Marketing intangibles are not created by budget size alone. They emerge when Indian distributors do more than sell — when they shape demand, bear risk, and retain too little proof.

Marketing intangibles after the shortcut era

Marketing intangibles have a habit of disappearing inside ordinary P&L lines. A distributor books advertising, trade schemes, retailer support and launch costs. The group’s legal ownership of the trademark sits elsewhere. The file then moves too quickly from that fact to a conclusion: the Indian entity was merely selling products and the real brand value always belonged offshore. That jump is now harder to defend. In India distribution structures, the real question is not whether every rupee of AMP spend creates a separate intangible. It plainly does not. The real question is whether local value creation is being under-documented when the Indian entity does more than routine demand support.

That question matters because the shortcut era has already been cut back by the courts. In October 2025, the Delhi High Court again dealt with AMP disputes by noting that Sony Ericsson had already rejected the bright line test, and that AMP cannot be carved out for transfer pricing adjustment by using that discarded shortcut. In another October 2025 decision involving Amadeus India, the same court treated the AMP controversy as covered by its earlier jurisprudence, including Bausch & Lomb. The doctrinal direction is now familiar: Revenue must first prove an international transaction; it cannot simply infer one because the Indian distributor spent heavily on advertising or because the foreign associated enterprise may have enjoyed an incidental benefit.

That should have ended lazy arguments on both sides, but it hasn’t. Many taxpayers still answer the marketing intangibles issue with bare legal ownership language, as if ownership clauses alone settle the economics. Many audits still begin with spend patterns and instinctively ask who really built local demand. The harder truth sits in between. OECD guidance is explicit that generic references to “marketing intangibles” do not remove the need to identify the relevant intangible with specificity. The same guidance also makes clear that a distributor’s entitlement turns on its actual rights, functions, control of risk and expected returns — not on slogans like “limited-risk distributor” pasted over a fact pattern that may have outgrown the label.

What 2025-26 changed for the file

What changed in 2025-26 is not a special AMP code. It is the wider compliance mood around transfer pricing. CBDT signed a record 219 APAs in FY 2025-26, taking the cumulative count to 1,034, after the already strong 174 signed in FY 2024-25. The Finance Act 2026 also expanded safe harbour thresholds and simplified parts of the framework for certain technology services. None of this resolves AMP by itself. But it does tell taxpayers something important: the system is moving toward administrable certainty where facts are disciplined and repeatable. Vague narratives age badly in that environment. They create compliance friction precisely when the self-assessment architecture is demanding cleaner, more auditable files.

That demand for discipline is visible in the new form-and-rules architecture as well. The Income-tax Rules, 2026 came into force on 1 April 2026. Form 52, which now governs APA annual compliance reporting under the Income-tax Act, 2025, requires taxpayers to confirm compliance in a more structured way and ties reporting to concrete assumptions, computations and agreed terms. The Finance Bill memorandum for 2026 also widened section 169 mechanics so that an associated enterprise whose income changes because of an APA can file the relevant return or modified return. Read together, these are not AMP provisions. They are signals. Indian transfer pricing administration is putting greater weight on traceable economics, matched outcomes and operational consistency. Marketing intangibles disputes will inevitably be judged in that atmosphere.

Where local value creation slips out of the record

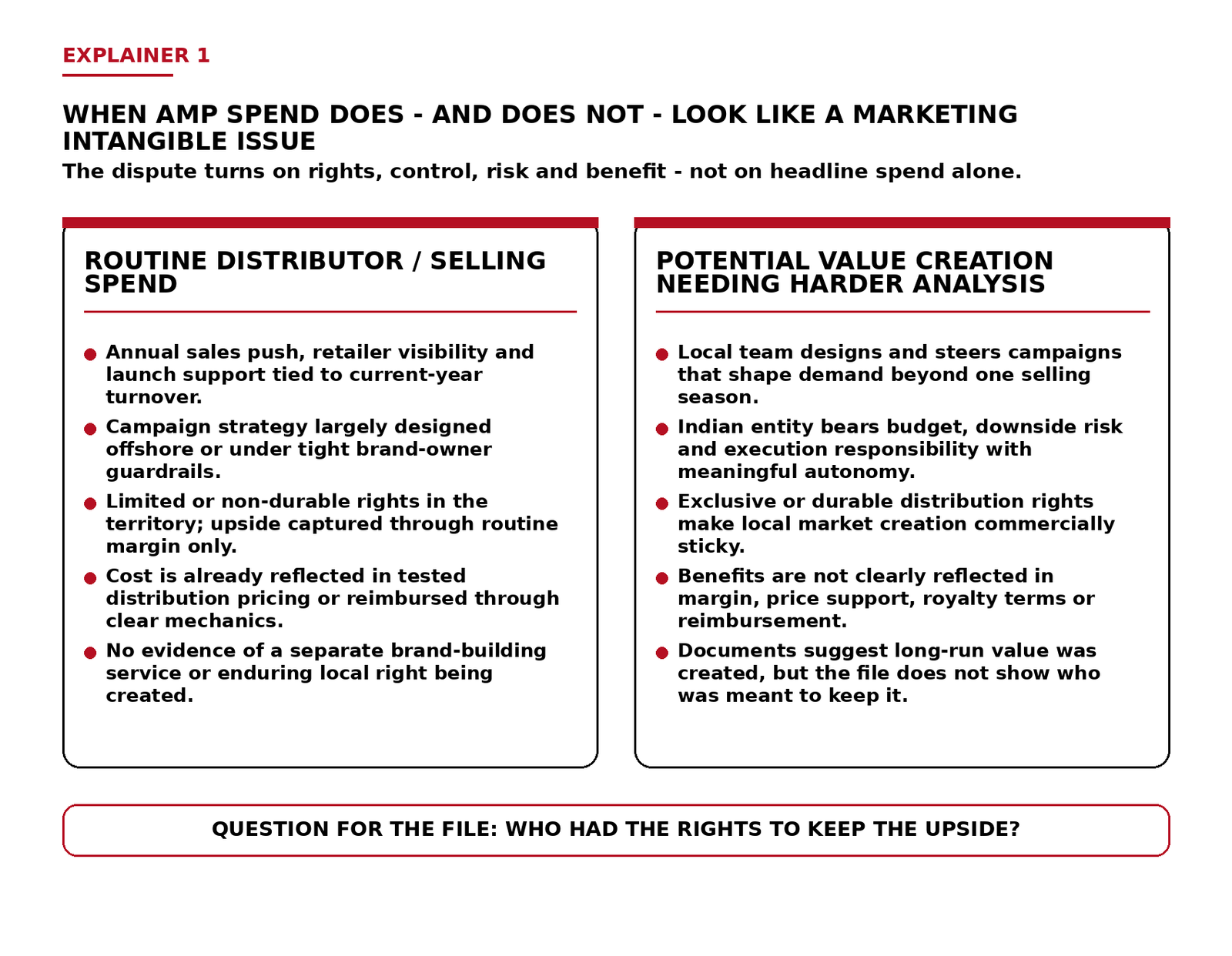

This is exactly where local value creation gets under-documented. The Indian file often contains invoices, agency agreements and a broad distribution contract, but not the evidence pack that answers the commercial question. Who approved the campaign? Who controlled the budget when sales disappointed? Who decided whether a launch would be cut, extended or scaled? Did the Indian entity merely execute a regional template, or did it shape market strategy for India’s channels, language, pricing sensitivities and retailer architecture? If the answer is the latter, then the issue is no longer just selling expense. It becomes a question of whether enduring local market value was created and, if so, whether the Indian entity’s compensation reflects that reality.

The under-documentation problem is often economic before it is legal. India is not a frictionless market. Distribution here can require local adaptation, channel education, retailer financing, repeated promotional investment and patient demand creation before a product becomes sticky. When an Indian distributor does that work under meaningful autonomy, bears downside risk and still keeps only a routine margin, the file starts looking thin. Not because every campaign creates a royalty-bearing intangible, but because the commercial upside may no longer line up with the conduct that produced it. That mismatch is where disputes begin. It is also where better documentation can prevent them before they reach litigation.

The cost of a thin evidence pack

The corporate consequences are larger than one adjustment line. If multinationals continue to under-document local value creation, they will either over-reserve for tax risk or over-defend fragile structures that do not survive scrutiny. Tax professionals then spend time reconstructing facts that should have been captured contemporaneously. Finance teams must explain why a supposedly routine distributor carried non-routine market-building burdens. The second-order effect does not stop inside the tax department. Where dispute risk hardens into pricing buffers, launch conservatism or heavier compliance overhead, some of that cost leaks into product pricing, channel incentives and consumer access. The Indian middle class rarely sees an AMP controversy, but it can still feel the tax incidence indirectly when companies price uncertainty into the market.

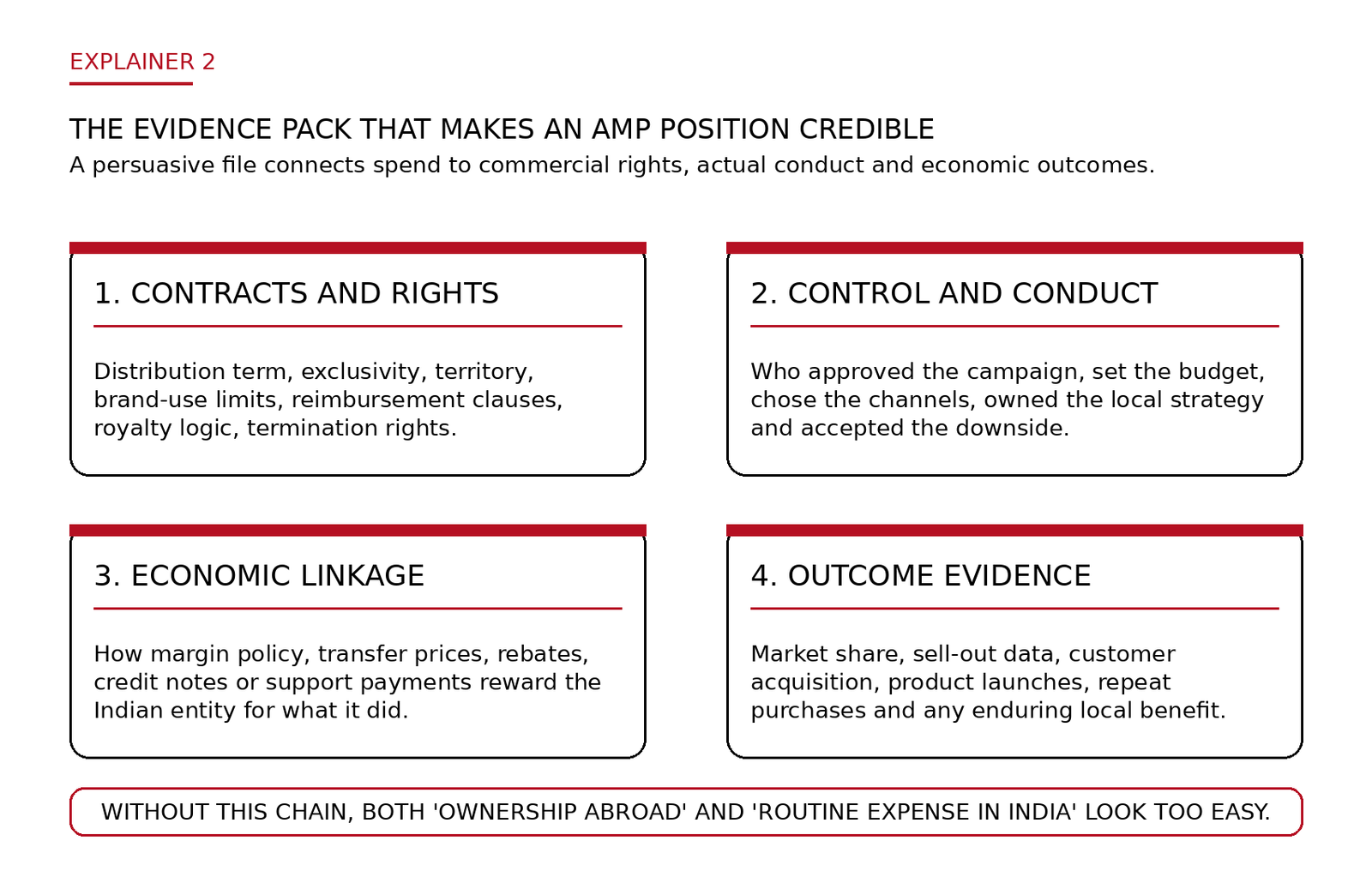

A mature response does not require theatrical restructuring. It requires adult precision. Taxpayers need distribution agreements that speak clearly about exclusivity, territory, brand-use rights, reimbursement logic, termination economics and the ownership of any market-specific outputs. They need board notes, approval chains and internal communications that show who actually controlled the spend and who accepted the risk. They need outcome evidence: market-share gains, repeat purchases, launch success, retailer expansion and the way those benefits were or were not reflected in transfer prices, rebates, support payments or margins. The Income Tax Department’s own transfer pricing documentation architecture already points in this direction by asking for the group’s strategy on the development, ownership and exploitation of intangibles, the legal owners, the important agreements and the related transfer pricing policies.

Marketing intangibles need proof, not posture

That is why the current marketing intangibles debate in India is less about finding a new formula than about abandoning old evasions. The bright line shortcut has been rejected. Generic ownership language is too thin. Generic references to “brand building” are too loose. What remains is a tougher but more honest discipline: identify the relevant rights with specificity, align them with actual conduct, and show how the economics rewarded that conduct. For Indian distributors, the safest file in 2026 is not the one that denies value creation in every case. It is the one that can document, without ornament, what the Indian entity actually did, what it was contractually allowed to keep, and why its compensation was arm’s length in that factual setting.

Sources & Data Points

- Press Information Bureau, Ministry of Finance, “CBDT signs record 219 Advance Pricing Agreements (APAs) in FY 2025–26” (31 March 2026). https://www.pib.gov.in/PressReleasePage.aspx?PRID=2247399&lang=1®=3

- Central Board of Direct Taxes, Press Release, “CBDT Signs 174 Advance Pricing Agreements in FY 2024-25” (31 March 2025). https://www.incometaxindia.gov.in/documents/20117/6490657/Press-Release-CBDT-Signs-174-Advance-Pricing-Agreements-in-FY-2024-25-dated-01-04-2025.pdf/20ddf3dd-5089-2699-e0d8-8e85777f3bf1?t=1762867556841

- Income Tax Department, “Form 52 – Frequently Asked Questions” (APA compliance reporting under section 169 / Rule 113). https://www.incometaxindia.gov.in/documents/d/guest/form-52-faqs

- Central Board of Direct Taxes, Notification, Income-tax Rules, 2026, dated 20 March 2026. https://www.incometaxindia.gov.in/documents/d/guest/en-notified-it-rules-2026-20-03-2026-pdf

- Income Tax Department, “Income-tax Act, 2025 [as amended by Finance Act, 2026]”. https://www.incometaxindia.gov.in/documents/d/guest/income_tax_act_2025_as_amended_by_fa_act_2026-pdf

- Union Budget 2026-27, Memorandum Explaining the Provisions in the Finance Bill, 2026. https://www.indiabudget.gov.in/doc/memo.pdf

- Income Tax Department, official Transfer Pricing page and documentation architecture. https://www.incometaxindia.gov.in/transfer-pricing

- Delhi High Court, ITA 505/2025, judgment dated 10 October 2025. https://delhihighcourt.nic.in/app/showFileJudgment/VKR09102025ITA5052025_151022.pdf

- Delhi High Court, ITA 511/2025, judgment dated 10 October 2025 (Amadeus India). https://delhihighcourt.nic.in/app/showFileJudgment/75310102025ITA5112025_130641.pdf

- Delhi High Court, Bausch & Lomb Eyecare (India) Pvt. Ltd. v. ACIT, judgment dated 23 December 2015. https://delhihighcourt.nic.in/app/downloadOrderbByDate/ITA/676/2014/23-12-2015

- OECD, Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations 2022. https://www.oecd.org/content/dam/oecd/en/publications/reports/2022/01/oecd-transfer-pricing-guidelines-for-multinational-enterprises-and-tax-administrations-2022_57104b3a/0e655865-en.pdf

- OECD, Guidance on Transfer Pricing Aspects of Intangibles. https://www.oecd.org/content/dam/oecd/en/publications/reports/2014/09/guidance-on-transfer-pricing-aspects-of-intangibles_g1g46cf9/9789264219212-en.pdf