Treaty shopping disputes in India now turn less on residency paperwork and more on who truly controls income, risk, and exit—raising a sharper question about how subjective tax planning has become.

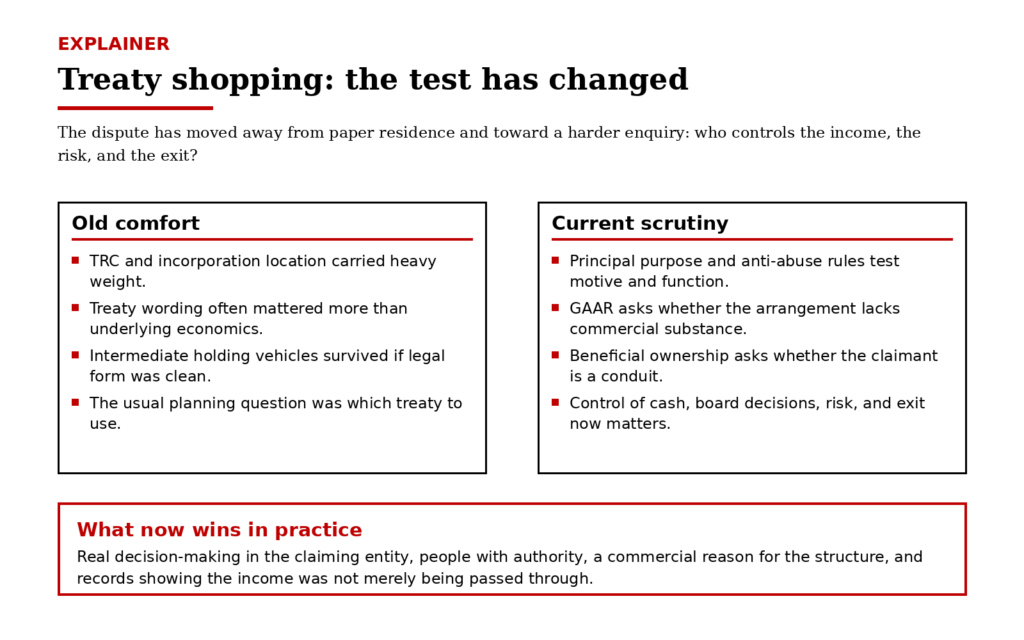

The old bargain was certainty

Treaty shopping used to be judged through a relatively stable grammar. If the claimant entity was tax resident where the treaty required, and if the legal ownership chain aligned with the document trail, the analysis often stopped there. That older approach was not accidental. It reflected a policy bargain India once made to attract capital with lower compliance friction, especially through widely used holding jurisdictions. The comfort was never absolute, but it was real. A tax residency certificate, a board file, and a legally coherent chain could carry enormous weight.

That history still matters because the structures did not disappear when the debate changed. India recorded USD 81.04 billion of FDI inflow in FY 2024–25, with Singapore contributing 30% and Mauritius 17%, according to the Ministry of Commerce and Industry. Those numbers are not proof of abuse. They are proof that treaty-linked investment routes remain economically significant. That is why the legal shift matters so much. When the line moves from formal entitlement to substantive justification, the cost is not confined to a handful of aggressive structures. It reaches mainstream cross-border planning, fund exits, treasury design, and M&A pricing.

Tiger Global changed the tone of the dispute

The timeliness trigger is the Supreme Court’s January 2026 ruling in Tiger Global. The Court did not say every intermediary vehicle is suspect. It said something more consequential. Mere holding of a tax residency certificate cannot, by itself, shut down enquiry once the statutory anti-abuse framework is in place. That is a major tonal shift from the older certainty associated with the government’s 2013 clarification that Indian authorities would accept the TRC as evidence of residence and would not go behind it on resident status. Residence still matters. It just no longer settles everything that follows.

What the Court effectively did was pull treaty planning out of a paperwork era and place it inside a mixed enquiry: treaty text, domestic anti-avoidance rules, facts, commercial purpose, and actual control. That is a harder arena for taxpayers and advisers because the dispute is no longer only about whether a treaty technically applies. It is about whether the claimant can credibly say the arrangement had economic coherence. In practice, the court file now asks: who could decide on the money, who bore the downside, who negotiated the exit, and who had the power to do something other than pass the gain or income onward.

Why the line moved from form to substance

This shift did not arise from one judgment alone. It reflects the larger anti-abuse turn in international tax. India signed the Multilateral Instrument in 2017 and the OECD records its entry into force for India from 1 October 2019. In the Income Tax Department’s synthesised treaty texts, the new preambular language now states that tax treaties are meant to eliminate double taxation without creating opportunities for non-taxation or reduced taxation through treaty-shopping arrangements. The same documents show the Principal Purposes Test in operation: a treaty benefit may be denied where it is reasonable to conclude that obtaining that benefit was one of the principal purposes of the arrangement, unless the outcome still accords with the object and purpose of the relevant treaty provision.

Domestic law has moved in the same direction. The Income-tax Act, 2025, which comes into force on 1 April 2026, preserves the GAAR architecture. Section 179 defines an impermissible avoidance arrangement as one whose main purpose is a tax benefit and which, among other things, lacks commercial substance or misuses the Act. Section 180 says an arrangement may be deemed to lack commercial substance where its substance differs materially from its form, where it uses accommodating parties, or where it has no significant effect on business risks or net cash flows apart from tax results. Section 181 explicitly allows denial not just of a tax benefit under the Act, but of a benefit under a tax treaty. In other words, treaty shopping is no longer analysed in a treaty-only silo.

Beneficial ownership still matters, but it is no longer the whole story

The beneficial ownership debate, or BO in practitioner shorthand, has also become more exacting. The Delhi High Court’s 2024 Tiger Global judgment discussed the classic OECD idea that BO is meant to exclude agents, nominees, and conduits with very narrow powers over income. That remains useful, but it is only one gate in a wider system. A vehicle may fail because it is a conduit. It may also fail because principal purpose, commercial substance, or GAAR-based misuse arguments do the work even where the BO analysis is inconclusive. That layered scrutiny is why taxpayers increasingly feel that planning is turning subjective: several overlapping tests can now be invoked against the same structure.

The real problem is not scrutiny. It is elasticity.

There is nothing inherently objectionable about courts looking beyond labels. Tax law has always struggled with arrangements that are immaculate in form and thin in economics. The real concern is elasticity. Phrases such as “one of the principal purposes”, “commercial substance”, and “misuse or abuse” are powerful because they catch sophisticated avoidance. They are also dangerous because they can slide into hindsight. A structure that looked commercially rational when capital was deployed can later be recast as tax-motivated after the exit succeeds. That turns ex ante planning into ex post moral judgment. For corporate India, that widens execution risk. For tax professionals, it shifts advisory work from legal opinion to evidence architecture. For the self-assessment architecture of the system, it increases uncertainty even when no fraud is alleged.

The second-order effects are easy to miss. The middle class does not litigate treaty shopping, but it still bears the tax incidence of bad design. If subjectivity becomes excessive, clean inbound capital demands a risk premium, valuations adjust, and the cost of funding rises across the system. If scrutiny is too weak, confidence in fairness and tax buoyancy erodes. Either way, someone pays. Professionals feel it through higher documentation burdens and defensive opinions. Corporates feel it through longer deal timetables, heavier diligence on board authority and treasury functions, and lower marginal utility from thin holding structures that once looked efficient on paper.

A workable line is still possible

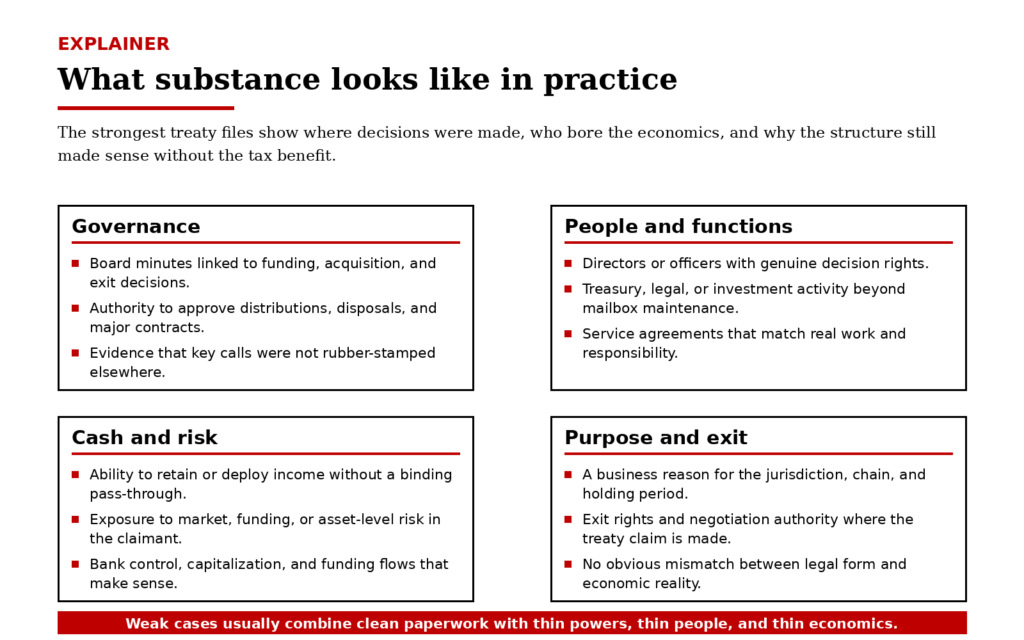

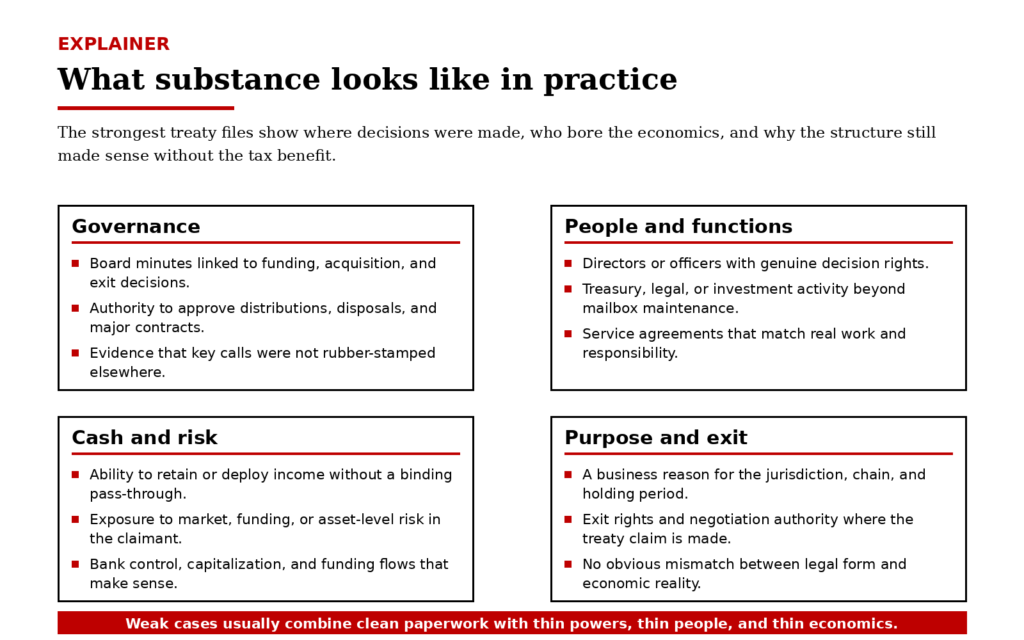

Planning is not becoming illegitimate. It is becoming evidentiary. That is the crucial distinction. Courts do not need a vague anti-avoidance mood to police treaty abuse. They need a disciplined way to test whether the treaty claimant had real powers over the income or gains, real exposure to the economics, and a business rationale that survives even after tax is stripped out of the story. That standard is demanding, but it is not arbitrary. It asks for commercial coherence, not moral purity.

That is where the next round of litigation will be decided. Not on whether a jurisdiction has a low rate. Not on whether a structure looks elegant on a chart. It will turn on whether the taxpayer can show substance with records that stand up under pressure: decision rights, funding logic, risk assumption, negotiation authority, and freedom to enjoy the income for its own account. Treaty shopping disputes are shifting from form to substance. The challenge for Indian tax jurisprudence now is to keep that shift rigorous without letting it become impressionistic.

Beneficial ownership still matters, but it is no longer the whole story

The beneficial ownership debate, or BO in practitioner shorthand, has also become more exacting. The Delhi High Court’s 2024 Tiger Global judgment discussed the classic OECD idea that BO is meant to exclude agents, nominees, and conduits with very narrow powers over income. That remains useful, but it is only one gate in a wider system. A vehicle may fail because it is a conduit. It may also fail because principal purpose, commercial substance, or GAAR-based misuse arguments do the work even where the BO analysis is inconclusive. That layered scrutiny is why taxpayers increasingly feel that planning is turning subjective: several overlapping tests can now be invoked against the same structure.

The real problem is not scrutiny. It is elasticity.

There is nothing inherently objectionable about courts looking beyond labels. Tax law has always struggled with arrangements that are immaculate in form and thin in economics. The real concern is elasticity. Phrases such as “one of the principal purposes”, “commercial substance”, and “misuse or abuse” are powerful because they catch sophisticated avoidance. They are also dangerous because they can slide into hindsight. A structure that looked commercially rational when capital was deployed can later be recast as tax-motivated after the exit succeeds. That turns ex ante planning into ex post moral judgment. For corporate India, that widens execution risk. For tax professionals, it shifts advisory work from legal opinion to evidence architecture. For the self-assessment architecture of the system, it increases uncertainty even when no fraud is alleged.

The second-order effects are easy to miss. The middle class does not litigate treaty shopping, but it still bears the tax incidence of bad design. If subjectivity becomes excessive, clean inbound capital demands a risk premium, valuations adjust, and the cost of funding rises across the system. If scrutiny is too weak, confidence in fairness and tax buoyancy erodes. Either way, someone pays. Professionals feel it through higher documentation burdens and defensive opinions. Corporates feel it through longer deal timetables, heavier diligence on board authority and treasury functions, and lower marginal utility from thin holding structures that once looked efficient on paper.

A workable line is still possible

Planning is not becoming illegitimate. It is becoming evidentiary. That is the crucial distinction. Courts do not need a vague anti-avoidance mood to police treaty abuse. They need a disciplined way to test whether the treaty claimant had real powers over the income or gains, real exposure to the economics, and a business rationale that survives even after tax is stripped out of the story. That standard is demanding, but it is not arbitrary. It asks for commercial coherence, not moral purity.

That is where the next round of litigation will be decided. Not on whether a jurisdiction has a low rate. Not on whether a structure looks elegant on a chart. It will turn on whether the taxpayer can show substance with records that stand up under pressure: decision rights, funding logic, risk assumption, negotiation authority, and freedom to enjoy the income for its own account. Treaty shopping disputes are shifting from form to substance. The challenge for Indian tax jurisprudence now is to keep that shift rigorous without letting it become impressionistic.

Sources & Data Points

- Supreme Court of India, The Authority for Advance Rulings (Income Tax) & Ors. v. Tiger Global International II/III/IV Holdings, 2026 INSC 60, judgment dated 15 January 2026.

- Delhi High Court, Tiger Global International II Holdings & Ors. v. Authority for Advance Rulings & Ors., judgment dated 28 August 2024.

- Income-tax Act, 2025 [30 of 2025], as amended by the Finance Act, 2026, official text published by the Income Tax Department.

- Department of Economic Affairs, Ministry of Finance, clarification on Tax Residency Certificate and section 90.

- OECD, Signatories and Parties (BEPS MLI Positions), official status document.

- Income Tax Department, Ministry of Finance, Malta Synthesised Text of the MLI and India–Malta tax treaty.

- Press Information Bureau, Ministry of Commerce & Industry, ‘India Records USD 81.04 Billion FDI Inflow in FY 2024–25’, 27 May 2025.

- Press Information Bureau factsheet, official macroeconomic update including April–July 2025 gross and net FDI data.

9. DPIIT FDI Factsheet, June 2025, official country-wise and cumulative FDI tables.