MFN clauses were sold as parity devices inside India’s treaty network. Recent disputes show they protect only when drafting, timing, notification and state practice point the same way.

MFN clauses looked cheap on paper because the real price sat in interpretation

MFN clause disputes rarely begin in court. They begin in spreadsheets. In many cross-border dividend and licensing structures, the decisive assumption was tucked into a protocol footnote: if India later gave a better withholding deal to another OECD state, the earlier treaty partner could claim the same concession. That sounded neat and symmetrical. For years, taxpayers treated the clause as a built-in ratchet. If a later India treaty with Slovenia, Lithuania or Colombia lowered dividend withholding or narrowed the scope of royalties or fees for technical services, the earlier France, Netherlands or Switzerland treaty, they argued, should move with it. That belief lowered tax incidence, improved post-tax returns, and made treaty planning look almost mechanical.

The attraction of the MFN clause was always parity, not generosity

An MFN clause in a tax protocol is not charity. It is a parity device. The treaty partner wants comfort that it will not be left commercially worse off if India later offers better source-state limits to another comparable jurisdiction. That is why the drafting often sounds automatic. The old France protocol said the same rate or restricted scope would also apply; the Netherlands protocol used similar language. Read alone, those words invited taxpayers to think the concession travelled on its own. But tax treaties do not operate in India as floating intentions. They work through a domestic legal gateway. That tension — between elegant drafting and India’s statutory method of giving treaty effect — sat quietly in the background until dividend withholding disputes forced it into the open.

What the Supreme Court actually did to the MFN clause debate

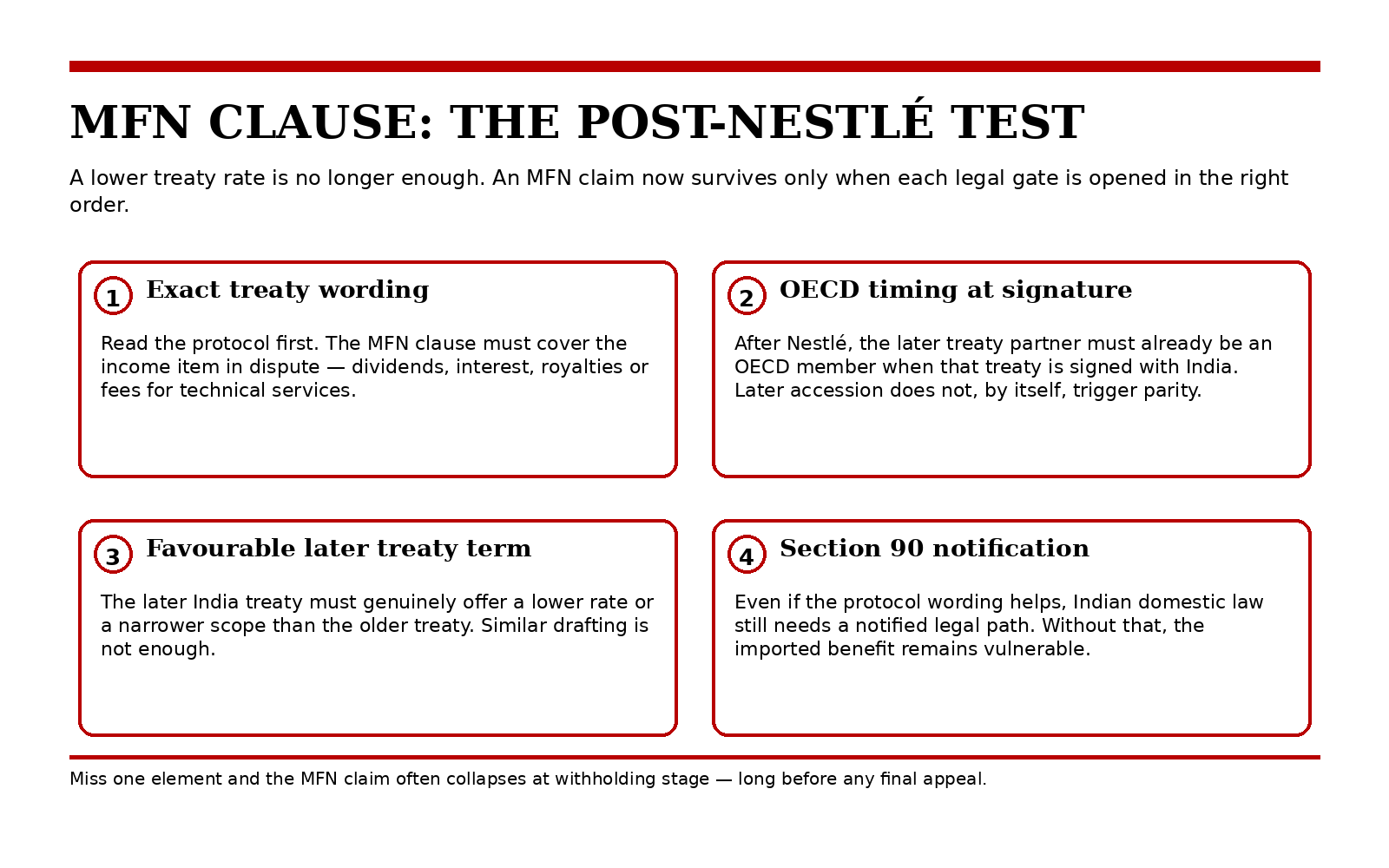

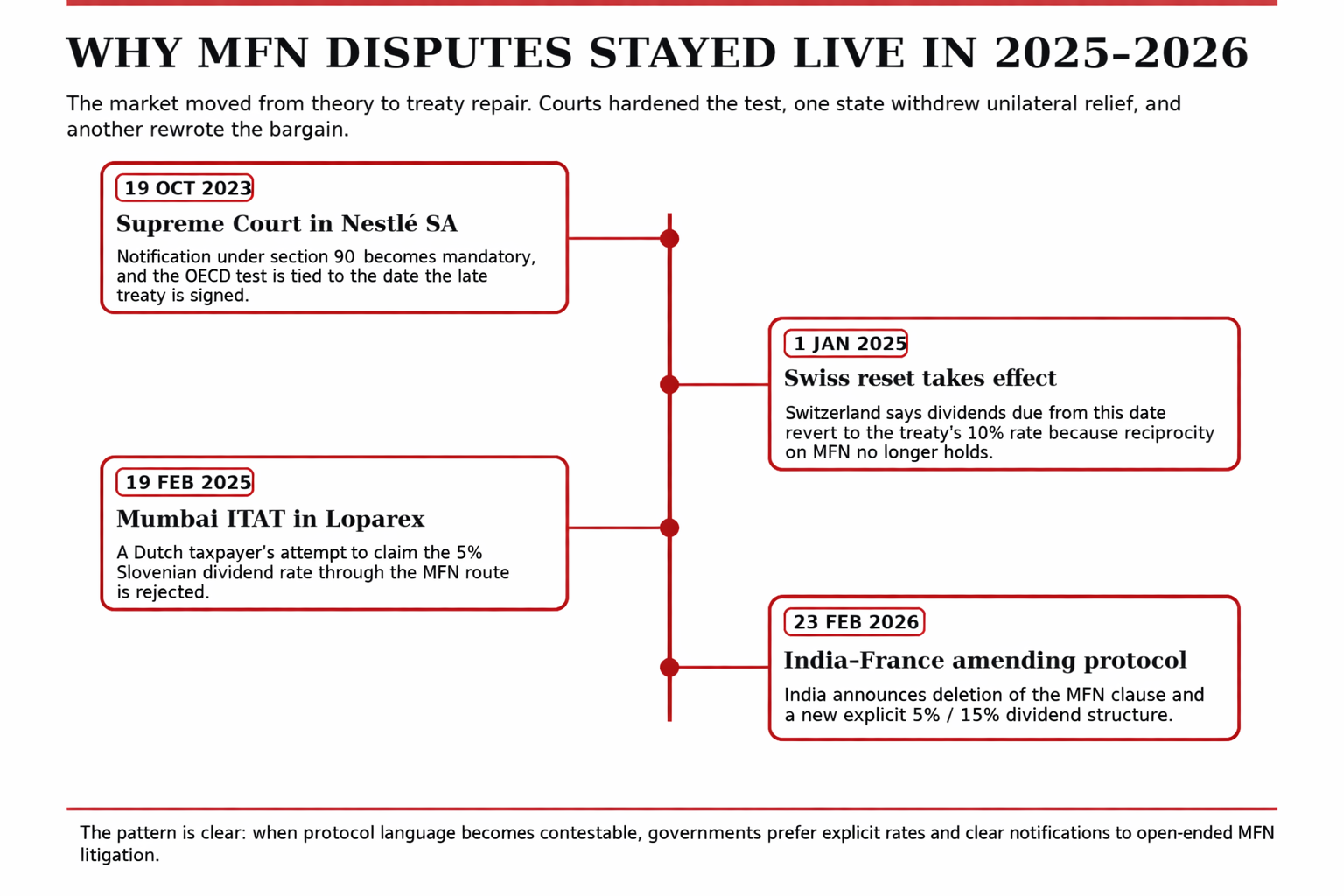

The Supreme Court’s October 19, 2023 judgment in Assessing Officer (International Taxation) v. Nestlé SA changed the terrain at both pressure points. First, it held that a notification under section 90(1) is a mandatory condition for giving effect to a DTAA term or protocol change that alters existing law. Second, it held that the expression “is a member of the OECD” carries present signification, so the relevant third state must be an OECD member when it enters into the treaty with India, not on some later accession date. It meant later OECD accession by countries such as Lithuania or Colombia could not, by itself, trigger imported benefits for older treaties.

The real drafting illusion was the belief that treaty text could outrun domestic incorporation

This is where the phrase “drafting illusion” earns its keep. The problem was not that MFN clause drafting was meaningless. The problem was that taxpayers often treated drafting as self-executing. It wasn’t. A protocol may be an integral part of a treaty, but the concession being imported from a later treaty still changes the operative position applied by the Indian tax administration. Under the court’s approach, that movement requires a conscious domestic act, not merely a clever textual bridge. Once that point is accepted, many older MFN clause models look less like hard treaty protection and more like contingent rights that depend on notification discipline, the precise income item involved, and the chronology of OECD membership.

Why 2025 proved the controversy was still cash-live, not academic

The 2025 Mumbai Tribunal order in Loparex Holding BV made that clear. The taxpayer sought to use the India-Netherlands protocol to import the 5 per cent dividend rate available under the India-Slovenia treaty for a qualifying shareholder. The claim failed. Once withholding agents, finance teams and tax officers read MFN clause claims as litigation-sensitive rather than administratively settled, behaviour changes. Companies withhold conservatively. Refund cycles lengthen. Gross-up clauses bite harder. Treasury teams start treating treaty relief as probabilistic rather than bankable. That increases compliance friction across the self-assessment architecture, even before a final court loss arrives.

The OECD timing point cut deeper than many planners expected

The OECD-membership condition was not a semantic sideshow. It went to the structure of the bargain. The India-Slovenia treaty did provide a 5 per cent dividend rate for a company holding at least 10 per cent of the payer’s capital, and that was precisely the kind of lower rate taxpayers wanted to import. But once courts insist that the third state must already be an OECD member when its treaty with India is signed, the field narrows sharply. The MFN clause stops acting like a rolling escalator that updates older treaties whenever a later partner joins the OECD. Instead, it behaves like a locked clause tied to the legal and institutional facts existing at signature. That is a much more static instrument than the market had priced in.

France and Switzerland sent the clearest 2025–2026 market signals

It came from states rewriting or retracting positions. Switzerland announced in December 2024 that, because India interprets the MFN clause differently and does not apply it, Switzerland would revert to the prior 10 per cent dividend rate from January 1, 2025 to restore reciprocity. Then came France. On February 23, 2026, India announced an amending protocol with France that deletes the MFN clause from the protocol altogether, while replacing the old single 10 per cent dividend rate with a split 5 per cent and 15 per cent structure. That is what serious treaty systems do after years of interpretive warfare: they stop hinting and start drafting expressly.

What this means for companies, advisers and the Indian middle class

For companies, the lesson is blunt. MFN clause positions can no longer be dropped into a memo as if protocol wording alone settles the answer. Advisers now have to map treaty text, notification history, OECD status at the time of signing, beneficial ownership, and the exact income category. For tax professionals, that raises the marginal utility of careful treaty reconstruction and lowers the value of old template opinions. For the Indian middle class, the effect is indirect but real. Cross-border tax uncertainty raises the cost of capital, increases pricing buffers in technology and licensing contracts, and slows clean profit repatriation. That may flatter short-run tax buoyancy, but it is a poor route to durable certainty. A stable fiscal glide path needs clarity, not rolling controversy.

MFN clauses still offer protection, but only when the protection is made real

So are MFN clauses dead? No. They can still matter where the clause is tightly drafted, the later treaty fits the income item in question, the third state satisfies the OECD condition at the right time, and India has taken the domestic steps needed to give the result legal effect. But that is narrow protection, not the drafting magic many taxpayers once assumed. The post-Nestlé position is harsher, yet cleaner. Real treaty protection now comes less from interpretive optimism and more from explicit renegotiation, precise notifications and a better match between international commitments and domestic implementation. Recent disputes have done something useful: they have forced the market to stop confusing treaty aspiration with enforceable relief

Sources & Data Points

Official public sources used for the article’s legal conclusions, dates, treaty text and current treaty developments are listed below.

- Supreme Court of India — Assessing Officer (International Taxation) v. Nestlé SA, judgment dated 19 October 2023

https://api.sci.gov.in/supremecourt/2022/6394/6394_2022_8_1502_47832_Judgement_19-Oct-2023.pdf

Used for the holdings that section 90(1) notification is mandatory for operative treaty change and that OECD status is tested at the time the later treaty is entered into with India.

- Income Tax Department — France: Comprehensive Agreements

https://www.incometaxindia.gov.in/w/france-comprehensive-agreements-1

Used for the original India–France protocol text containing the MFN clause.

- Income Tax Department — Netherlands: Comprehensive Agreements

https://www.incometaxindia.gov.in/w/netherlands-comprehensive-agreements-1

Used for the original India–Netherlands protocol text containing the MFN clause.

- Income Tax Department — Slovenia: Comprehensive Agreements

https://www.incometaxindia.gov.in/w/slovenia-comprehensive-agreements-1

Used for the 5% dividend rate available to a company holding at least 10% of the payer’s capital.

- Income Tax Appellate Tribunal, Mumbai — Loparex Holding BV, order dated 19 February 2025

https://itat.gov.in/public/files/upload/1741159150-6rzSKK-1-TO.pdf

Used for the 2025 tribunal-level application of the post-Nestlé MFN approach in a dividend withholding dispute.

- Press Information Bureau, Ministry of Finance — India and France sign Amending Protocol to update DTAC, dated 23 February 2026

https://www.pib.gov.in/PressReleseDetailm.aspx?PRID=2231751&lang=2®=3

Used for the deletion of the MFN clause from the India–France protocol and the new 5% / 15% dividend structure.

- Swiss Federal Department of Finance / SFI — Switzerland suspends unilateral application of the MFN clause, statement dated 11 December 2024

https://www.estv.admin.ch/dam/en/sd-web/bifa29jbp2im/int-laender-indien-suspension-mfn-en.pdf

Used for the Swiss decision to revert to the treaty’s 10% dividend rate with effect from 1 January 2025 due to lack of reciprocity.