Faceless penalty disputes are increasingly being won not by denying every addition, but by showing that digitised tax enforcement still failed the oldest procedural test: a fair hearing.

Faceless penalty disputes now turn less on whether an addition exists and more on whether the state heard the taxpayer properly before monetising that addition. That shift matters. In the old assessment culture, penalty litigation often rode on the facts of the underlying addition and the credibility of explanations offered across years of correspondence. In the faceless system, the record is thinner, tighter and almost entirely digital. A notice, a portal upload, a standardised show-cause draft, a compressed response window, then an order. For taxpayers and advisers, that has changed the battlefield. The strongest defence is often no longer “the department is wrong on tax”, but “the department didn’t lawfully arrive there”.

Faceless penalty was built for efficiency, not informality

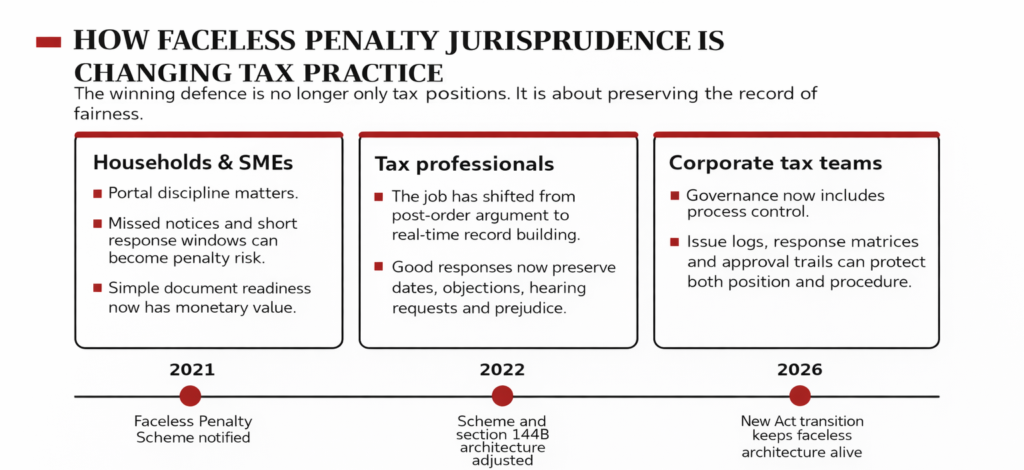

The legal architecture is not ambiguous. The Faceless Penalty Scheme, 2021 was notified under section 274, and the department’s own faceless guidance contemplates electronic proceedings, structured allocation and a personal hearing request that should generally be allowed after written submissions. Finance Act changes in 2022 then rewired section 144B because the government itself acknowledged operational difficulties in the first round of faceless assessment. Penalty administration did not sit outside that story; it absorbed the same design tension. The state wanted scale, consistency and less interface. Taxpayers wanted to know that reduced interface would not quietly become reduced hearing.

Why natural justice has moved to the centre

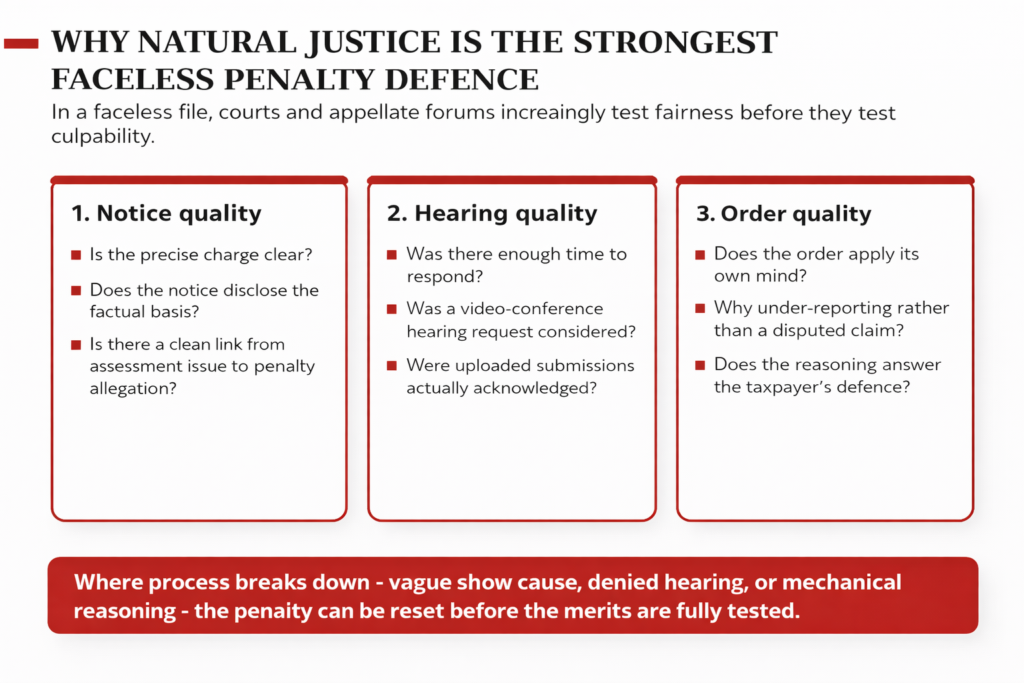

Penalty is not an ordinary arithmetic consequence of assessment. That has always been the theory, but faceless processing has made the distinction economically sharper. A section 270A exposure can still bite hard: 50 per cent of tax on under-reported income, and 200 per cent where the department characterises the case as misreporting. Once those percentages are attached to a digital workflow, every weakness in process becomes commercially material. Was the exact charge made clear? Was the taxpayer shown the factual basis on which the authority moved from a disputed claim to an allegation of under-reporting or misreporting? Was a hearing request meaningfully considered? Did the final order deal with the actual response, or only reproduce a template conclusion? In a faceless file, those questions are not technical irritants. They are the file.

The system made merits disputes more data-heavy – and process failures more visible

This is the irony of the current phase. Faceless assessment has given the department a stronger evidentiary environment through portal-based notices, AIS-linked trails and tighter digital capture of submissions. That can make pure denial a weak litigation strategy. But the same system also leaves a cleaner audit trail of procedural failure. A vague show-cause notice, a response uploaded but not addressed, a hearing sought but not granted, or an order that jumps from addition to penalty without separate reasoning – all of that is easier to demonstrate in a timestamped digital record than in the older paper-bound era. Faceless design reduced informal discretion, but it also reduced the department’s ability to hide behind informalism.

Why this defence is resonating now

The broader litigation environment shows that challenges to faceless proceedings are still very much alive. Supreme Court cause lists in February and April 2026 carried large batches of revenue appeals arising from high court rulings in faceless income-tax matters across multiple states. Not every one of those matters is a penalty case. That is not the point. The point is that process defects in the faceless regime have not remained isolated teething troubles; they are generating continuing appellate traffic at the highest level. Penalty jurisprudence sits downstream from that conflict. If courts insist that assessment machinery must respect notice, disclosure and hearing standards, it becomes harder for penalty authorities to argue that a separate quasi-civil consequence can survive a thinner standard of fairness.

The real fault-line is independent application of mind

This is where many penalty orders remain vulnerable. An addition may justify scrutiny, but it does not mechanically justify penal culpability. Faceless workflows tend to compress the sequence from proposed variation to final addition to penalty initiation. That administrative convenience can produce lazy reasoning. A claim may fail because evidence is inadequate, valuation is disputed, timing is contested or legal interpretation goes the wrong way. None of that automatically proves under-reporting, and still less misreporting. A defensible penalty order needs to show why the taxpayer’s conduct crossed the statutory threshold. If the order merely imports the language of the assessment or recites boilerplate, natural justice arguments become powerful because they expose not only procedural deficiency but also the absence of real adjudication.

What this means for taxpayers and tax practice

For salaried taxpayers and small businesses, the immediate cost is compliance friction. A faceless notice can be legally valid yet practically unforgiving. Missed email alerts, portal unfamiliarity, short response windows and difficulty in assembling documents quickly can turn a manageable explanation into a penalty problem. For tax professionals, the work is changing from after-the-fact advocacy to real-time record construction. The best advisers now draft penalty responses as if they are building a writ paper-book: specific objections, dated submission trails, hearing requests, prejudice arguments and clear distinctions between a failed claim and culpable conduct. For companies, especially those operating under tighter governance standards, the implication is broader. Internal tax controls now need to preserve process, not just position.

Natural justice is not a magic password

There is a temptation in the market to turn every faceless defect into a guaranteed escape route. That is wrong. Courts are unlikely to indulge performative objections where the taxpayer had full disclosure, adequate time and a fair chance to respond. Nor does every portal glitch become a jurisdictional defect. The doctrine is returning as a serious defence because the stakes are serious, not because judges want to reopen the age of endless oral hearings. The better reading is narrower and more durable: once the state chooses industrial-scale digital adjudication, it must obey its own procedure with unusual discipline. Efficiency cannot be purchased by thinning out fairness.

Why the 2026 transition keeps the issue alive

The arrival of the Income-tax Act, 2025 does not close this chapter. The CBDT’s 2026 transition FAQ says schemes designed to reduce direct contact – including faceless assessment and faceless appeals – continue under the corresponding provisions of the new law. That continuity matters. It means the jurisprudence being shaped now will not remain trapped in legacy disputes under the 1961 Act. The deeper lesson is not that faceless reform has failed. It is that the reform has matured enough for courts, advisers and taxpayers to ask a more demanding question. In a system built on self-assessment architecture and digital enforcement, can the revenue still impose a civil sanction without showing, clearly and demonstrably, that it listened before it punished? Increasingly, that is the question that decides the case.

Sources & Data Points

All links below are official government or court sources. Supreme Court cause lists are cited only to establish that faceless-procedure litigation remained live in early 2026, not to state merits outcomes.

- Faceless Penalty Scheme, 2021 – Notification No. 2/2021 (S.O. 117(E), 12 January 2021) – https://www.incometaxindia.gov.in/documents/d/guest/notification_no_2_2021

- Faceless Penalty (Amendment) Scheme, 2022 – Notification No. 54/2022 (27 May 2022) – https://www.incometaxindia.gov.in/documents/d/guest/notification_no_54_2022

- Directions under section 274(2B) after the 2022 faceless changes – Notification No. 55/2022 (27 May 2022) – https://www.incometaxindia.gov.in/documents/d/guest/notification_no_55_2022

- Faceless Scheme overview page, including guidance on personal hearing requests – https://www.incometaxindia.gov.in/faceless-scheme

- Circular No. 23/2022 – Explanatory Notes to the Finance Act, 2022, including section 144B streamlining – https://www.incometaxindia.gov.in/documents/20117/6507196/Circular-23-2022.pdf/9ca2d322-35aa-b850-e8f0-00b97fec4952?t=1762868705065&version=1.0

- Penalties under the Income-tax Law (Income Tax Department reference note, updated January 2026) – https://www.incometaxindia.gov.in/documents/20117/42998/Penalties-under-the-Income-tax-Law_2026-01-23_03-16-20_5114b6_en.pdf/0e5b2ee7-53b0-18ff-1877-36439177ea8d?t=1774013423941&version=1.0

- Form 35 User Manual – faceless first appeals on the e-filing portal – https://www.incometax.gov.in/iec/foportal/help/statutory-forms/popular-form/form35-um

- Income-tax Act, 2025 as amended by Finance Act, 2026 – https://www.incometaxindia.gov.in/documents/d/guest/income_tax_act_2025_as_amended_by_fa_act_2026-pdf

- FAQs on Interplay and Transition – Income-tax Act, 2025 (updated April 2026) – https://www.incometaxindia.gov.in/documents/81799/11848482/FAQs-on-Interplay-and-Transition.pdf/05f80c1a-073c-a5d7-fb6f-55509242be53?t=1774082865717

- Statements of Fiscal Policy as required under the FRBM Act – Budget 2025-26 – https://www.indiabudget.gov.in/budget2025-26/doc/frbm1.pdf

- Receipt Budget 2026-2027 – https://www.indiabudget.gov.in/doc/rec/allrec.pdf

- Economic Survey 2025-26, Chapter 2: Fiscal Developments – https://www.indiabudget.gov.in/economicsurvey/doc/eschapter/echap02.pdf

- Supreme Court of India cause list, 17 February 2026, showing connected faceless assessment appeals – https://api.sci.gov.in/jonew/cl/2026-02-17/M_J_1.pdf

- Supreme Court of India fresh civil cause list, 8 April 2026, showing connected faceless assessment appeals – https://api.sci.gov.in/jonew/cl/2026-04-08/M_J_1.pdf