form 34F

Official rule text on MAP application procedure, 24-month endeavour, 30-day taxpayer acceptance window, and AO effect-giving timeline. Open source

- Advance Pricing Agreement Programme of India – Annual Report (2024-25), CBDT

Used for 2024-25 APA/BAPA numbers and CBDT’s discussion of MAP inventory and closures in calendar 2024. Open source

- Office Memorandum dated 27 October 2025 on giving effect to MAP outcomes where appeal is pending before CIT(A)

Recent operational clarification that CIT(A) intimation accepting withdrawal can serve as proof of withdrawal for Rule 44G purposes. Open source

- OECD – Mutual Agreement Procedure Statistics per jurisdiction: India (2024 reporting period)

Official jurisdiction-specific MAP statistics used for India’s 2024 average resolution times and category-level timing data. Open source

- OECD – 2024 Mutual Agreement Procedure Statistics dataset page

Official OECD landing page for the 2024 MAP statistics release. Open source

- OECD announcement dated 31 October 2025 on 2024 MAP and APA statistics

Used for the 2024 global average MAP resolution time and wider tax-certainty context. Open source