APA vs litigation is now less a doctrinal choice than a capital-allocation decision: how much uncertainty can a large taxpayer still afford to carry on its books?

APA vs litigation is no longer a seminar-room binary. In 2026, it has become a boardroom decision about capital, management bandwidth and the marginal utility of uncertainty. Large taxpayers can still win in appeal. Some should keep fighting. But the old instinct — contest every transfer-pricing adjustment because conceding once invites the next one — is losing force. India’s tax administration is steadily building a certainty architecture around transfer pricing, while litigation remains slow, fact-intensive and expensive in ways that don’t always show up in legal budgets. The real question isn’t whether an assessee has a technical case. It is whether another five or seven years of contest actually creates more enterprise value than a negotiated forward path.

The APA regime has crossed the proof-of-concept stage

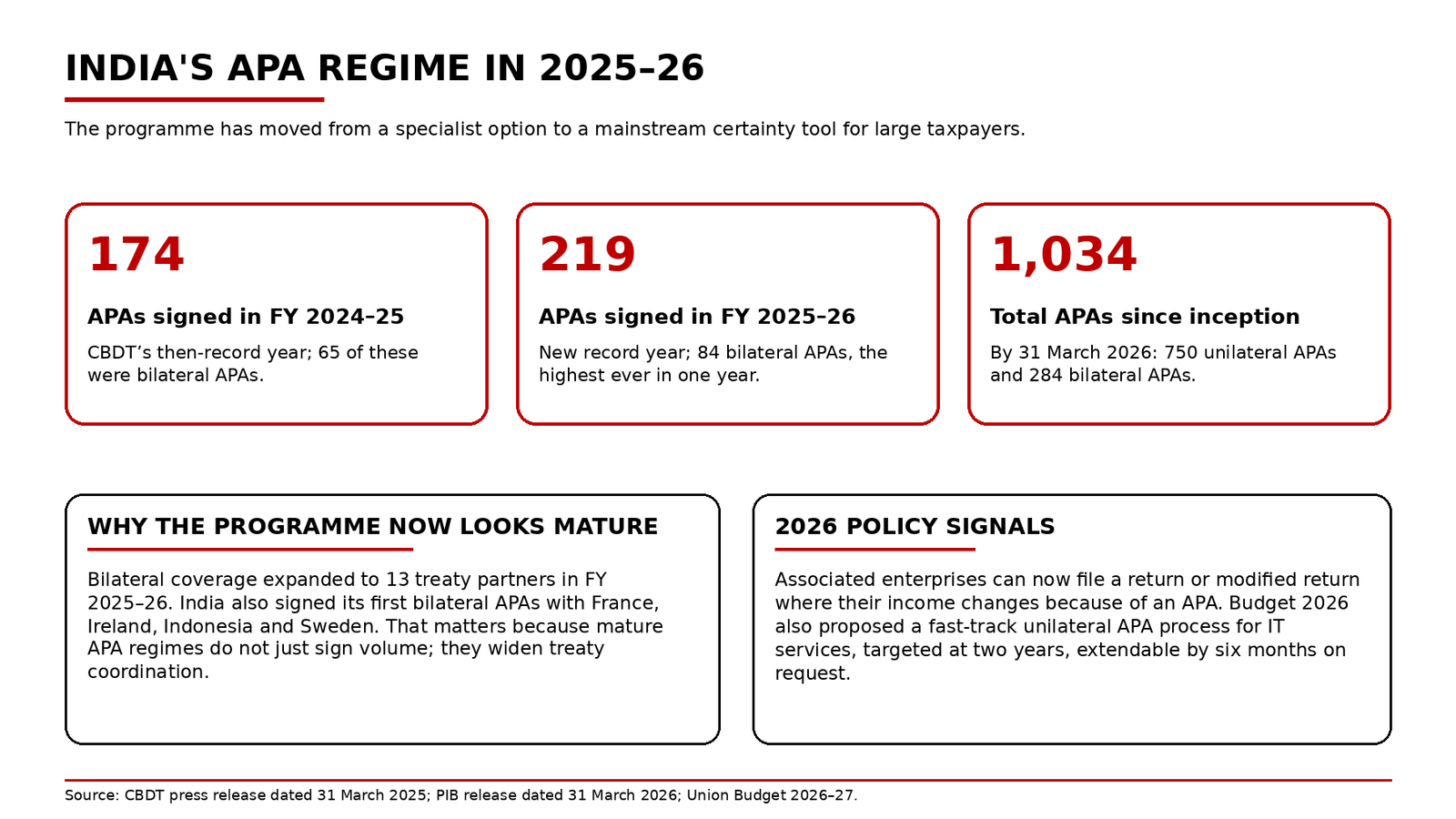

That shift is visible in the numbers. CBDT signed a record 174 Advance Pricing Agreements in FY 2024-25, then surpassed that with 219 APAs in FY 2025-26. The cumulative count has now crossed 1,000, reaching 1,034 since the programme began. Just as important, the bilateral side is deepening. India signed 65 BAPAs in FY 2024-25 and 84 in FY 2025-26, with the latest year covering 13 treaty partners and delivering first-ever bilateral APAs with France, Ireland, Indonesia and Sweden. This is not bureaucratic decoration. It is evidence that the regime has moved from experimental to institutional. Once a dispute-resolution channel starts producing that kind of throughput, corporate tax strategy has to treat it as mainstream rather than exceptional.

Why APA vs litigation feels different in 2026

The legal and administrative signals all point in the same direction. The Income-tax Act, 2025 preserves the APA framework and confirms that agreements signed under the old law continue if they are not inconsistent with the new Act. Finance Act, 2026 has gone a step further by allowing the associated enterprise of the person entering into an APA to file a return or modified return, within the prescribed period, where its own income changes because of that agreement. For IT services, the Union Budget 2026-27 proposed a fast-track unilateral APA process with an endeavour to conclude cases within two years, extendable by six months at the taxpayer’s request. The department has also introduced a renewal form that expressly aims to cut duplication and lower processing time where transactions remain the same or highly similar. Even outside APA, the policy direction is unmistakable: the 2025 Budget proposed a three-year block-period arm’s-length-price scheme as an alternative to yearly examination, with implementation papers saying the scheme takes effect from 1 April 2026 and rules are to be framed by 30 September 2026.

Where APA beats litigation

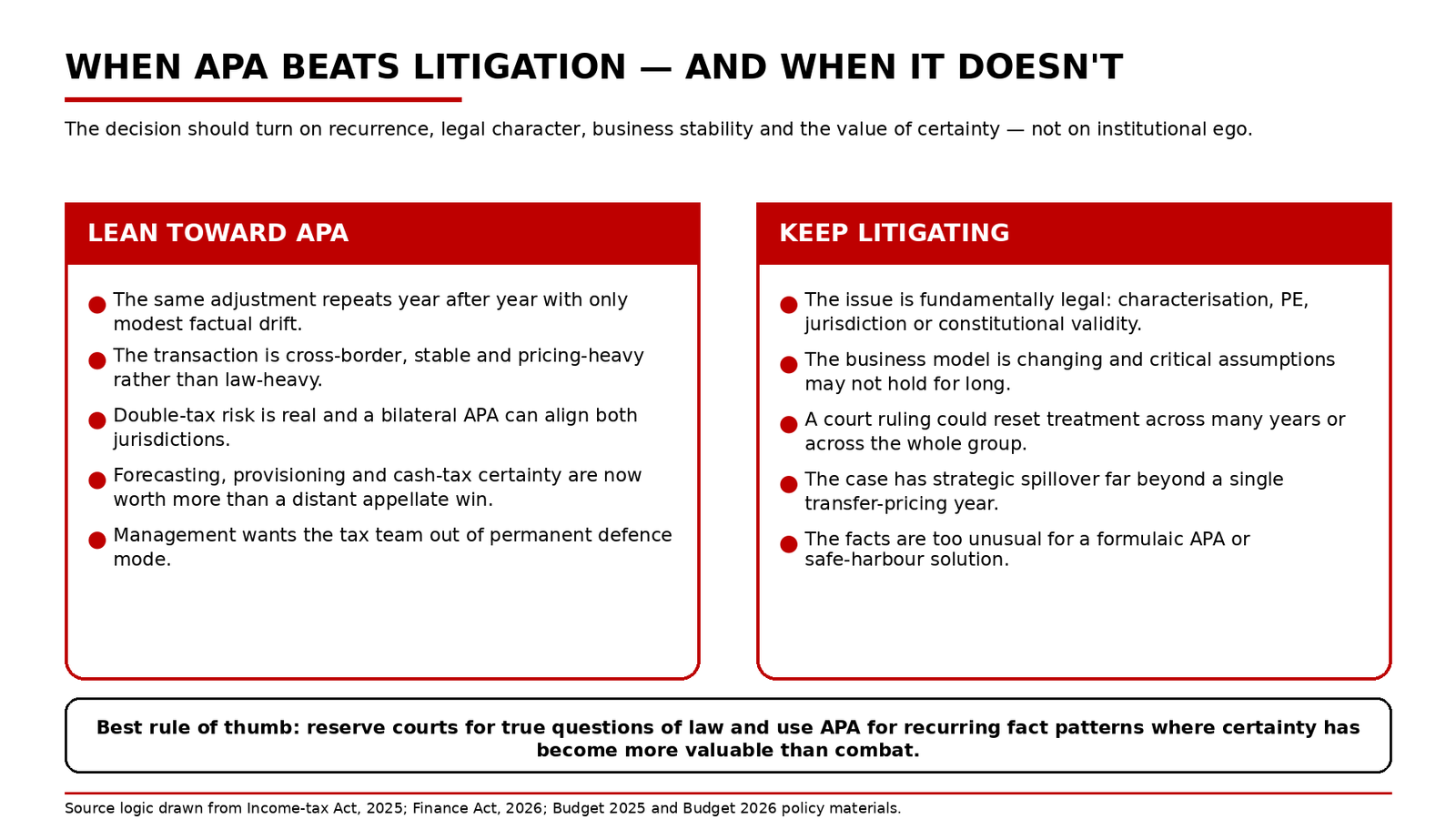

The case for APA is strongest where the dispute is recurring, fact-heavy and commercially stable. Think routine IT and IT-enabled services, contract R&D, distribution structures, treasury support, low value-adding services, intra-group financing or long-running service arrangements where the same functions, assets and risks are examined every year with modest factual drift. In those cases, the taxpayer is often not fighting a one-year adjustment at all; it is fighting an annuity. Litigation may still produce a win for one assessment year, but the compliance friction survives, the documentation burden repeats, and the tax function remains trapped in defensive mode. A bilateral APA has another advantage that litigation often cannot deliver cleanly: protection against actual or potential double taxation through coordinated treatment with the treaty partner.

When litigation still earns its keep

That doesn’t mean large taxpayers should stop appealing on principle. Litigation still matters where the issue is genuinely legal rather than merely computational. Characterisation disputes, permanent-establishment questions, jurisdictional overreach, constitutional challenges, retroactivity arguments and cases that could reset the treatment of a business model across years or across the group may still belong in court. The same is true where the facts are in motion. An APA works best when critical assumptions can be stated with confidence. If the business is pivoting, functions are migrating, ownership of intangibles is being reorganised, or the value chain is moving away from a steady-state model, an APA can lock in a methodology that quickly goes stale. In those situations, accepting short-run litigation pain may be cheaper than institutionalising the wrong answer.

The real cost-benefit test

Large taxpayers should therefore stop treating APA as a soft option and litigation as the hard-headed one. The harder question is arithmetic. What is the expected tax and interest exposure over multiple years? How much finance-team time is being consumed by audits, objections, remands and appeal strategy? What is the cost of carrying uncertain tax positions through provisioning cycles, investor discussions, internal budgeting and intercompany cash planning? An APA can cover up to five consecutive tax years, and the current renewal guidance also contemplates rollback for earlier years where the rules permit. That changes the payoff profile dramatically. The value of closure is not just lower counsel fees. It is lower variance in effective tax rate, cleaner forecasting and fewer management hours stranded in legacy disputes. In a self-assessment architecture, repeated uncertainty becomes its own cost base. Where a transfer-pricing issue has become repetitive, the marginal utility of another contested year can be surprisingly low.

Why IT services are the clearest swing sector

If any segment captures the 2026 shift, it is IT services. The government has widened the safe-harbour pathway by grouping several technology service segments into a single Information Technology Services category, setting a 15.5 per cent margin, raising the threshold from ₹300 crore to ₹2,000 crore, and promising automated, rule-driven approval with a five-year continuation option. It has simultaneously promised a fast-tracked unilateral APA process for IT services. That combination matters. It gives taxpayers a menu: automated safe harbour for commoditised fact patterns, UAPA where more tailoring is needed, BAPA where double-tax protection matters, and litigation where a genuine point of law remains alive. For many large but routine service providers, continuing to litigate by default will start to look less like discipline and more like habit.

The second-order effects of choosing certainty

There is a wider policy point here. A mature certainty regime changes professional behaviour. Tax teams spend less time drafting post-mortems and more time building evidence packs, intercompany agreements and critical-assumption discipline before the audit cycle begins. Boards get better visibility on tax incidence and capital allocation. Multinationals can price India risk more accurately in investment committees. Even the middle class is not fully insulated from this. Tax uncertainty eventually leaks into hiring plans, pricing decisions and the compliance costs embedded in products and services. None of this means APAs are a magic wand. A badly scoped agreement can simply formalise a weak position. But a system that pushes recurring fact disputes toward ex ante resolution and reserves courts for sharper legal questions is usually a healthier one.

The point at which a large taxpayer should stop fighting

The answer, then, is not ideological. A large taxpayer should stop fighting when the dispute is recurring, the fact pattern is stable, the double-tax risk is real, and the enterprise value of certainty has overtaken the expected upside of a distant appellate win. It should keep fighting where the issue is truly legal, strategically spillover-heavy, or tied to a business model still in flux. That is the mature reading of India’s APA regime in 2026. The system is no longer asking taxpayers only whether they can defend a position. It is asking whether they still want to spend scarce time and capital defending the same position every year.

Sources & Data Points

- CBDT signs record 219 Advance Pricing Agreements in FY 2025–26, taking total number of APAs beyond 1,000 since inception — Used for FY 2025–26 APA volume, cumulative total, UAPA/BAPA split, treaty-partner spread, and the FY 2025–26 safe-harbour context.

- CBDT Signs 174 Advance Pricing Agreements in FY 2024–25 — Used for FY 2024–25 APA volume, bilateral count, cumulative total then achieved, and the first multilateral APA milestone.

- Union Budget 2026–27 Budget Speech — Used for the fast-track unilateral APA proposal for IT services, the associated-entity modified-return proposal, and the 2026 safe-harbour direction.

- Memorandum Explaining the Provisions in the Finance Bill, 2026 — Used for the technical detail that associated enterprises may file a return or modified return where income changes because of an APA, within the prescribed three-month window.

- Income-tax Act, 2025, as amended by Finance Act, 2026 — Used for sections 168 to 170 on advance pricing agreements, effect to APA, and secondary adjustment consequences.

- FAQs on Interplay and Transition — Income-tax Act, 2025 — Used for the 2026 transition clarification that APAs signed under the old Act continue to bind if not inconsistent with the new Act.

- Application for Renewal of an Advance Pricing Agreement (Form 54 guidance note) — Used for the stated objective of reducing duplication and potentially lowering processing time for same or similar transactions, and for the five-year forward plus rollback framing in the guidance.

- Form 54 User Manual — Income Tax Department — Used to confirm that renewal requests can cover unilateral, bilateral or multilateral APAs and can include rollback where the rules permit.

- CBDT notifies amendments in Income-tax Rules, 1962 to expand the scope of safe harbour rules — Used for the 2025 safe-harbour expansion from ₹200 crore to ₹300 crore and the fact that the amendments applied to AY 2025–26 and AY 2026–27.

- Implementation of Budget Announcements 2025–26 — Used for the status note that the proposed three-year block-period arm’s-length-price scheme was to take effect from 1 April 2026, with rules to be framed by 30 September 2026.