Remote work permanent establishment risk now turns less on stamped passports than on where key functions sit, who shapes contracts, and how long “temporary” delivery models are allowed to harden.

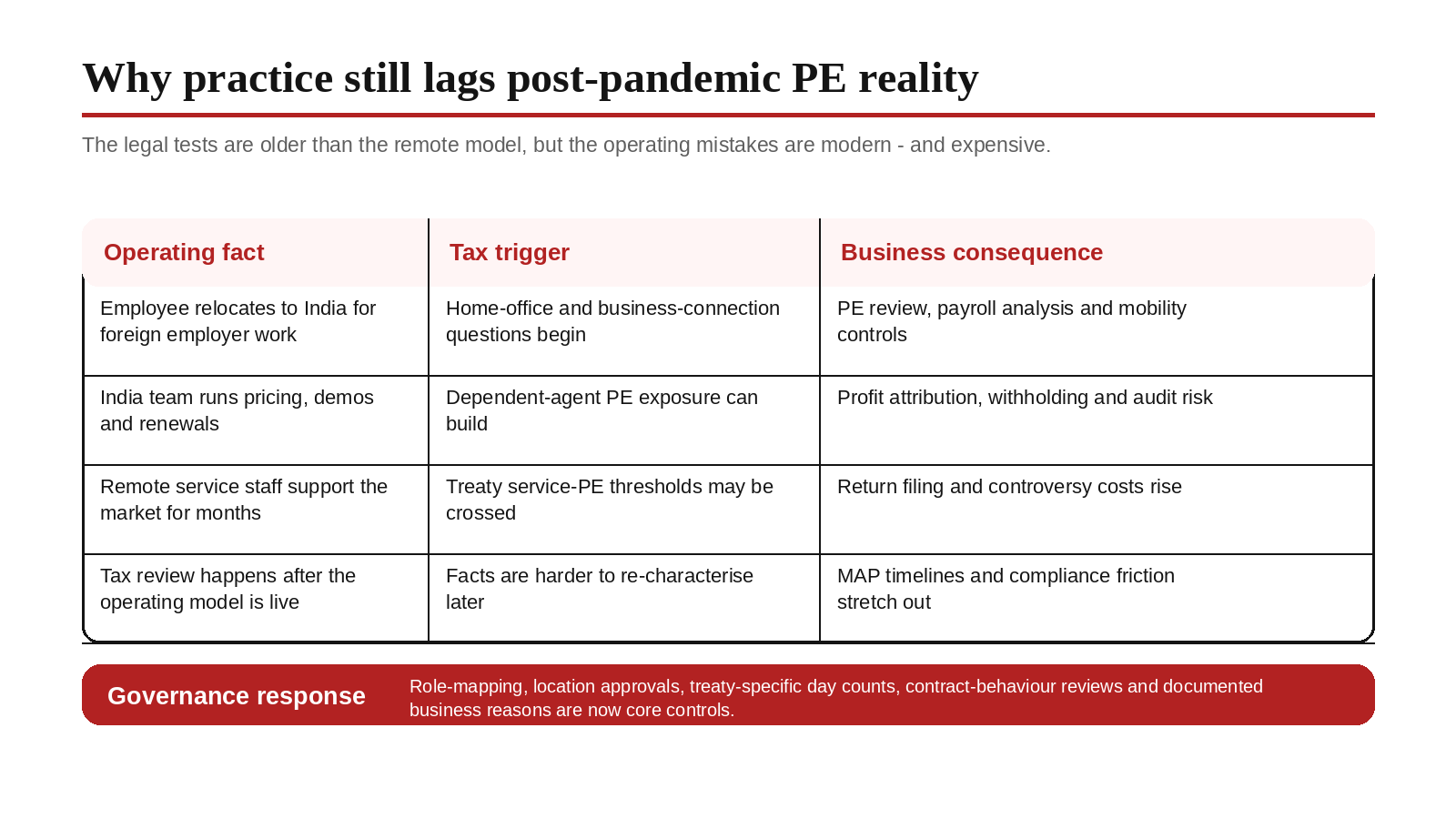

Remote work permanent establishment risk used to be treated as a pandemic footnote. It isn’t one anymore. The old instinct was simple: no branch, no leased office, no regular travel, so no serious tax presence problem. That instinct is stale. Cross-border delivery is lighter on infrastructure but heavier on people functions. Sales engineers can shape terms from a flat in Bengaluru. Product specialists can support a market for months without entering a client’s office. The exposure has not vanished. It has moved from visible premises to less visible operating facts.

The pandemic exception has narrowed

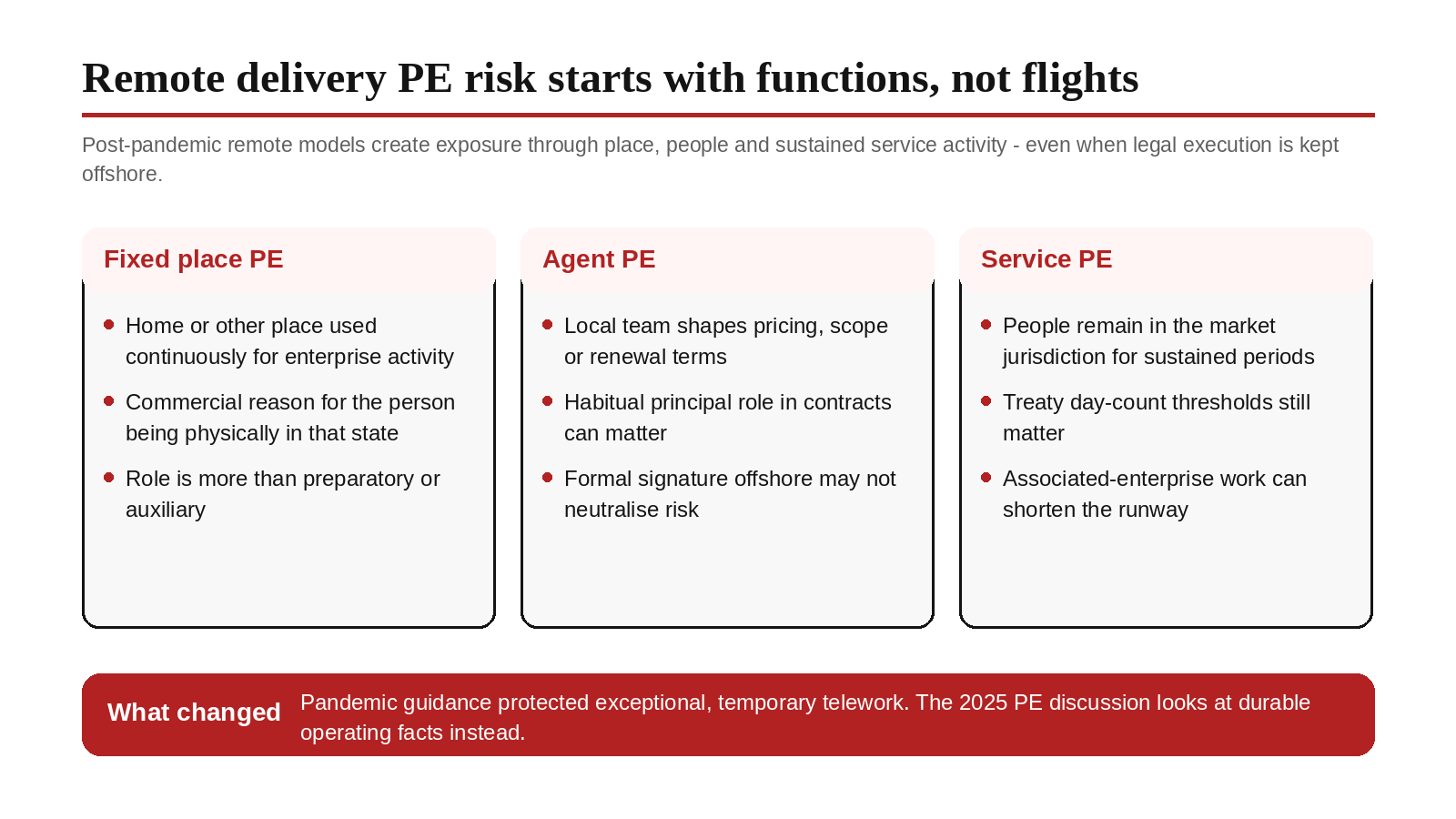

The comfort many companies drew from pandemic-era guidance was always narrower than they admitted. The OECD’s January 2021 guidance said the exceptional and temporary change in where employees worked because of COVID-19 should not create new permanent establishments; teleworking from home due to public-health measures was treated as an extraordinary fact pattern, not an enterprise choice. That shield was built for compulsion, not design. The OECD’s 2025 update moves the discussion to recurring cross-border work from homes and other locations, assessed on current facts rather than emergency assumptions. Once remote delivery becomes part of the operating model, the analysis gets much less forgiving.

In that newer framework, what matters is not the slogan of “work from anywhere” but the anatomy of presence. The 2025 OECD commentary says a home or other relevant place does not automatically become the enterprise’s place of business simply because an employee works there. Yet continuous use over an extended period, the share of total working time spent there, and the commercial reason for the person being physically present in that state all matter. A notable feature is its general indication that where an individual works from that place for less than 50 per cent of total working time over a twelve-month period, it would generally not be treated as the enterprise’s place of business. Useful benchmark, yes. Safe harbour, no.

Why India remains a harder PE jurisdiction

India is a difficult jurisdiction in which to rely on OECD comfort language as a full defence. In the same 2025 update, India formally records disagreement with the new home-office thresholds and conditions, taking the view that an individual’s home can be at the disposal of the enterprise for Article 5 purposes. That matters because many multinational policies assume treaty practice will converge around a single OECD reading. It may not. If meaningful business functions are being performed from India for a foreign enterprise, the absence of a brass-plate office will not carry the weight it once did.

Domestic law points the same way. The Income-tax Act, 2025, as amended by the Finance Act, 2026, keeps a broad “business connection” architecture. It preserves SEP, but it also keeps the classic people-based triggers: a person acting for a non-resident who habitually concludes contracts, habitually plays the principal role leading to contract conclusion, habitually maintains stock for regular delivery, or habitually secures orders can create exposure. That matters because remote delivery models often separate formal signature from real commercial behaviour. The salesperson may never sign. The India-based account lead may merely “coordinate”. But if those functions shape the commercial outcome repeatedly, the tax analysis changes.

The treaty side is no softer. The Multilateral Instrument’s Article 12 widened the dependent-agent PE standard beyond cases where a person formally signs contracts, extending it to situations where someone habitually plays the principal role leading to contracts that are routinely concluded without material modification. Groups centralise legal execution in one country and assume the tax risk stays there. In practice, pricing calls, scoping discussions, technical demos, renewal negotiations and implementation promises are often carried out somewhere else. When those functions sit in India, the claim that “contracting happens offshore” starts to look fragile.

Remote delivery can still create service PE

The same gap appears in service PE analysis. Many of India’s treaties can tax sustained services without a traditional fixed office. The India-US treaty treats the furnishing of services through employees or other personnel as a PE if activities continue for more than 90 days in any twelve-month period, or if the services are performed for a related enterprise. The India-UK treaty also contains a service-PE clause, with a 90-day test and a shorter 30-day rule for associated enterprises. That means a group can have no branch with external-facing contracts and still walk into PE risk because its remote delivery model leaves people in the market jurisdiction carrying out sustained service functions.

Where practice still lags

This is where practice remains behind reality. HR asks whether an employee may relocate. Business asks whether the client can still be served. Finance asks whether billing can continue from the existing entity. Tax often arrives late, and when it does, the discussion is reduced to day counts or signing authority. That is too narrow for 2026. India’s 2024 MAP statistics show that attribution or allocation cases – the category that includes profits attributable to a PE – remain slow to resolve, with bilateral closures for post-2015 cases averaging a little over 46 months. Get the model wrong and the price is years of uncertainty, double-tax risk and documentation drag.

The second-order effects are already visible. Larger multinationals are building location governance and role-mapping around remote work. Mid-sized groups are more exposed because they still treat remote delivery as an efficiency choice rather than a tax design choice. For Indian tax professionals, the work is shifting from treaty recital to functional forensics: who negotiated, who supervised, who delivered, who maintained the customer relationship, and where those acts occurred. For professionals who want geographic flexibility, the result is tighter mobility approvals, employer-of-record structures, altered compensation design or blunt bans on working from India for foreign employers. Tax rules do not kill flexibility. They make unstructured flexibility expensive.

PE still bites before the theory does

India’s wider nexus architecture reinforces the point. The 2026 rules prescribe SEP thresholds of Rs 2 crore of payments and 300,000 users, showing that India still thinks beyond physical premises. Yet for many treaty-protected businesses, classic PE questions will bite earlier and more concretely than SEP debates. A home office, an India-based deal team, a support function that becomes customer-critical, or a services presence that quietly crosses treaty day thresholds can create immediate controversy. In a services-heavy economy, that is not peripheral. The Department of Commerce estimates India’s services exports at USD 387.93 billion in April-February 2025-26, up from USD 351.93 billion a year earlier. The BLS said 33 per cent of employed people worked at home on days worked in 2024, while Eurostat said 52.9 per cent of EU enterprises with at least 10 employees held remote meetings in 2024.

The serious answer, then, is that practice has caught up only halfway. Most tax leaders now accept that remote work can create PE risk. Far fewer have rebuilt governance around that insight. The question is no longer whether a company has a formal office in India or whether someone flew in last quarter. It is whether the enterprise has allowed commercially meaningful functions to settle in a jurisdiction while preserving legal forms designed for a different era. Once that happens, the gap between “remote support” and “taxable presence” starts to collapse.

Sources & Data Points

https://www.oecd.org/content/dam/oecd/en/publications/reports/2025/11/the-2025-update-to-the-oecd-model-tax-convention_c7031e1b/5798080f-en.pdf

Used for the updated home-office PE commentary, the 50% working-time benchmark in the new commentary, and India’s stated disagreement with parts of that approach.

https://www.oecd.org/content/dam/oecd/en/publications/reports/2021/01/updated-guidance-on-tax-treaties-and-the-impact-of-the-covid-19-pandemic_3f44f5d6/df42be07-en.pdf

Used for the temporary-pandemic exception and the distinction between extraordinary telework and enduring remote-working arrangements.

https://www.incometaxindia.gov.in/documents/d/guest/income_tax_act_2025_as_amended_by_fa_act_2026-pdf

Used for section 9 business connection language, including contract-conclusion, principal-role and SEP concepts.

https://www.incometaxindia.gov.in/documents/d/guest/en-notified-it-rules-2026-20-03-2026-pdf

Used for the prescribed SEP thresholds of Rs 2 crore of payments and 300,000 users.

https://www.oecd.org/content/dam/oecd/en/topics/policy-sub-issues/beps-mli/multilateral-convention-to-implement-tax-treaty-related-measures-to-prevent-beps.pdf

Used for Article 12 on dependent-agent PE and the ‘principal role leading to the conclusion of contracts’ standard.

https://www.incometaxindia.gov.in/w/usa-comprehensive-agreements-1

Used for the service-PE clause and the more-than-90-days test.

https://www.incometaxindia.gov.in/w/uk-comprehensive-agreements-1

Used for the service-PE clause, including the 90-day rule and the 30-day associated-enterprise rule.

https://www.oecd.org/content/dam/oecd/en/topics/policy-issue-focus/map-statistics/map-statistics-india.pdf

Used for India’s 2024 MAP inventory and average closure time for attribution/allocation cases.

https://www.commerce.gov.in/wp-content/uploads/2026/03/PIB-Release.pdf

Used for India’s April-February 2025-26 services export estimate of USD 387.93 billion.

https://www.bls.gov/news.release/pdf/atus.pdf

Used for the 2024 statistic that 33% of employed people worked at home on days worked.

https://ec.europa.eu/eurostat/web/products-eurostat-news/w/ddn-20250514-2

Used for the 2024 statistic that 52.9% of EU enterprises with at least 10 employees conducted remote meetings.