DEMPE analysis now separates serious transfer pricing files from decorative ones. As audits mature, template-heavy narratives on intangibles are turning from comfort documents into adjustment bait.

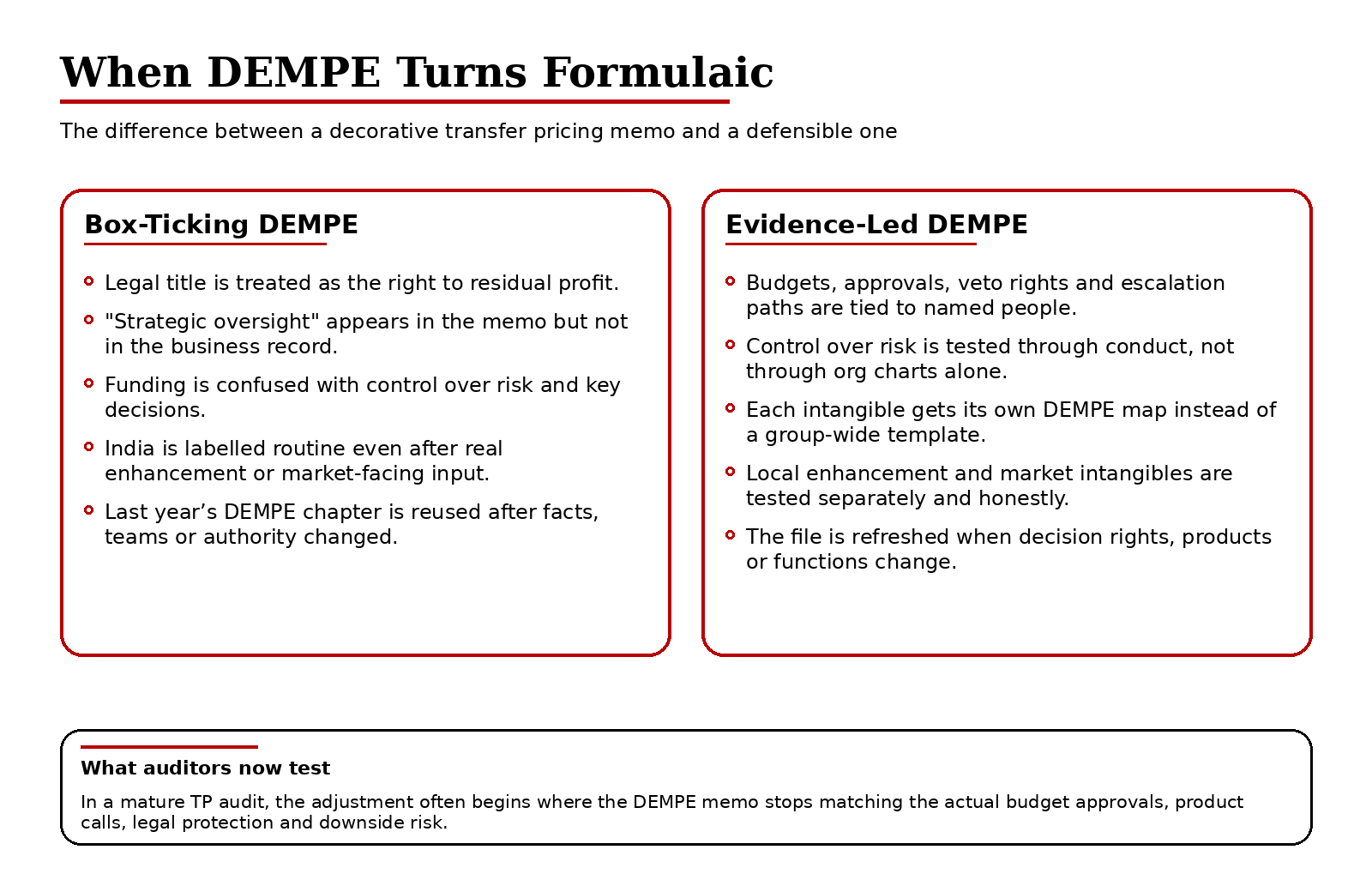

DEMPE analysis is supposed to answer a commercial question, not decorate a local file. Who actually developed the intangible? Who improved it, protected it, paid for failure, and decided when to scale or kill the asset? Yet too many transfer pricing files in India and across large multinational groups now read as if the answer can be produced by template. Development sits with one entity because the R&D centre is there. Protection sits with another because legal title sits there. Exploitation sits almost everywhere because everyone “supports” revenue. It looks tidy. It also looks increasingly unsafe.

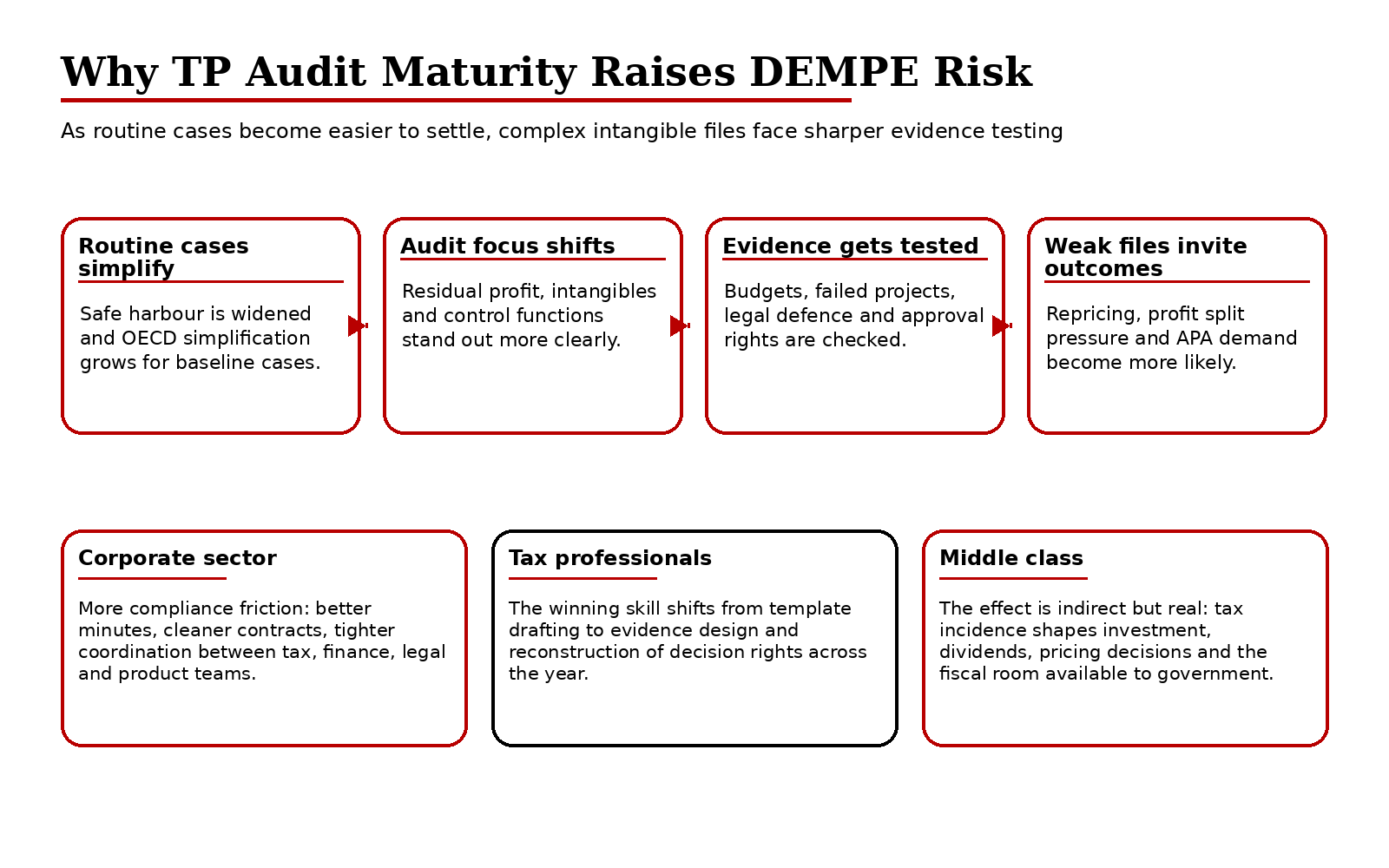

That shift matters because the enforcement environment no longer rewards tidy narratives by default. India closed FY 2025-26 with a record 219 APAs, including 84 bilateral APAs, taking the cumulative tally to 1,034. A year earlier, the number was already a record 174. At the same time, the Union Budget’s Receipt Budget put corporation tax at a revised estimate of ₹11.09 lakh crore for 2025-26 and a budget estimate of ₹12.31 lakh crore for 2026-27. Those numbers do not prove aggression. They do signal institutional maturity and fiscal stakes. This is what TP audit maturity looks like in practice. In that setting, a DEMPE note that merely recites legal ownership, broad job titles and a benchmark margin starts to look less like compliance and more like compliance theatre.

Why DEMPE analysis is now being tested harder

The OECD’s own architecture never intended DEMPE to be a box-ticking exercise. Its guidance says that members of a group performing functions related to the development, enhancement, maintenance, protection and exploitation of intangibles must be compensated for those contributions. It goes further: if the legal owner neither performs nor controls those functions, it is not entitled to the residual return simply because its name sits on the registration certificate. That was always the intellectual centre of DEMPE. The point was to look through labels and find control, capability, risk assumption and economically significant conduct.

Once that principle is taken seriously, the weakness of formulaic files becomes obvious. Many groups still prepare DEMPE chapters as a dressed-up FAR analysis with better nouns. “Strategic oversight” gets assigned to the parent. “Execution support” goes to India. “Market exploitation” goes to distributors. But when a transfer pricing audit asks who approved the R&D budget, who set the product roadmap, who decided to litigate an infringement claim, who bore the cost of failed trials, or who had authority to redirect engineers toward a new commercial use, the memo often stops being persuasive. The verbs in the document do not line up with the verbs inside the business.

India’s own documentation rules make that mismatch dangerous. Rule 10D requires far more than a conclusion. It asks for the ownership structure, a profile of the group, the nature and value of transactions, a FAR analysis, the assumptions that affect pricing, and authentic supporting material. It also insists that documentation be contemporaneous and refreshed when there is a significant change in facts. In a self-assessment architecture, that means a taxpayer cannot safely recycle last year’s DEMPE story when product leadership shifted, when local engineers began making market-specific enhancements, or when a treasury entity kept funding an intangible but stopped controlling the downside risk.

Where the real danger lies

The danger is not that tax officers have suddenly discovered DEMPE. The danger is that routine transfer pricing is being simplified elsewhere, which leaves more administrative attention for hard cases. The OECD’s 2025 consolidated report on Amount B is explicit about the policy direction: simplify baseline distribution cases, cut compliance costs, and enhance tax certainty. India’s March 2026 APA press release points in the same direction domestically. The Finance Act 2026 changes to Safe Harbour Rules raise the threshold sharply, consolidate several tech-service segments into a single category, and aim for a more automated framework. That is sensible policy. But it also means the harder questions will stand out more starkly. Intangibles, control functions and residual profit allocation will not be able to hide inside a sea of routine disputes.

That has second-order effects well beyond the tax department and the in-house tax team. For the corporate sector, the immediate cost is higher compliance friction: more interviews, better minute-keeping, tighter intercompany drafting, cleaner decision logs, and closer alignment between tax, finance, legal and product functions. For tax professionals, the job shifts from benchmarking and narrative assembly to evidence design. The strongest adviser in a DEMPE controversy may not be the one with the largest database, but the one who can reconstruct decision rights over three years of product development. For the Indian middle class, the link is indirect but real. When transfer pricing disputes reprice residual profit, the tax incidence does not vanish into the air; it feeds into dividends, investment decisions, executive compensation, and eventually the fiscal room available to the state.

What a defensible DEMPE analysis looks like in 2026

A defensible DEMPE analysis in 2026 is usually narrower, messier and more honest than the polished versions many groups still circulate. It accepts that different intangibles inside the same business may have different DEMPE maps. A legal owner can still retain meaningful returns, but only where it can show real control over outsourced functions and real assumption of economically significant risk. An Indian entity can still be routine, but only where the evidence shows routine conduct rather than merely a routine label. And where multiple entities make non-trivial contributions, the file should say so early rather than hoping a one-sided method can carry a fact pattern that is already drifting away from a simple arm’s length price analysis and toward profit split logic.

The practical answer, then, is not to abandon DEMPE analysis. It is to stop flattering it. A serious file should map rights to people, people to decisions, decisions to documents, and documents to money. It should show who approved budgets, who owned failures, who authorised legal protection, who directed enhancement, and who had the power to exploit the asset commercially. It should also explain what changed during the year. That last point matters more than many taxpayers admit. Once DEMPE becomes formulaic, it stops being a risk-control tool and starts becoming evidence for the other side.

The irony is that India’s transfer pricing system now offers more certainty routes than before, not fewer. APA signings are at a record high, safe harbours have been widened for routine categories, and the transition to the Income-tax Act, 2025 expressly preserves existing APAs so long as they are consistent with the new law. That is the backdrop against which DEMPE analyses will now be read. Not as theory. Not as literature. As proof. And in a mature audit environment, proof that feels mass-produced is often the most dangerous proof of all.

Sources & Data Points

Used for the FY 2025-26 APA record: 219 APAs signed, 84 BAPAs, and 1,034 cumulative APAs since inception; also used for the Safe Harbour reform references.

Used for the FY 2024-25 APA data point: 174 APAs, including 65 BAPAs, and India’s first MAPA.

Used for India’s official description of transfer pricing, TPO referral mechanics, the Most Appropriate Method framework, Rule 10D documentation requirements, and the policy logic of safe harbour.

Used for the 2026 transition point that an APA signed under the old Act continues to bind so long as it is not inconsistent with the new Act.

Used for the core DEMPE principles on control, legal ownership, residual returns, and compensation for functions, assets and risks related to intangibles.

Used for the current OECD policy direction toward simplification of baseline distribution cases, lower compliance costs and higher tax certainty.

Used for the corporation tax figures cited in the article: revised estimate of ₹11.09 lakh crore for 2025-26 and budget estimate of ₹12.31 lakh crore for 2026-27.