Capital vs revenue lines are fraying in India’s digital economy. SaaS subscriptions, cloud infrastructure, and data-driven intangibles create ‘enduring’ benefits without durable assets—forcing tax doctrine to chase new facts.

Capital vs revenue is no longer an accounting footnote for Indian digital businesses; it is a strategic risk that shows up in cash, valuation, and boardrooms. Walk into a mid-size SaaS firm at quarter-end and you’ll see finance teams triage cloud bills, platform fees, implementation invoices, and cross-border licences, then ask an old question with a new sting: did we just buy a service, or did we build an asset? The answer moves taxable profit, affects reported margins, and shapes the self-assessment architecture that India’s income-tax system leans on. In a digital business, the same invoice can be argued three ways — as a recurring operating cost, as a capital outlay, or as a payment whose character turns on treaty language. That’s why disputes have spread from edge cases to the centre of financial planning.

Capital vs revenue in the SaaS era: why ‘rent’ behaves like infrastructure

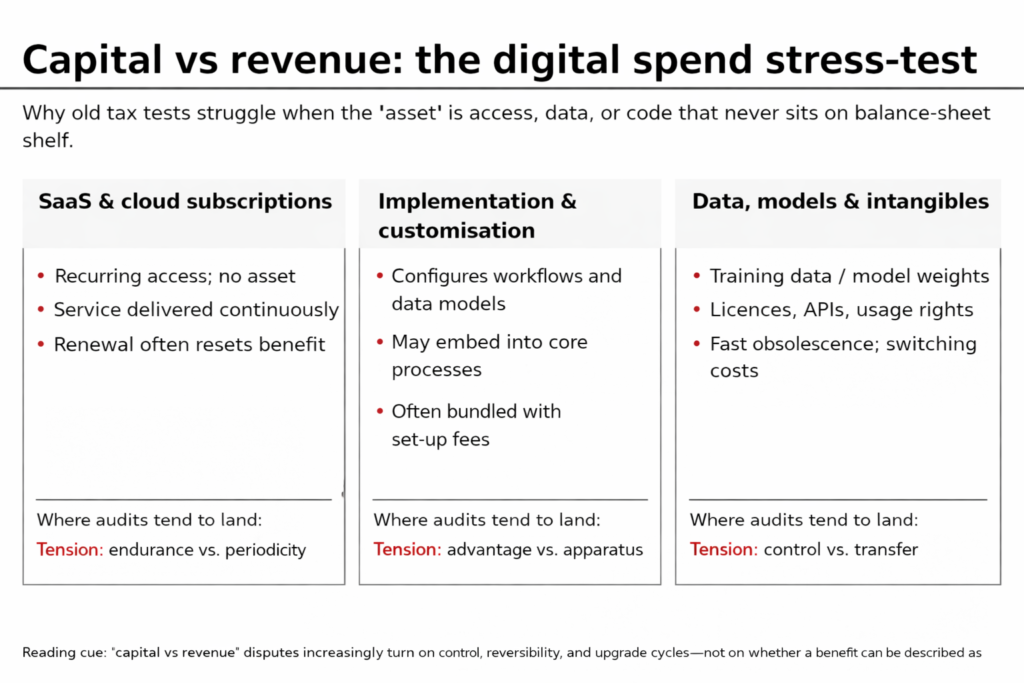

A subscription can run a company’s core operations without transferring a line of code. That simple fact destabilises the capital vs revenue boundary. The classic intuition says capital expenditure upgrades the profit-making apparatus, while revenue expenditure keeps it running. SaaS flips that: control sits with the vendor; dependence sits with the customer. A year of CRM access is rent in form, but switching costs can feel like ownership in substance once workflows, permissions, and data pipelines harden around a vendor’s architecture. Add rapid release cycles and bundled support, and the familiar ‘enduring benefit’ test starts to describe everything — and therefore explains very little. Businesses chase speed and reliability, not asset formation, but doctrine still asks them to prove what they never intended to create.

Income-tax Act, 2025: new numbering, same judgement calls

India’s direct tax statute has been rewritten, but the capital vs revenue dilemma hasn’t been legislated away. The Union Budget 2026-27 states that the Income-tax Act, 2025 comes into force from 1 April 2026, replacing the Income-tax Act, 1961. The Income Tax Department’s press release and transition FAQs stress continuity, with transitional provisions to keep pending proceedings intact. For digital firms, that is a warning as much as reassurance: simplification of sections doesn’t simplify judgement calls. The new Act reorganises the rulebook, but it doesn’t abolish the need to decide whether a payment creates a capital asset, adds to a block of intangibles, or is simply laid out wholly and exclusively for business. Old disputes will keep running under transition rules, and new ones will be argued in fresh numbering.

Digital economy disputes: cloud characterisation leaks into doctrine

Digital economy disputes are also dragging capital vs revenue into cross-border characterisation fights. Once payments travel abroad, the labels multiply: royalty, fees for technical services, business income, permanent establishment. Yet the anxiety is familiar: does the payer “use” equipment or intellectual property, or merely consume a service? A 2025 Delhi High Court matter involving cloud computing receipts (in appeals concerning Amazon Web Services) captures the fault line, with the revenue testing whether cloud computing payments are ‘royalty’ under domestic law and the India–US tax treaty. That debate is formally about income character, not deductions, but it reveals the same doctrinal strain. Cloud blurs the difference between renting computing capacity and exploiting embedded software, and the tax system is forced to pick a label even when business reality refuses one.

Implementation and customisation: the disguised asset inside the contract

The most combustible fact pattern sits inside bundled contracts. Implementation and customisation invoices can look like consultancy, but their economic effect can resemble capex: they rewire internal controls, embed data schemas, and hard-code workflow logic. The more irreversible the change, the easier it is for an assessing officer to argue that the profit-making apparatus has been upgraded. Digital firms respond by slicing contracts into “set-up”, “migration”, “integration”, and “support”, hoping to defend recurring deductions while capitalising only what truly creates an enduring system. But contract design has its own compliance friction. If the split looks artificial, it invites disputes; if it is too blunt, it may trigger downstream questions on withholding, GST input tax credits, and transfer-pricing alignment for intra-group services.

Intangibles and the ‘enduring benefit’ rethink

Indian tax law recognises intangible assets for depreciation — know-how, patents, copyrights, trademarks, licences, franchises, and similar business or commercial rights — but digital businesses keep expanding the perimeter. Is a perpetual software licence an intangible asset? Often. Is a one-year SaaS term? Usually not. Is an exclusive data licence an asset, or a consumable input to a model that will be retrained next quarter? The elasticity invites argument. A Supreme Court decision dated 19 December 2025 on non-compete fees is a useful signal of how courts are re-reading “enduring benefit” in modern markets. The Court held that a payment to keep a competitor out did not create a new profit-earning apparatus or a monopoly, and allowed it as revenue expenditure. That reasoning matters for digital spend: a benefit can last and still be operational, especially when its value depends on continuous execution rather than ownership.

Litigation lock-up and fiscal stakes for tax buoyancy

Ambiguity carries a measurable fiscal cost, and the latest public audit trail shows how large the litigation machine has become. The CAG’s Report No. 14 of 2025 (Direct Taxes, for the period ended March 2023) records that appeals pending with Commissioner (Appeals) rose to 5.30 lakh in FY 2022-23, with the amount locked in those cases increasing to ₹16.53 lakh crore; it also reports ₹7.18 lakh crore locked across pending appeals at the ITAT, High Courts, and the Supreme Court. The Receipt Budget 2026-27 puts the revised estimate of corporation tax for 2025-26 at ₹11.09 lakh crore, and ‘taxes on income’ (non-corporate) at ₹13.12 lakh crore. When so much money is collected or contested at scale, the capital vs revenue line becomes a macro variable. Tax buoyancy benefits from clarity; ambiguity converts revenue into arrears and investment into legal reserves.

Second-order effects for households, tax professionals, and corporates

The second-order effects spill beyond large corporates. In a subscription-heavy economy, tax incidence travels. A company facing uncertain deductibility may build a risk buffer into pricing, which lands on client budgets and ultimately on households through higher costs of services that now sit in the input stack of almost everything: education platforms, health-tech, logistics, and small retailers using software for billing. For tax professionals, the churn shows up as case-load inflation and a documentation arms race — more time on contract annotations, allocation keys, and evidentiary trails, less time on productive planning. For the corporate sector, the cost is not only cash; it is optionality. Firms become conservative about upgrades and experimentation when the tax outcome of the next toolchain change feels unknowable.

A modern capital vs revenue test for digital spend

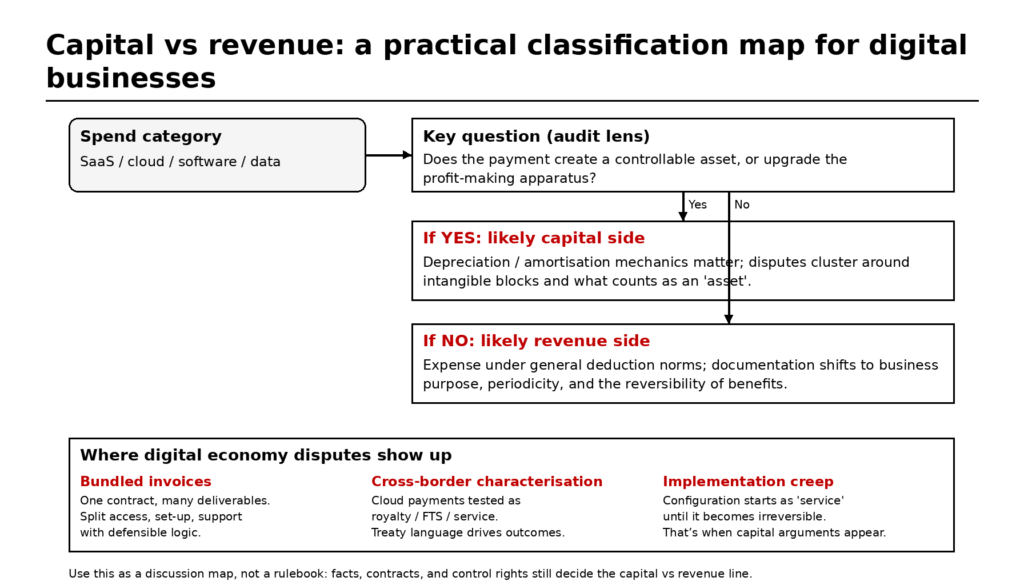

A modern capital vs revenue test for digital businesses shouldn’t try to write a universal rule for SaaS, data, and cloud. It should narrow the factual questions that drive disputes and align them with how digital value is produced. Start with control rights: can the taxpayer exclude others, transfer the right, or keep using it without the vendor? Then test reversibility: can the business unwind the benefit at low cost, or is it embedded in processes and data? Add the upgrade cycle: does value depend on continual vendor updates, or does it persist independently? These questions map to cloud realities better than duration. If the administration wants fewer disputes, it can publish narrower guidance on typical SaaS, implementation, and data-licence patterns, and force the debate onto contracts and facts rather than slogans. Until then, digital businesses will keep fighting old doctrines with new invoices, and everyone will pay the compliance bill.

Sources & Data Points

- Receipt Budget 2026-27 (RE 2025-26 direct tax heads) — https://www.indiabudget.gov.in/doc/rec/allrec.pdf

- CAG Report No. 14 of 2025 (Direct Taxes, period ended March 2023) — appellate pendency and amounts locked — https://cag.gov.in/uploads/download_audit_report/2025/Report-No.-14-of-2025_CA-2022-23_English-PDF-A-068a46a0b283d09.44138066.pdf

- Union Budget 2026-27 Speech — commencement of Income-tax Act, 2025 from 1 April 2026 — https://www.indiabudget.gov.in/doc/budget_speech.pdf

- Income-tax Act, 2025 [30 of 2025] (as amended by Finance Act, 2026) — https://www.incometaxindia.gov.in/documents/d/guest/income_tax_act_2025_as_amended_by_fa_act_2026-pdf

- Income-tax Act, 1961 [43 of 1961] (as amended by Finance Act, 2026) — https://www.incometaxindia.gov.in/documents/d/guest/income_tax_act_1961_as_amended_by_fa_act_2026-1-pdf

- CBDT Press Release (1 Apr 2026): Income-tax Act, 2025 comes into force — https://www.incometaxindia.gov.in/documents/d/guest/press-release-income-tax-act-2025-comes-into-force-from-01-april-2026-pdf

- CBDT FAQs on Interplay and Transition — Income-tax Act, 2025 — https://www.incometaxindia.gov.in/documents/81799/11848482/FAQs-on-Interplay-and-Transition.pdf/05f80c1a-073c-a5d7-fb6f-55509242be53?t=1774082865717

- Delhi High Court (29 May 2025): cloud computing receipts and ‘royalty’ questions (ITA 150/2025 & 154/2025) — https://delhihighcourt.nic.in/app/showFileJudgment/VIB29052025ITA1502025_153957.pdf

- Supreme Court (19 Dec 2025): non-compete fee allowed as revenue expenditure (2025 INSC 1481) — https://api.sci.gov.in/supremecourt/2013/5229/5229_2013_14_1504_67116_Judgement_19-Dec-2025.pdf

- Explanatory Memorandum to Finance Bill, 2026 (direct tax amendments, incl. Income-tax Act, 2025 transition issues) — https://www.indiabudget.gov.in/doc/memo.pdf

- Income-tax Rules, 2026 (notified, reference to Income-tax Act, 2025) — https://www.incometaxindia.gov.in/documents/d/guest/en-notified-it-rules-2026-20-03-2026-pdf