Equalisation levy began as India’s answer to untaxed digital value, but its withdrawal shows how global tax negotiations, domestic friction, and legacy disputes finally boxed in unilateral design.

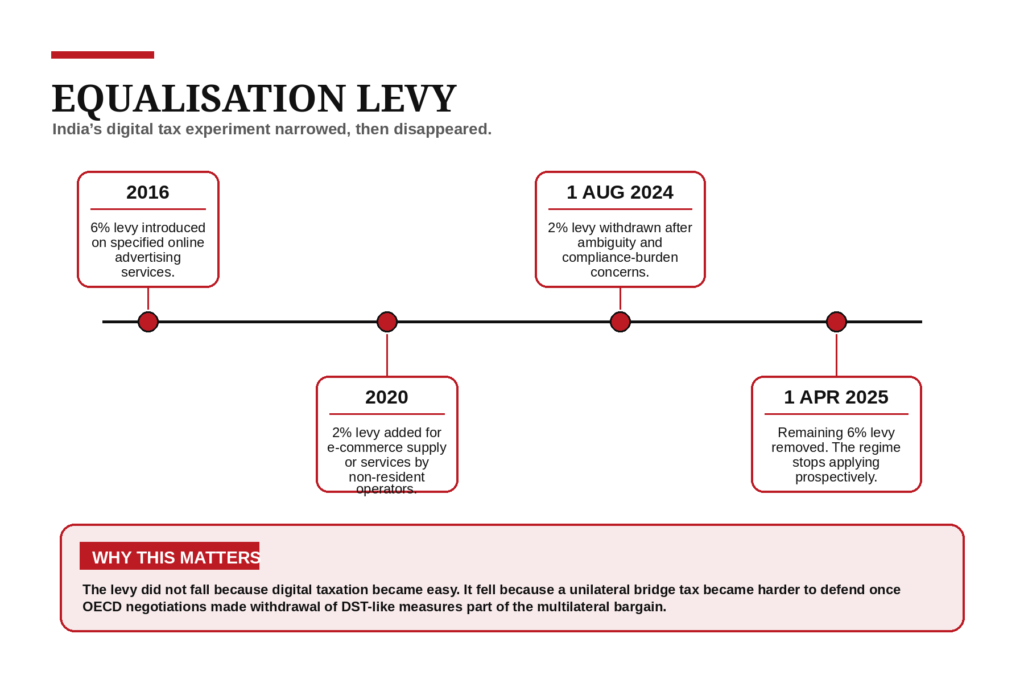

Equalisation levy is already a historical tax with a very current message. For nearly a decade, India used it as a workaround for a familiar problem: global digital businesses could earn heavily from Indian users and advertisers without easily fitting into the old permanent establishment grammar of international tax. That workaround looked bold in 2016, expansive in 2020, and awkward by 2024. By 1 August 2024 the 2 per cent levy on e-commerce supply or services had been withdrawn, and from 1 April 2025 the remaining 6 per cent levy on specified online advertising services was removed. That sequence says less about ideology than about the shrinking room for unilateral digital taxes in a world now organised around the OECD’s Two-Pillar project.

Equalisation levy was built as a bridge, not a final settlement

When India first imposed equalisation levy in 2016, the policy logic was straightforward. Digital commerce had widened faster than treaty law. The old tax base depended too heavily on physical presence, while digital groups could monetise customer access in India with limited onshore taxable presence. Equalisation levy was therefore not framed as a classic income-tax answer. It was a separate charge, imposed outside the Income-tax Act, aimed at specified digital payments. In 2020, India widened the experiment by adding the 2 per cent levy on e-commerce supply or services by non-resident operators. That was the real escalation. A narrow anti-base-erosion device became a broader market-jurisdiction claim.

That expansion changed the compliance equation. The 2 per cent version created harder questions: what counted as e-commerce supply, how far facilitation went, and when platform revenue overlapped with royalty or fees for technical services. Those are not drafting curiosities. They change contract pricing, withholding design, and dispute risk. For Indian businesses buying digital services, the levy became part of procurement friction. For multinational groups, it became another India-specific layer to model alongside treaty exposure, transfer pricing, and significant economic presence rules.

Why the levy began to lose policy oxygen

The official reason for rolling back the 2 per cent levy was telling: stakeholders had raised concerns about ambiguity and compliance burden. That is a concise way of saying the tax was collecting revenue while also producing classification fights and uncertainty in ordinary commercial flows. That uncertainty has a cost. It raises the marginal cost of cross-border digital advertising, marketplace operations, and platform-led intermediation. It also pushes the tax system into a high-volume, low-clarity enforcement cycle that looks assertive but does not necessarily improve tax certainty.

The remaining 6 per cent levy on online advertising survived the 2024 rollback, but only briefly. Its removal from 1 April 2025 shows that the state ultimately chose coherence over symbolism. Once the broader e-commerce limb had gone, retaining the advertising limb would have preserved a legacy carve-out without solving the larger architecture question. The system would still have been split between income-tax rules that increasingly speak the language of nexus, attribution, and treaties, and a parallel levy designed as an exceptional response to digitalisation.

Pillar One cornered unilateral levies even before it fully arrived

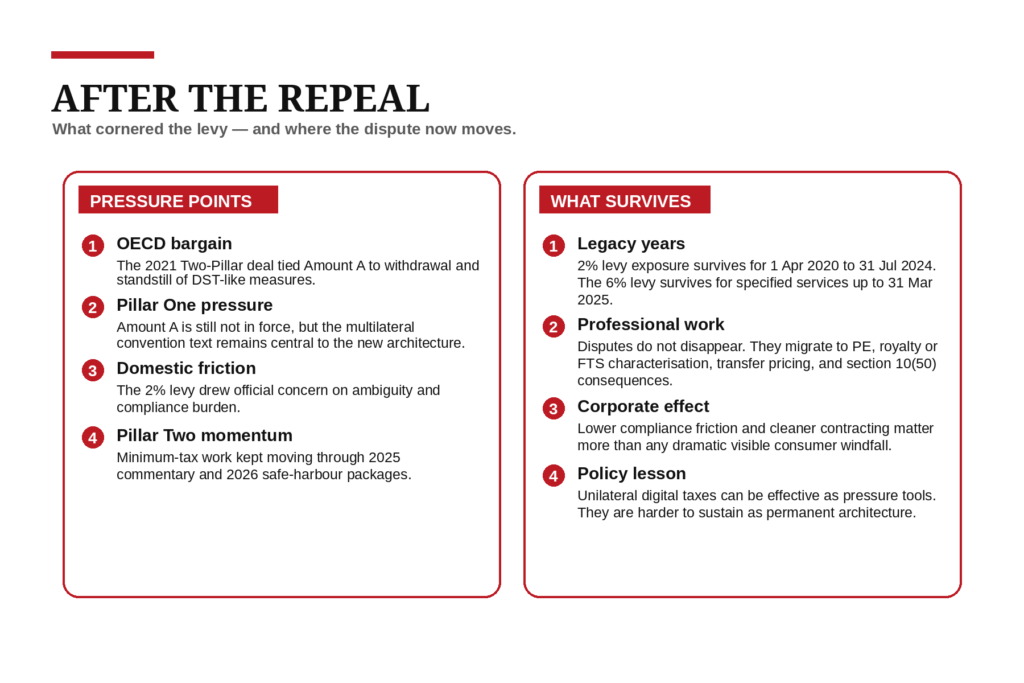

Equalisation levy did not need a fully operational Pillar One to lose strategic ground. The October 2021 OECD/G20 statement made the bargain explicit: a multilateral deal on reallocating taxing rights would travel with the withdrawal and standstill of digital services taxes and similar measures. The January 2025 update from the co-chairs showed how close and yet incomplete that process remained. The text of the Multilateral Convention for Amount A had been revised and stabilised, but consensus on the wider Pillar One package was still being held up by unresolved issues around Amount B. The OECD’s current Amount A page still says the convention text is not yet open to signature.

That gap matters, but not in the way critics often frame it. The repeal of India’s levy does not prove that Pillar One has succeeded. It proves that Pillar One changed the diplomatic price of staying unilateral. every domestic levy starts looking less like a permanent instrument and more like negotiating inventory. India appears to have judged that keeping equalisation levy alive would buy less fiscal leverage than it once did, while preserving bilateral friction and domestic complexity.

Pillar Two changed the politics faster than Pillar One changed the law

The other reason equalisation levy began to look dated is that Pillar Two moved from blueprint to administrative reality faster than Amount A did. By May 2025 the OECD had issued a consolidated commentary to the GloBE Rules incorporating agreed administrative guidance up to March 2025. By January 2026 the Inclusive Framework had added a side-by-side package with new safe harbours and simplification mechanisms. That does not substitute for a market-jurisdiction tax. Pillar Two is a minimum tax system, not a turnover levy and not a reallocation rule. Still, it changes the politics. Once the global conversation shifts toward effective tax rates, top-up taxes, and coordinated anti-base-erosion rules, a standalone levy on digital receipts starts to look dated.

Repeal does not mean the controversy has vanished

The levy may be gone prospectively, but it will stay alive in legacy assessments, appeals, refund positions, deduction disputes, and questions around section 10(50) for historical years. The 2 per cent levy still matters for transactions from 1 April 2020 to 31 July 2024, and the 6 per cent levy still matters for specified services up to 31 March 2025. For tax professionals, that means the work is not disappearing; it is mutating. Old levy disputes will continue, while new controversies migrate into permanent establishment, royalty versus business income, fees for technical services, transfer pricing, and the still unfinished law on significant economic presence.

Indian consumers should not expect a dramatic dividend from repeal. Much of the levy’s burden was usually embedded in ad budgets, platform commissions, merchant pricing, or wider procurement costs. The bigger gain is lower compliance friction and cleaner contracting for businesses that buy or sell through cross-border digital channels. For the corporate sector and tax advisory market, it is immediate.

Equalisation levy is gone in law, but not in policy memory

Equalisation levy now looks like what it probably was from the start: a bridge instrument for a phase when digital business outgrew treaty concepts faster than multilateral reform could catch up. India deserves credit for moving early when the global system was still arguing about whether market jurisdictions deserved a larger claim at all. It also deserves credit for stepping back once the cost of unilateralism began to exceed its utility.

So was equalisation levy living on borrowed time in a Pillar One–Pillar Two world? The legal answer is yes. The analytical answer is subtler. Multilateral reform has not cleanly solved digital taxation; Pillar One is still unfinished. But the future lies in fewer stand-alone levies and more contest over nexus, attribution, minimum tax design, and coordinated dispute resolution. India’s digital tax argument has not ended. It has moved to a more technical battlefield.

Sources & Data Points

- Memorandum to the Finance Bill, 2016 — introduction of the 6% equalisation levy

- Memorandum explaining the Finance (No. 2) Bill, 2024 — withdrawal of the 2% levy on e-commerce supply or services from 1 August 2024

- Statements of Fiscal Policy, Budget 2025-26 — records that the 6% equalisation levy on specified services was removed from 1 April 2025

- Income Tax Department: Equalisation Levy — current official overview and note that provisions are not applicable from 1 April 2025

- Income Tax Department: Non-resident – Benefits allowable [AY 2026-27] — note on section 10(50) not applying from AY 2026-27

- OECD/G20 Statement on a Two-Pillar Solution, 8 October 2021 — withdrawal and standstill commitment for DST-like measures

- OECD: Pillar One Update from the Co-Chairs, January 2025 — status of Amount A and unresolved issues around the wider Pillar One package

- OECD: Multilateral Convention to Implement Amount A of Pillar One — current official page stating the convention text is not yet open to signature

- OECD: Pillar One – Amount B — February 2025 consolidated report, February 2026 pricing tool revision, and implementation materials

- OECD: Global Anti-Base Erosion Model Rules (Pillar Two) — May 2025 consolidated commentary and January 2026 side-by-side package