Digital evidence in search cases is reshaping tax litigation: not because every file proves concealment, but because metadata, device history and chain-of-custody now influence who must explain what.

The legal architecture has changed before the evidentiary culture has

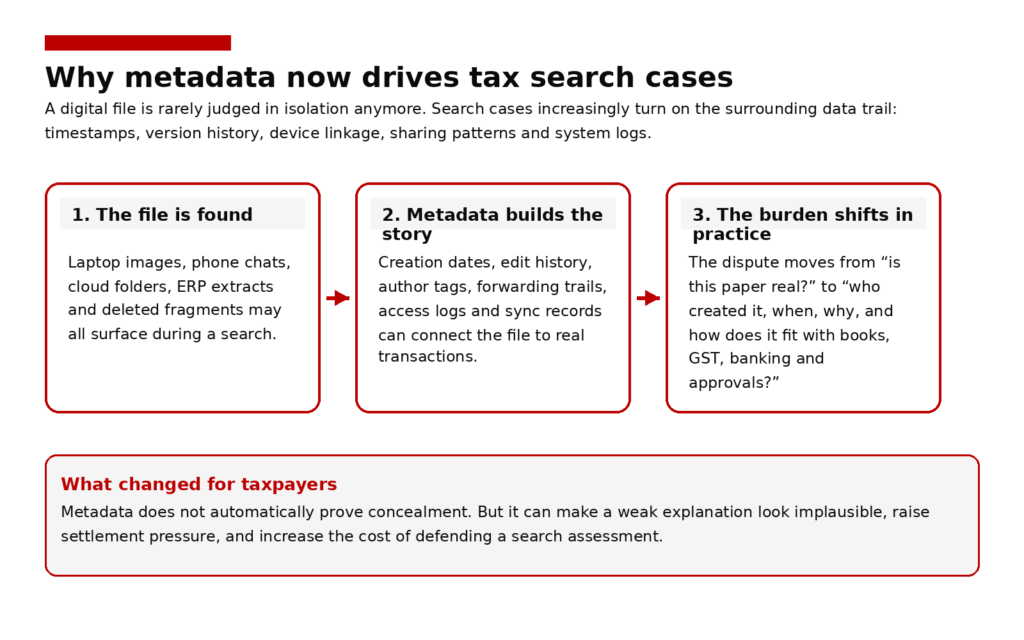

Digital evidence in search cases now sits at the start of the dispute, not the end. In an earlier era, a raid turned on paper diaries, cash trails and oral statements that could later be diluted in cross-examination. That world hasn’t vanished, but it no longer dominates. Phones mirror business life. Cloud folders preserve drafts. Email headers, login history, spreadsheet versions, ERP audit logs and even deletion patterns create a parallel record of conduct. For taxpayers, the real danger is not only what a document says. It is what the metadata around that document lets the department argue about timing, ownership, control and intent.

That shift matters more after the search-assessment architecture changed. The Union Budget 2024 memorandum said the recast of Chapter XIV-B was meant to deliver early finalisation of search assessments, coordinated investigation and lower multiplicity of proceedings. The Income-tax Department’s assessment guidance now states that, with effect from 1 September 2024, search and requisition cases stand outside the reassessment route and are governed by block assessment. The new Income-tax Act, 2025, which came into force on 1 April 2026, preserves that transition logic through saving provisions and FAQs that make clear pre-commencement searches continue under the old law. Put plainly, the forum has become more consolidated just as the evidentiary record has become more digital.

Why digital evidence in search cases shifts the pressure point

That combination changes the burden of explanation in practice. Search law still does not relieve the department of proving undisclosed income. But electronic trails make it easier for the department to build an inferential case before it ever reaches a statement under oath. A worksheet recovered from a laptop may be tentative. Add file creation dates, author tags, linked mail traffic, WhatsApp forwarding history, payment timestamps and backup copies from another device, and the same worksheet starts to look less like a rough projection and more like an operational record. Tax officers do not need perfect certainty to raise a high-stakes theory. They need a coherent narrative that survives the self-assessment architecture long enough to shift compliance friction back onto the taxpayer.

The law of proof is quietly adapting to that reality. The Bharatiya Sakshya Adhiniyam, 2023, in force since 1 July 2024, expressly preserves admissibility for electronic or digital records and lays down the certification framework for electronic records. That does not mean every screenshot becomes gospel. It does mean disputes increasingly turn on how the record was produced, what device or system generated it, whether integrity safeguards can be described, and whether the chain from source to output has been documented with discipline. In tax searches, those questions are no longer courtroom technicalities. They are strategy questions from day one of the panchnama onwards.

This is where metadata becomes more dangerous than the headline document. A loose Excel file can sometimes be explained away as modelling. A file whose properties show repeated revisions after vendor meetings, sharing across finance staff, alignment with invoice series, and correlation with bank credits becomes harder to dismiss as casual chatter. Deleted files can also be double-edged. The act of deletion does not prove suppression, but in a search case it can support an adverse reading when paired with restored fragments, cloud sync records or inconsistencies in employee explanations. For promoters and CFOs, the second-order effect is obvious: weak digital governance now creates tax incidence risk even when the substantive transaction has a defensible commercial story.

Metadata risk is really governance risk

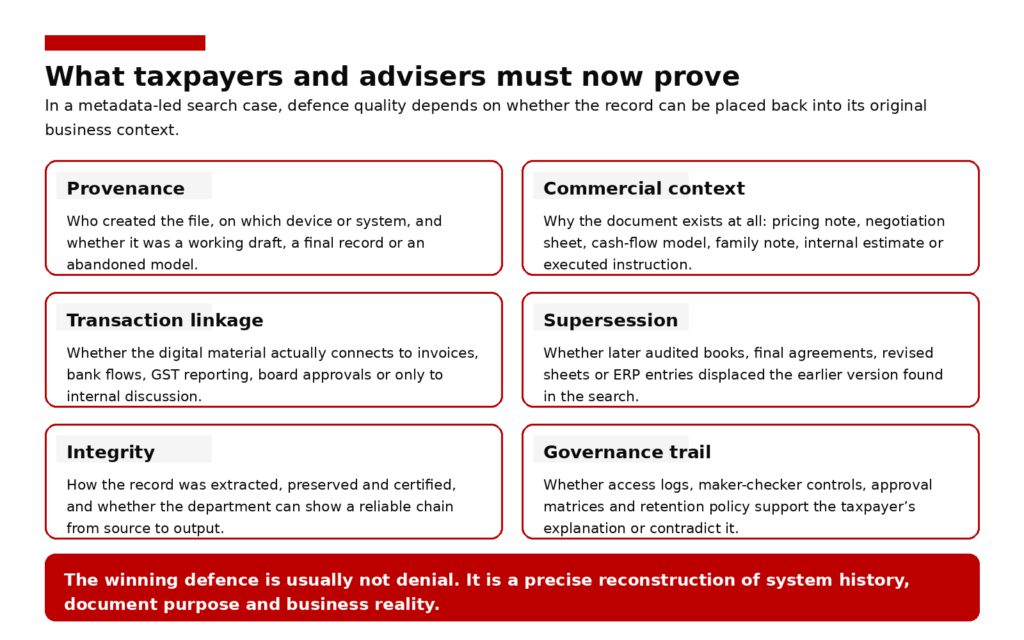

For the middle class and small businesses, the lesson is less dramatic but just as uncomfortable. Retail investors, salaried executives with side ventures, consultants, doctors and small manufacturers leave dense digital footprints without enterprise-grade controls. Personal and business communication often sit on the same devices. Draft term sheets, unexecuted side letters, cash-tracking notes, family office spreadsheets and broker chats can all travel together. Search cases involving such records will often be fought over context, not authenticity alone. That raises the cost of defence. Advisers must now reconstruct workflows, device usage and document provenance instead of merely reconciling ledger entries.

Tax professionals are already feeling the workload migration. The strongest defence in a digital-evidence search case is rarely a broad claim that the material is “dumb data”. It is a granular rebuttal: who created the file, when, on which system, for what provisional purpose, whether the underlying transaction ever crystallised, and whether the record was later superseded by audited books, board approvals, GST disclosures or banking channels. That demands closer work between tax counsel, forensic experts, ERP teams and internal finance staff. It also changes engagement economics. Practitioners who understand metadata, audit logs and evidentiary certificates will command a premium because the case now turns as much on system architecture as on statutory interpretation.

What this means for advisers, companies and taxpayers

Large corporates face a different risk. Their formal controls are stronger, but their data exhaust is much wider. Enterprise systems retain version histories, approval matrices, access logs, maker-checker trails and communication archives that can either protect or hurt them. Where a company’s internal controls match its tax position, digital evidence can shorten the dispute and narrow the allegations. Where the control environment says one thing and the return says another, metadata can become a revenue weapon. That is why digital retention policy is no longer just an IT or privacy issue. It is part of tax risk management, transfer-pricing readiness, investigation response and board-level governance.

None of this means taxpayers are doomed in the age of metadata. Search assessments still rise or fall on legal thresholds, jurisdiction, relevance, linkage to undisclosed income and the quality of corroboration. Courts have never loved additions built on isolated scraps. But taxpayers who treat digital records as incidental are making a category error. In 2026, metadata doesn’t merely decorate the evidence. It organises the story. And in tax litigation, the side that controls the story often controls the settlement pressure, the litigation timeline and, eventually, the outcome.

The administrative signal from government is also unmistakable. The Department’s 2026 directory notes the release of a Search and Seizure Manual, 2025, alongside other office-procedure manuals. That sounds internal, but it matters externally. Better standardisation tends to make evidence packaging tighter, not looser. A system that documents extraction, preservation and follow-up more consistently reduces the room for sloppy challenges, while increasing pressure on taxpayers to contest substance rather than merely procedure. The gain for the state is enforcement efficiency. The cost is that weak record hygiene, once survivable, becomes expensive much faster.

Sources & Data Points

– Income-tax Act, 2025 [as amended by Finance Act, 2026] – commencement from 01-04-2026.

– FAQs on Interplay and Transition – Income-tax Act, 2025 – clarifies that searches initiated before 01-04-2026 continue under the Income-tax Act, 1961 by virtue of the saving clause.– Departmental Directory 2026 – records release of the Search and Seizure Manual, 2025, indicating administrative standardisation within the department.