A decade after GAAR entered the statute book, India’s anti-avoidance rule looks less like a daily weapon and more like a quiet constraint on how aggressive planning gets priced.

GAAR in India has reached the awkward age at which fear should have turned into evidence. When the rule first dominated tax debate, boardrooms treated it as a possible veto on cross-border planning and advisers warned of a long winter of subjectivity. The reality in 2026 is quieter. India’s revised tax revenue for 2025-26 stands at about Rs. 40.78 lakh crore in the Receipt Budget for 2026-27, with corporation tax at Rs. 11.09 lakh crore and taxes on income at Rs. 13.12 lakh crore. At that scale, an anti-avoidance rule is not judged by rhetoric. It is judged by whether it improves tax buoyancy without making investment feel legally provisional.

GAAR in India has aged into a system, not a scare story

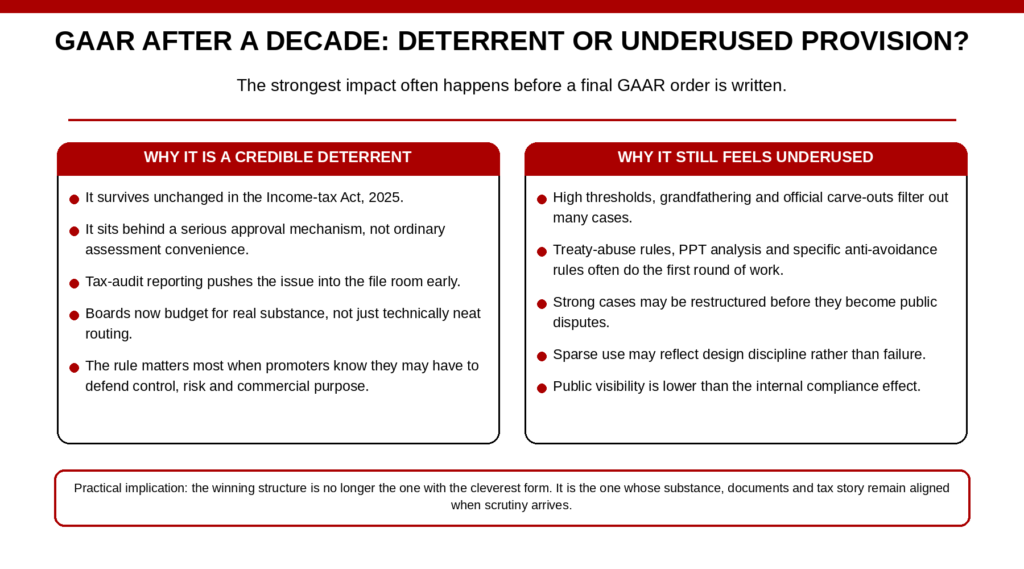

That is why GAAR now looks less like an emergency clause and more like permanent fiscal plumbing. The official transition FAQs issued after the Income-tax Act, 2025 came into force say GAAR has been retained as it is, with thresholds, approval mechanisms and safeguards continuing. That continuity matters. A rule that survives a wholesale rewriting of the statute is no longer a headline. It is policy intent carried forward.

The regime also entered adulthood with unusual caution. The Finance Act, 2015 deferred implementation by two years and protected investments made up to 31 March 2017 through the rules. Even in March 2026, CBDT amended Rule 10U on grandfathering language. A provision launched with this much transitional protection was never designed as a mass-use weapon. It was designed as a deterrent that had to remain credible without unsettling old capital or inviting a repeat of India’s retrospective-tax reputation shock.

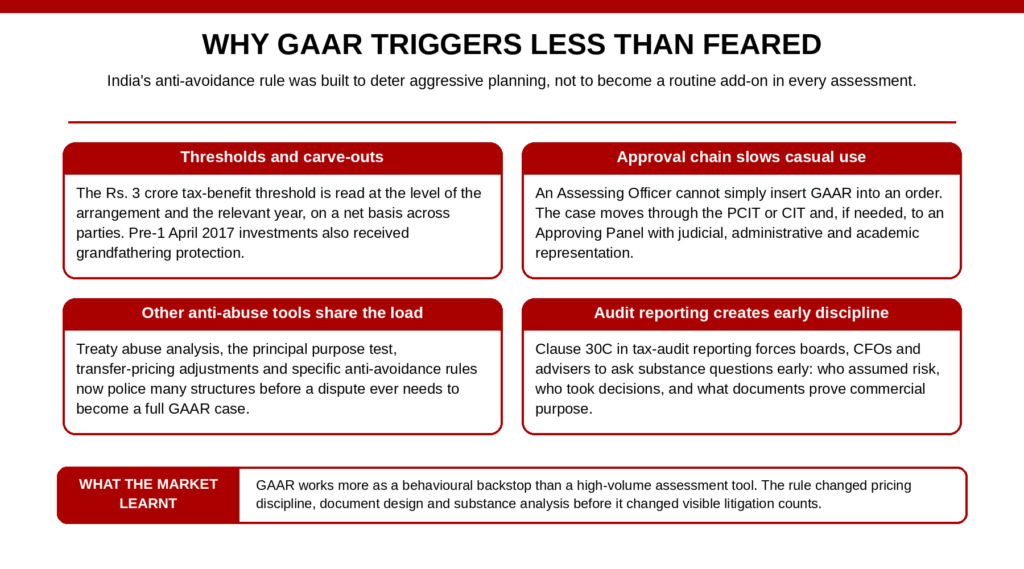

Why GAAR in India triggers less than feared

CBDT’s 2017 clarifications narrowed the mythology further. GAAR, the Board said, should not be invoked merely because an entity sits in a tax-efficient jurisdiction. It should not override a taxpayer’s basic choice of how to structure a transaction. If an FPI’s jurisdiction is driven by non-tax commercial considerations and the main purpose is not to obtain a tax benefit, GAAR should not apply. The same circular also underlined that the Rs. 3 crore tax-benefit threshold is read at the level of the arrangement and the relevant assessment year, taking into account the impact on all parties on a net basis. Add the consistency principle — if an arrangement is held permissible in one year on unchanged facts, GAAR should not suddenly appear in the next — and the supposedly boundless rule starts to look carefully engineered.

The procedure adds another brake. The department’s own assessment guidance shows that GAAR is not something an Assessing Officer casually drops into an order. The AO first refers the matter to the PCIT or CIT. The commissioner must issue reasons and hear objections. Only then can the case go to an Approving Panel comprising a High Court judge, a senior IRS officer and a specialist academic or scholar. This is a deliberately heavy approval chain. It lowers trigger frequency, but that is the point. The state wanted seriousness, not a shortcut.

The anti-abuse landscape around GAAR has changed

There is a second reason GAAR looks quieter now: it is no longer the only anti-abuse language in the room. OECD materials record that India deposited its instrument of ratification for the Multilateral Instrument on 25 June 2019 and that it entered into force for India on 1 October 2019. OECD guidance on treaty abuse says tax administrations can now use effective treaty provisions, including the principal purpose test, to stop treaty shopping. That changes the practical ecology of disputes. Some arrangements that might once have been framed as domestic GAAR cases can now be challenged through treaty-abuse provisions, beneficial ownership analysis, transfer-pricing adjustments or other specific anti-avoidance rules. GAAR has not vanished; it has become the backstop behind a more crowded front line.

That helps explain why public GAAR theatre has been thinner than the early panic suggested. The scarcity of visible, repeated GAAR fights does not prove inactivity. It may reflect triage. Sophisticated groups often restructure before the issue reaches a final order. Advisers screen transactions against substance, control, commercial purpose, risk allocation and exit logic long before a file reaches assessment. The shadow of GAAR changes behaviour even when the rule itself stays in the drawer.

Why the provision still matters

The best evidence of that behavioural effect sits in compliance, not in headlines. Clause 30C in the department’s 2026 guidance on items reportable in the tax audit report requires the tax auditor to state whether the assessee has entered into an impermissible avoidance arrangement. That is a powerful design choice. It means GAAR operates not only at the end of an assessment but inside the self-assessment architecture itself. Once a provision enters the audit checklist, boards and advisers start asking different questions at the structuring stage: why this jurisdiction, why this intermediary, who truly assumes risk, and what papers prove a commercial rationale if the tax benefit is stripped away.

For the corporate sector, that shifts cost from litigation to preparation. The burden is not merely legal. It is operational. Groups must budget for substance: people with real authority, records tying financing and decision-making to actual functions, and transaction papers that do not collapse when someone asks who controlled the cash, the exit or the downside. For tax professionals, the work has moved away from elegant form engineering and toward fact architecture. That raises compliance friction, but it also creates a clearer market for higher-value advisory work.

The middle class meets GAAR indirectly. Salaried taxpayers will rarely see Chapter X-A in their own files, but they bear the political consequences of whether the state can credibly tax high-end avoidance without constantly widening routine compliance burdens elsewhere. If anti-avoidance at the top works, even imperfectly, the system relies less on squeezing marginal revenue from already visible taxpayers. But the opposite risk also matters. If GAAR becomes too subjective, capital costs rise and business uncertainty feeds into jobs, wages and prices. The right test is balance, not bravado.

Credible deterrent, not dead letter

On that test, GAAR in India today looks credible but intentionally sparse. It is not a dead letter, because the law continues unchanged, the approval machinery remains intact, tax audit reporting forces early visibility, and the surrounding treaty-abuse framework has become sharper. It is also not the sweeping headline provision that its critics and defenders once imagined. Underuse, in this context, may actually be a sign of design discipline. A general anti-avoidance rule should not be an everyday clause. It should be the state’s reserve capacity against arrangements whose legal form still outruns their economic substance. After a decade, that is where India seems to have landed.

SOURCES & DATA POINTS

- Receipt Budget 2026–2027, Ministry of Finance — Used for 2025-26 revised tax revenue, corporation tax and taxes on income figures. [Open source]

- Income-tax Act, 2025 (as amended by Finance Act, 2026) — Used for current statutory continuity and GAAR’s continued place in the post-2026 code. [Open source]

- FAQs on Interplay and Transition from the Income-tax Act, 1961 to the Income-tax Act, 2025 — Used for the official statement that GAAR continues unchanged under the 2025 Act. [Open source]

- CBDT Circular No. 19/2015 — Used for deferment of GAAR implementation and protection for investments made up to 31 March 2017. [Open source]

- CBDT Circular No. 07/2017 (in Tax Bulletin Jan–Mar 2017) — Used for official clarifications on tax-efficient jurisdictions, FPI treatment, the Rs. 3 crore threshold and the consistency principle. [Open source]

- Income Tax Department assessment guidance page — Used for the current procedural description of how GAAR references move from the AO to the commissioner and then to the Approving Panel. [Open source]

- Items reportable in the Tax Audit Report (2026 guidance) — Used for Clause 30C reporting on impermissible avoidance arrangements. [Open source]

- Notification No. 54/2026, Income-tax (Tenth Amendment) Rules, 2026 — Used for the March 2026 amendment to Rule 10U grandfathering language. [Open source]

- OECD: Preventing tax treaty abuse — Used for the current description of how the principal purpose test and related treaty-abuse tools operate in the post-BEPS environment. [Open source]

- OECD MAP Peer Review Report, India (Stage 2) — Used for the official OECD record that India deposited its MLI instrument on 25 June 2019 and that it entered into force for India on 1 October 2019. [Open source]