Transfer pricing true-ups look routine in group finance decks. In an Indian audit file, the same entry can expose weak contracts, late benchmarking and a fragile control stack.

The Entry That Changes the File

Transfer pricing true-ups usually arrive late in the year, late in the close process. A captive services company is short of its target margin. A distributor has overshot it. A management-fee charge was booked on provisional logic and now needs repair. In management reporting, that feels ordinary. In a tax audit file, it is anything but. A year-end adjustment compresses an entire pricing policy into one visible event, and that is why transfer pricing true-ups draw so much attention. The entry is small. The questions are not.

Why Transfer Pricing True-Ups Happen in the First Place

At one level, transfer pricing true-ups are commercially routine. Limited-risk entities are often priced to land within an arm’s length range, but real years refuse to behave like budgets. Utilisation moves, attrition spikes, foreign exchange shifts, procurement savings fail to arrive, or a delayed product launch leaves a service centre under-absorbed. A year-end true-up restores the result to the pricing policy the group says it intended all along. The OECD’s 2022 Transfer Pricing Guidelines recognise compensating adjustments before the return is filed as a practical feature of transfer pricing because comparable data may not be fully available when associated enterprises first set their prices.

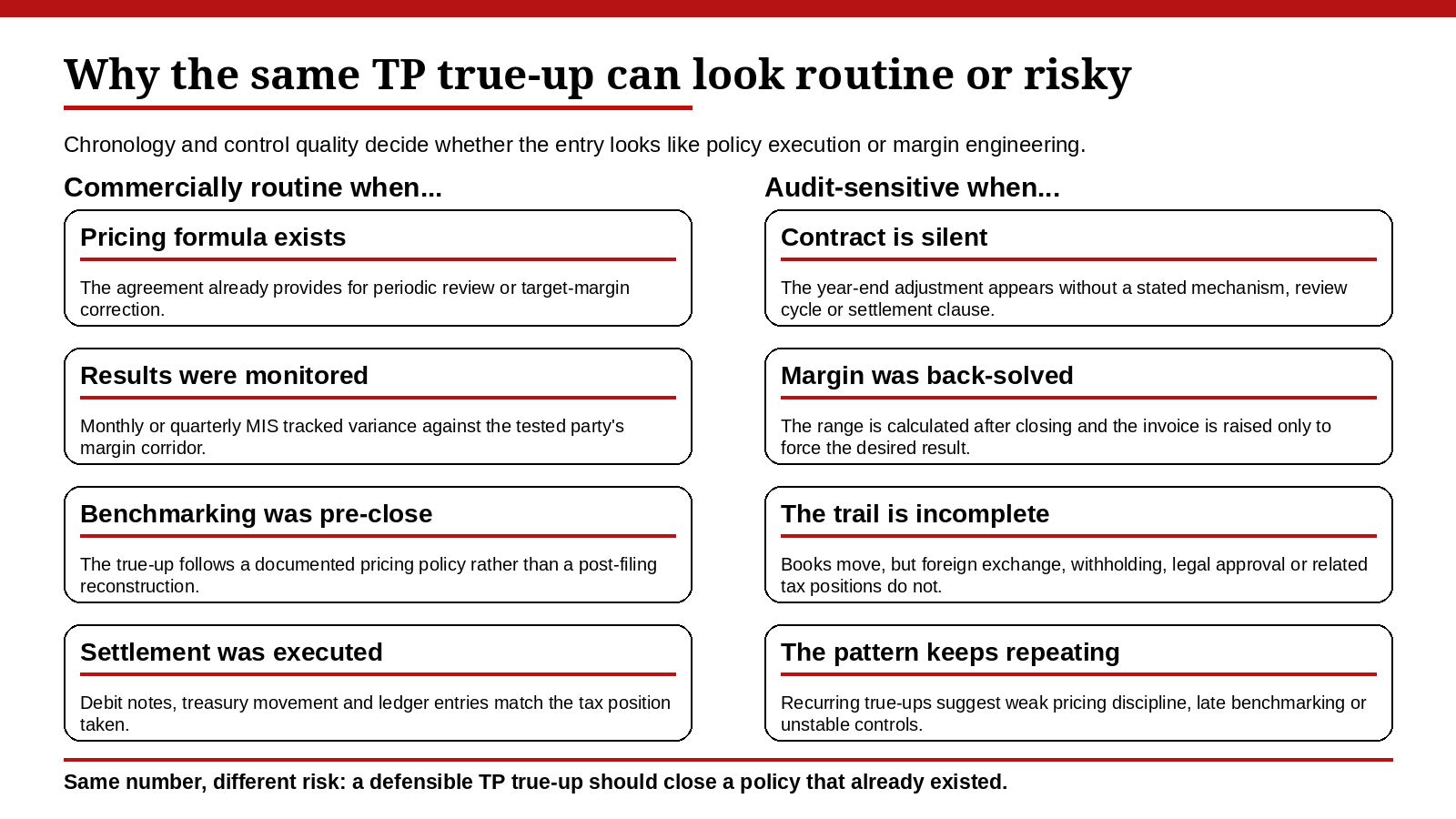

What Makes a TP True-Up Look Suspicious

The Indian problem is not the existence of a year-end adjustment; it is the absence of a believable mechanism behind it. Tax officers do not ask only whether the final number sits inside a range. They ask whether the true-up completes an already designed pricing arrangement or retrofits one after the year has closed. That distinction matters because India’s documentation rules require contemporaneous records of assumptions, policies, price negotiations and the adjustments made to align transfer prices with the arm’s length result. If the intercompany agreement says nothing about periodic re-pricing, if internal MIS never tracked the target margin, or if the debit note appears only after benchmarking is back-solved, the transfer pricing true-up begins to look less like commercial hygiene and more like result engineering.

Why Indian Scrutiny Is Structural, Not Episodic

India’s self-assessment architecture asks the taxpayer to take a position, support it in the accountant’s report and maintain a Rule 10D file that can survive sequence testing. Once a year-end adjustment changes the economics, the audit questions become chronological. When was the policy fixed? Who approved the mechanism? What event triggered the adjustment? Did the accounting entries, intercompany settlement, withholding position, foreign exchange paperwork and any related indirect-tax treatment move consistently with it? A TP true-up that fixes only the income-tax outcome while the rest of the transaction trail stands still is almost inviting a challenge.

The 92CE Problem: When a True-Up Becomes a Cash Issue

The stakes rise further because Indian law does not always let a transfer pricing adjustment remain a paper exercise. Where a primary adjustment increases Indian income, the excess money with the associated enterprise is generally expected to be repatriated within the prescribed period. If that does not happen, section 92CE can push the case toward imputed interest consequences or an additional-tax route. That changes the debate. A weak year-end TP true-up is no longer just a documentation defect. It can become a cash-management issue, a secondary-adjustment issue and, for cross-border groups, a double-tax problem if the counterparty jurisdiction does not move in step.

Why Transfer Pricing True-Ups Are Under More Scrutiny in 2025-2026

Policy is making this sharper, not softer. New Delhi is not retreating from transfer pricing discipline; it is sorting transactions into those that can be standardised and those that still need fact-heavy examination. Budget 2025 proposed a scheme to determine arm’s length price for a block period of three years as an alternative to yearly examination, and the implementation note says it takes effect from 1 April 2026 with rules to be framed by 30 September 2026. In parallel, CBDT expanded the scope of safe harbour in March 2025. Then Budget 2026 moved much further for IT services, announcing a common 15.5 percent safe-harbour margin, a threshold lifted to ₹2,000 crore, automated approval and continuity for five years, now reflected in the notified Income-tax Rules, 2026. The signal is plain: if a transaction fits a simplified corridor, compliance friction may fall; if it does not, the residual population must explain itself with far more precision.

What the APA Numbers Are Really Saying

The APA data points in the same direction. On 31 March 2026, CBDT said it had signed a record 219 Advance Pricing Agreements in FY 2025-26, taking the cumulative count to 1,034. That is not just an administrative milestone. It is evidence that taxpayers still value ex ante certainty enough to invest in structured pricing solutions, and that the administration is willing to expand certainty routes where the fact pattern is stable enough to be standardised. In that environment, repeated year-end transfer pricing true-ups in the ordinary audit population are more likely to be read as a risk marker. Not because true-ups are inherently abusive, but because recurring corrections may suggest that pricing discipline, benchmark refresh cycles or contract architecture have not kept pace with business scale.

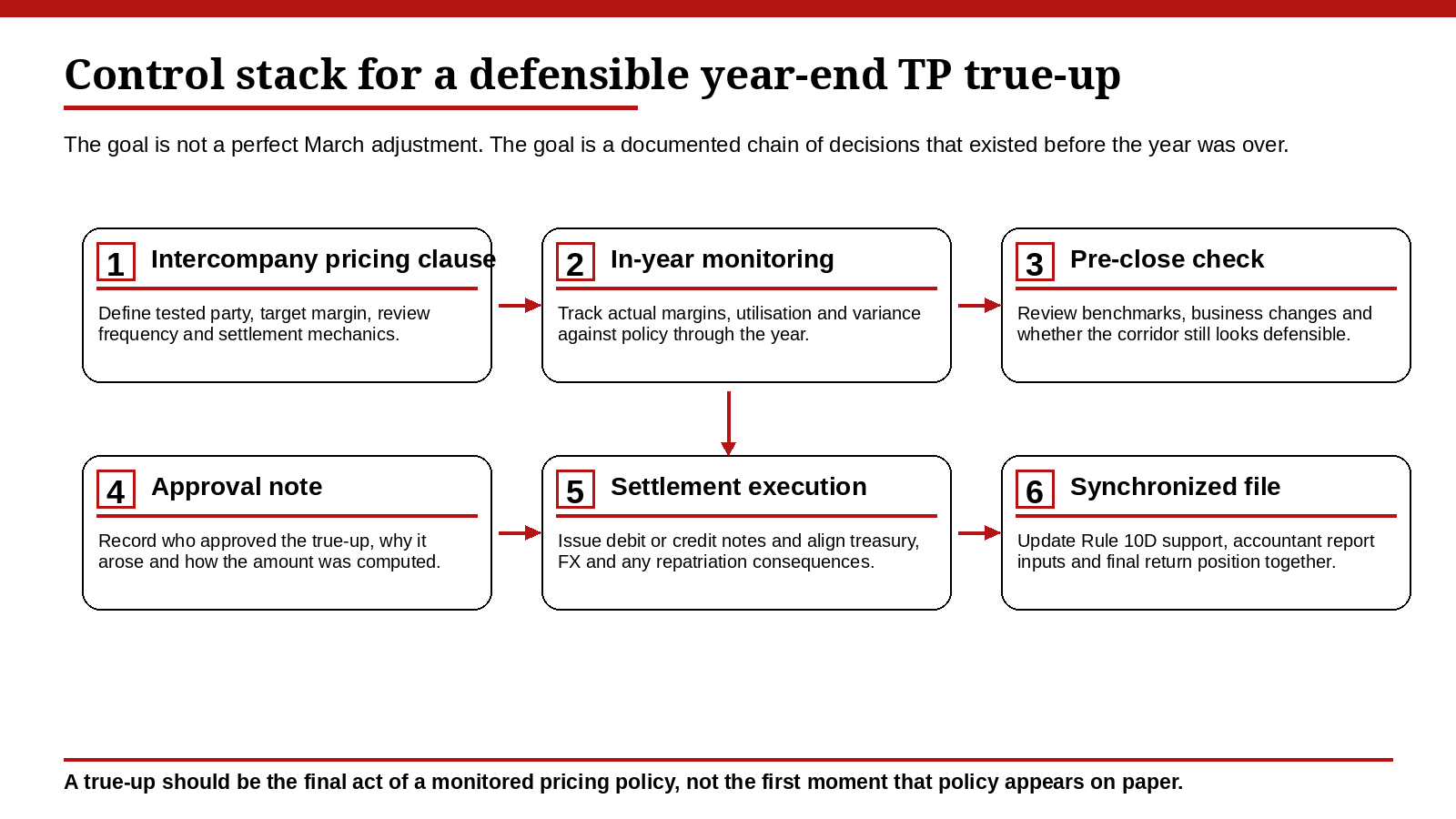

What a Defensible True-Up Control Stack Looks Like

A defensible transfer pricing true-up starts long before the last week of March. The intercompany agreement should define the pricing formula, the tested party, the target range or target point, the review frequency and the settlement mechanism. Finance should monitor actual margins through the year rather than waiting for the statutory file to be assembled. Deviations should create internal alerts, not year-end surprise. Management should be able to show why the chosen corridor remained reasonable, what changed commercially and why the final adjustment is the consequence of policy rather than the invention of policy. In practice, that means a control stack built around quarterly variance review, pre-close benchmarking checks, documented approval thresholds and clean debit-note or credit-note execution before the return position is frozen.

Who Ultimately Pays for Weak TP Controls

Tax professionals are being pushed out of the comfort zone of narrative benchmarking and into the harder work of control design, chronology management and settlement discipline. For corporates, better control around TP true-ups reduces controversy cost, working-capital stress and the risk that a small margin correction turns into a secondary-adjustment fight. For India’s urban middle class, especially in clusters built around GCCs, IT services and cross-border service delivery, the second-order effects are not abstract. Repeated transfer pricing friction eventually shows up in softer hiring plans, tighter margin management, delayed investment and slower compensation growth. Lower dispute drag, by contrast, leaves more room for cleaner capital allocation and steadier employment decisions.

Commercially Routine, Administratively High-Risk

So are year-end transfer pricing true-ups commercially routine or audit triggers by design? They are both. Commercially, they are often the inevitable result of pricing volatile businesses before all the facts are known. Administratively, they have become audit triggers by design because they concentrate the whole transfer pricing story into one observable event: agreement quality, monitoring discipline, settlement execution and documentary honesty. Companies that treat the true-up as the last step of a living pricing policy can usually defend it. Companies that treat it as a March journal entry designed to manufacture the right margin are effectively drafting the first paragraph of the tax authority’s case for them.

Sources & Data Points

- Income Tax Department – Transfer Pricing — Used for the statutory framework on transfer pricing documentation, Rule 10D, Form 3CEB obligations, and the section 92CE summary on repatriation and additional tax.

- OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations, 2022 — Used for the treatment of compensating adjustments and the cross-border frictions created by different approaches to year-end adjustments.

- Press Information Bureau – Budget 2025 direct-tax reform release — Used for the 2025 proposal to determine arm’s length price for a block period of three years and the stated policy intent to expand safe harbour.

- Implementation of Budget Announcements 2025-26 — Used for the implementation status: the block-period ALP scheme takes effect from 01.04.2026, rules are to be framed by 30.09.2026, and CBDT issued Notification No. 21/2025 on safe harbour expansion.

- CBDT Press Release dated 25 March 2025 on safe harbour amendments — Used for the March 2025 expansion of safe harbour scope, including the threshold increase from ₹200 crore to ₹300 crore and applicability to AY 2025-26 and AY 2026-27.

- Budget 2026-27 Speech — Used for the 2026 policy measures: common 15.5 percent safe-harbour margin for IT services, threshold increase to ₹2,000 crore, automated approval, five-year continuity, fast-track UAPA intent, and modified-return facility for associated entities of APA taxpayers.

- Income-tax Rules, 2026 notified on 20 March 2026 — Used for the notified safe-harbour rule text, including the 15.5 percent operating margin and ₹2,000 crore threshold for eligible information technology services, plus the five-year option structure.

- Press Information Bureau – CBDT signs record 219 APAs in FY 2025-26 — Used for the latest official APA data point: 219 APAs signed in FY 2025-26 and 1,034 APAs cumulatively since the programme began.