Section 263 survives the statutory rewrite as section 377, but the new regime makes the revision clock cleaner, the paperwork sharper, and weak assessment records easier to attack.

The renumbering that matters less than advertised

Section 263 begins this story because that is still the phrase taxpayers, counsels and search queries use. In practice, revision notices seldom arrive because someone in the department has uncovered a cinematic fraud. They usually arrive because the assessment order looks thin, the questionnaire looks generic, or a large claim appears to have been accepted without a defensible audit trail. The Income-tax Act, 2025 does not retire that supervisory instinct. It renumbers it. CBDT’s press release bringing the new law into force on 1 April 2026 says the rewrite simplifies and modernises the statute “without altering the underlying tax policy”. That line is the right place to start.

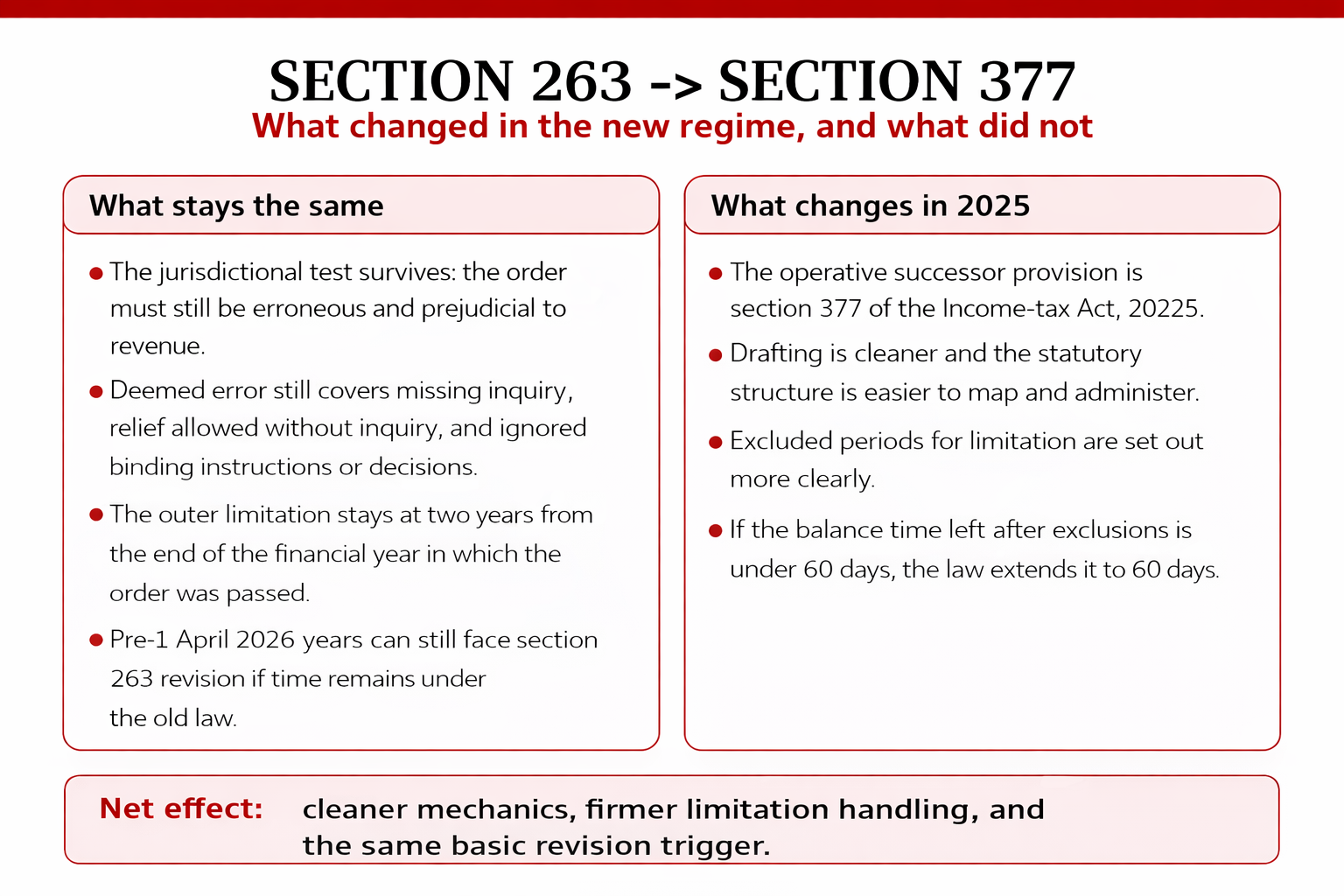

The new Act was passed by Parliament in August 2025, received presidential assent on 21 August 2025, and took effect from 1 April 2026. Departmental material describes it as a simplification exercise that cut the statute from 819 sections to 536 while preserving policy substance. For revision power, that matters a great deal. The legal architecture that practitioners knew under section 263 has not been diluted by fresh taxpayer-friendly drafting. It now sits primarily in section 377 of the Income-tax Act, 2025, and the core trigger remains intact.

Why section 263 became sharper before the rewrite

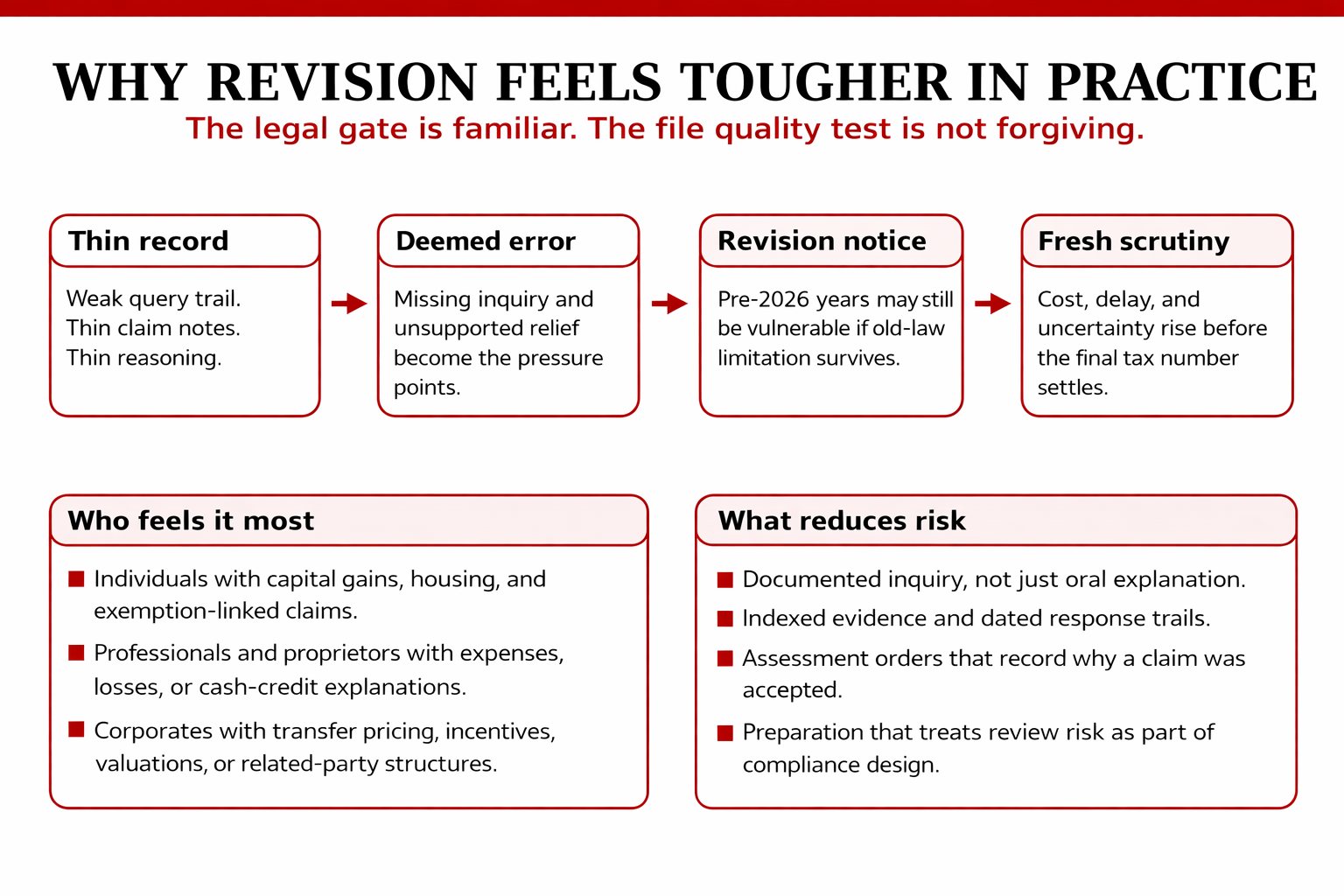

That is why the real expansion story predates the 2025 Act. The important statutory hardening happened when Parliament amended section 263 through the Finance Act, 2015. The official memorandum accompanying that Bill openly said the meaning of an order “erroneous in so far as it is prejudicial to the interests of the revenue” had become contentious. The solution was not to leave the matter to abstract doctrine. It was to codify a deemed-error framework: no inquiry where inquiry should have been made, relief granted without inquiry, disregard of Board directions, and disregard of binding jurisdictional High Court or Supreme Court rulings. Since then, many section 263 battles have turned less on grand constitutional rhetoric and more on whether the assessment file can show real application of mind.

Another widening came later and matters particularly for large businesses. CBDT’s Circular No. 23 of 2022, explaining the Finance Act, 2022, records that Parliament clarified the revision power over Transfer Pricing Officer orders because the earlier text left uncertainty over who could revise them. Section 377 now carries that approach forward in plain terms: it expressly covers orders passed by the Assessing Officer or the Transfer Pricing Officer and also folds in orders under section 166. That means the new regime preserves revision risk not only for routine assessments but also for transfer pricing and value-sensitive corporate disputes where the stakes are much higher.

Section 377 changes the mechanics, not the trigger

CBDT’s March 2026 FAQ on the transition answers the central question in unusually direct language. The jurisdictional requirement, it says, continues: the order must still be both erroneous and prejudicial to the interests of the revenue. That is the legal gate. So the claim that the 2025 Act has quietly lowered the threshold for revision is too broad. The state has not received a brand-new power to revise merely because it dislikes an Assessing Officer’s view. In law, section 377 still demands jurisdictional satisfaction before revision can stand.

Even so, the administration did gain something valuable: cleaner mechanics. Section 377(4) keeps the outer limitation period at two years from the end of the financial year in which the order sought to be revised was passed. But section 377(6) now sets out the excluded periods more clearly, including rehearing time and court-ordered stay periods. Section 377(7) adds an explicit rule that if the residual time left after those exclusions is under 60 days, the limitation automatically stretches to 60 days. CBDT’s transition FAQ confirms there is no substantive change in the outer limit, but it also confirms a tidier computation framework. Tidy computation usually helps the department, because technical disputes over counting days shrink.

Section 377 also preserves a carve-out that many taxpayers misread. Where the assessment order has already been carried in appeal, the Commissioner’s revision power extends to matters not considered and decided in that appeal. That does not sterilise the entire assessment order. It merely walls off the issues already adjudicated. In real litigation, that means a taxpayer can succeed on one contested point before an appellate forum and still face revision on another claim that the assessment record handled badly. The result is layered procedure rather than closure.

Why the power may feel harsher anyway

If the law is substantially the same, why does the power still look more threatening in the 2025 Act era? One reason is administrative standardisation. A shorter, cleaner statute is easier to train on, easier to map against internal risk flags, and easier to operationalise inside analytics-led supervision. The Department’s own 2026 material describes a broader shift toward non-intrusive, risk-based, data-driven compliance management. That kind of machinery does not reduce revision exposure. It often makes the selection of weak assessments more systematic. The weapon is old; the targeting can improve.

For the Indian middle class, section 263 is not everyday vocabulary, but its effects travel through ordinary files. Capital gains reinvestment, housing-related claims, business-loss set-off, cash-credit explanations in small proprietorships, expense claims in professional practices, and exemption-linked computations are all shaped by a self-assessment architecture that depends on a competent assessment record. When that record is skeletal, revision can extend uncertainty, delay refunds, and force a second round of compliance even where the eventual tax demand is not dramatic. Compliance friction becomes its own burden. That is one reason the power often feels harsher than the statutory text alone suggests.

For tax professionals, the lesson is hard but clear: build the assessment file as if a sceptical Commissioner will read it two years later. In the new regime, polished legal submissions matter less than demonstrable inquiry, indexed evidence, written response trails, and assessment orders that show why a claim was accepted. For the corporate sector, especially groups dealing with transfer pricing, incentives, valuation disputes, or related-party structures, section 377 means governance has to travel backwards into assessment preparation itself. A strong position recorded badly is now a weak asset. That is where “erroneous and prejudicial” gets weaponised – not because the statute suddenly changed its philosophy, but because poor record-building invites it.

The real question is not wording, but discipline

So is revision easier to invoke in the new regime? In substance, not by much. The sharpest legislative move happened years earlier, when Parliament codified what counts as deemed error, and it happened again when transfer pricing orders were brought more clearly within the revision net. What the 2025 Act does is something more subtle and still important. It preserves the same legal gate, tightens the transition through section 536, cleans up the limitation mechanics, and reduces drafting clutter that used to give taxpayers room to fight on form. Section 263’s successor is not a new weapon. It is the same weapon with a cleaner sheath. In a tax system that wants higher tax buoyancy without openly redrawing the fiscal bargain, that may be the precise design choice.

Sources & Data Points

Income-tax Act, 2025 [30 of 2025], as amended by Finance Act, 2026 – especially section 377 (revision of orders prejudicial to revenue) and section 536 (repeal and savings). Official text hosted by the Income Tax Department.

2. CBDT, FAQs on Interplay and Transition from the Income-tax Act, 1961 to the Income-tax Act, 2025, March 2026 – especially Q7.22 to Q7.25 on fresh revision for pre-2026 years, continuity of the ‘erroneous and prejudicial’ test, limitation, and pending revision matters.

3. CBDT Press Release, ‘Income-tax Act, 2025 comes into force from 1st April, 2026,’ dated 1 April 2026 – for commencement, assent date, and the official statement that the rewrite simplifies the law without changing underlying tax policy.

4. Income Tax Department, Departmental Directory 2026 – introductory note on the reform journey, enactment timeline, and the reduction of the statute from 819 sections to 536.

5. Memorandum Explaining the Provisions in the Finance Bill, 2015 – official explanation for the amendment to section 263 and the codification of deemed-error grounds.

6. CBDT Circular No. 23 of 2022, Explanatory Notes to the Provisions of the Finance Act, 2022 – official explanation of the amendment clarifying revision of Transfer Pricing Officer orders under section 263.