DIN validity after Circular 4/2026 no longer turns on typography alone; the real fight is whether the department can prove a lawful, traceable, system-backed communication issued on time.

DIN validity after Circular 4/2026 is no longer a tidy argument about whether a number appears in the right corner of a tax notice. It is now a harder and more interesting dispute about state authenticity. When a taxpayer receives a notice, draft order, summons or approval, the real question is not cosmetic. It is institutional. Can the Income-tax Department prove that the communication was genuinely system-backed, attributable to a lawful authority, and issued through a traceable audit trail? That trust problem sat behind the original DIN regime. It still does. What has changed is the legal architecture around how that trust may now be proved.

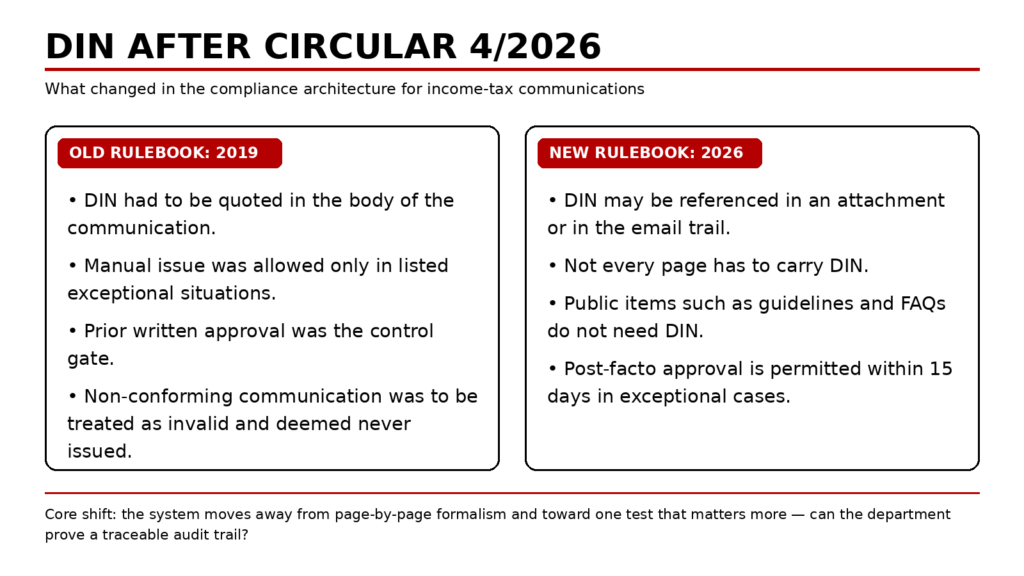

That is why the 2019 circular still matters, even though it no longer governs the field. CBDT Circular No. 19/2019 was framed around a clear administrative anxiety: some notices and orders were being issued manually without a proper audit trail. The Board responded sharply. From 1 October 2019, no communication to an assessee or other person was to be issued without a computer-generated DIN duly quoted in the body of the communication, save for tightly framed exceptional situations. It also imposed a hard consequence: a communication not in conformity with paragraphs 2 and 3 of that circular was to be treated as invalid and deemed never to have been issued. That language gave DIN litigation its edge. It turned process into jurisdiction.

Circular No. 4/2026, issued on 31 March 2026, does not abandon DIN discipline. It rewrites what counts as sufficient referencing. The circular says a communication may be referenced by DIN not only in the communication itself, but also through a separate attached document mentioning DIN, or even in the email correspondence. It also says every page of the communication need not separately carry DIN. Just as importantly, public communications such as guidelines and FAQs are kept outside the DIN requirement. That is not a drafting nicety. It marks a decisive move away from page-by-page formalism and toward a broader evidentiary standard of notice authenticity.

The other visible shift is procedural softness. Under the 2019 regime, manual issuance in exceptional situations required prior written approval. Under Circular 4/2026, exceptional cases remain broadly familiar—technical difficulty, lack of electronic access while discharging official duties, PAN migration delay, PAN not being available, or system functionality being unavailable—but the circular now permits post-facto approval within 15 days of issue, based on reasons recorded in writing. For situations covered by paragraphs 3(a), 3(b) and 3(c), the communication must then be uploaded on the system with appropriate DIN referencing within 15 working days. In policy terms, CBDT has chosen to reduce compliance friction for the Department while trying to preserve an audit trail after the event. That makes administration easier. It also makes disputes more document-heavy.

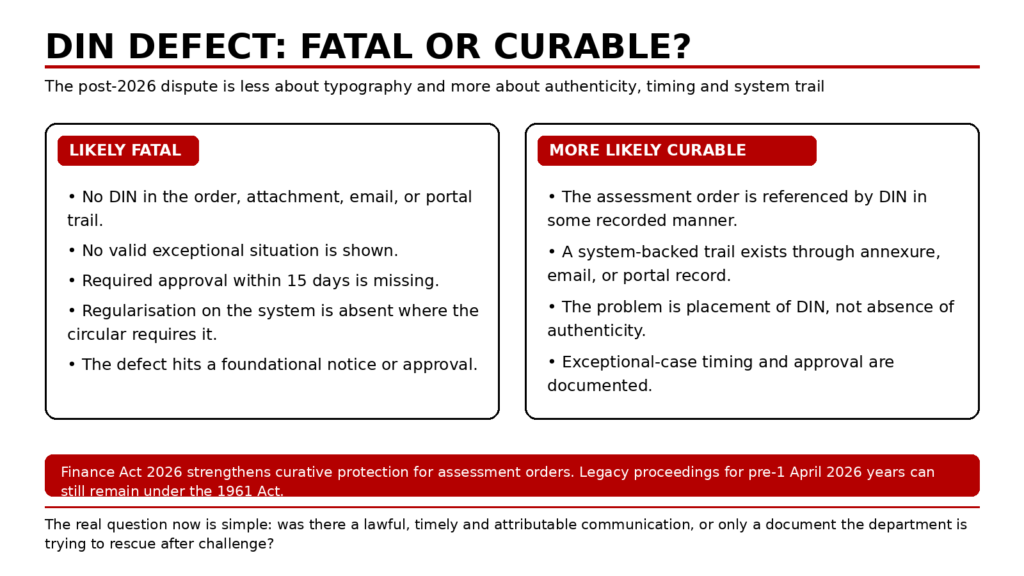

But the real centre of gravity has shifted from the circular to the statute. The Finance Bill, 2026 inserted section 292BA into the Income-tax Act, 1961, and the accompanying memorandum states that the amendment is retrospective from 1 October 2019. The language is narrow, but potent: no assessment under the 1961 Act shall be invalid merely because of any mistake, defect or omission in quoting a computer-generated DIN, so long as the assessment order is referenced by such number in any manner. The Income-tax Act, 2025 now carries parallel language in section 522(2). That phrase—in any manner—is the hinge on which the next round of DIN litigation will turn. It does not erase the DIN requirement. It does make it materially harder to knock out an assessment order on placement defects alone.

The statutory design goes further under the new Act. Section 522(3) of the Income-tax Act, 2025 says that electronic approvals in relation to assessment, reassessment or recomputation proceedings are administrative and supervisory in nature and shall not be invalid because of insufficiency of reasons or defects in authentication or communication, including absence of digital signature, where the approval has been granted electronically. That does not end controversy. It does, however, show the legislative mood. Parliament is plainly trying to stop revenue proceedings from collapsing on technical infirmities once a system trail exists. Read with section 523, which limits late service objections where the assessee has appeared or cooperated without timely protest, the message is clear: post-2026 tax litigation will reward early, precise objections, not delayed procedural ambushes.

So where does that leave the fatal flaw versus curable lapse debate? The cleanest answer is that DIN validity after Circular 4/2026 has become document-specific. If there is no DIN at all in the order, attachment, email chain, or portal trail; if the Department cannot show that an exceptional case genuinely existed; if the required approval within 15 days is missing; or if the later system upload demanded by the circular never happened, the taxpayer still has a serious jurisdictional challenge. That is especially true where the impugned paper is not a downstream assessment order but a foundational notice, sanction, approval or satisfaction document. On the other hand, where the Department can show a contemporaneous DIN trail in some recorded manner, the defect begins to look curable rather than fatal. That is the new dividing line.

This is also why transitional law now matters. CBDT’s official 2026 FAQs on interplay and transition make clear that if a search was initiated before 1 April 2026, the entire proceeding—including assessment, reassessment, penalty and appeal—continues under the Income-tax Act, 1961 as if the new Act had not been enacted. The same FAQ confirms that revision proceedings for pre-2026 years can also continue under the old Act. So the market will live in a two-statute world for some time. Legacy proceedings will still attract the stricter old-law contest over DIN compliance, while post-2026 years will increasingly be filtered through section 522’s curative structure. For litigators, that means the first question is no longer Is there a DIN defect? It is Which Act governs this defect?

For the middle class taxpayer, this may sound technical, but it changes the burden of vigilance. A missing DIN on page one used to be a comparatively visible signal. Now the taxpayer may need to examine the portal download, annexures, covering email and timing of later regularisation. For tax professionals, the practical effect is sharper still. File review now becomes a chain-of-custody exercise: document type, governing statute, DIN location, email metadata, exception invoked, approval timing, and system upload history. For large companies, the second-order effect is straightforward. Preserve the whole communication stack. In an era of faceless administration and automated workflow, jurisdiction may turn less on rhetoric and more on digital record discipline.

The balanced view, then, is this. DIN validity after Circular 4/2026 has not been diluted into irrelevance, and it has not survived in its old absolutist form either. The Board still insists on traceability. Parliament has simply made it harder to weaponise formatting defects against assessment orders where authentic system reference can be shown. That means weak DIN cases will now get weaker, but strong ones may get stronger because the fight has moved from typography to proof. The serious issue is no longer whether the number was printed in the perfect place. It is whether the State can prove lawful, timely, attributable issuance. That is where taxpayers will still win. And that is where Revenue will now try hardest not to lose.

Sources & Data Points

1. CBDT Circular No. 19/2019 dated 14 August 2019 on generation, allotment and quoting of DIN in notices, orders, summons, letters and correspondence. Official PDF

2. CBDT Circular No. 4/2026 dated 31 March 2026 on referencing by Document Identification Number (DIN). Official PDF

3. Finance Bill, 2026, clause 26, inserting section 292BA into the Income-tax Act, 1961, along with the memorandum explaining its scope and retrospective effect from 1 October 2019. Official PDF

4. Income-tax Act, 2025 as amended by the Finance Act, 2026, especially section 522(2), section 522(3) and section 523. Official PDF

5. CBDT FAQs on Interplay and Transition from the Income-tax Act, 1961 to the Income-tax Act, 2025, including the answers on pre-1 April 2026 search and revision proceedings. Official PDF