Block assessment is back in Indian tax administration, promising faster search cases and cleaner enforcement, yet reopening an older question: how much procedural compression can constitutional tax administration bear?

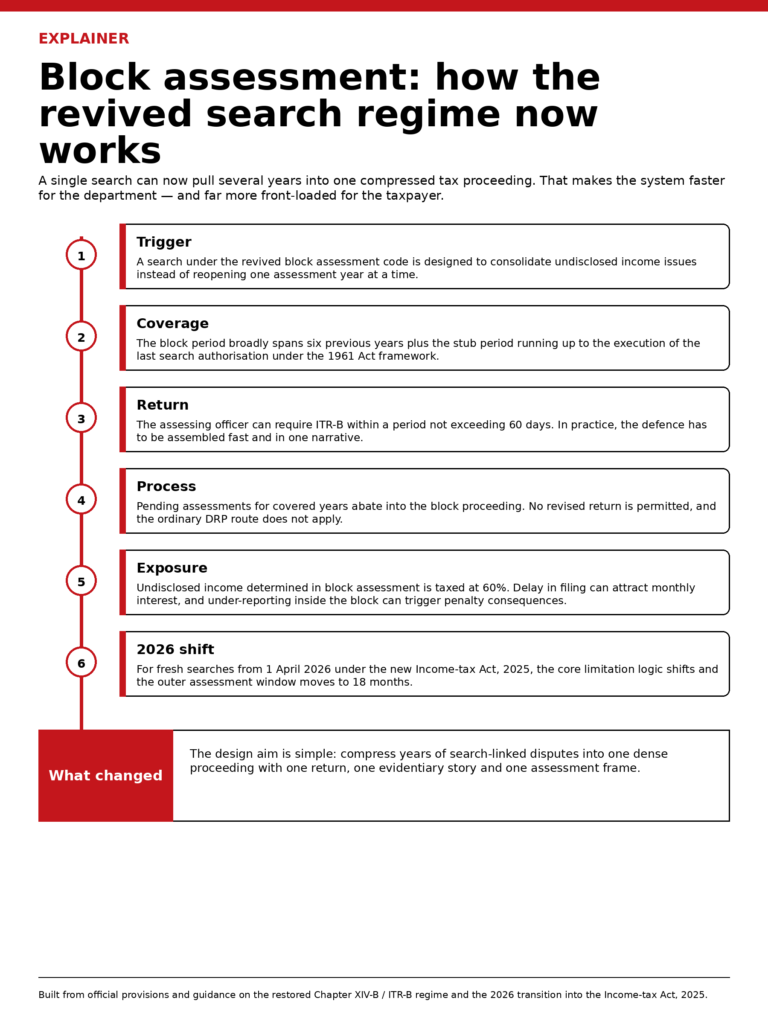

Block assessment is back, and that matters because India’s tax administration has effectively admitted that its post-2021 search framework was too fragmented for serious search cases. The official memorandum to the Finance (No. 2) Bill, 2024 says the department had ended up with staggered, year-by-year proceedings, often reopening only the time-barring year first and keeping the searched taxpayer in litigation for years. The revival of block assessment from 1 September 2024 is the legislative answer: one consolidated proceeding for undisclosed income found in a search or requisition, not a long chain of reopenings.[1]

Why block assessment returned

The policy logic is straightforward. Search is meant to uncover concealed income, and concealment rarely respects assessment-year boundaries. The 2024 memorandum explicitly framed the restored regime as a way to secure early finalisation, coordinated investigation and fewer overlapping proceedings.[1] Under the revived Chapter XIV-B architecture, the block period for searches under the 1961 Act covers six previous years plus the stub period from 1 April of the year of search until the last authorisation is executed; pending assessments and reassessments for those years abate into the block proceeding; and the undisclosed income so determined is taxed at 60% under section 113.[1][3]

That is a material departure from India’s ordinary self-assessment architecture. Annual compliance assumes year-specific reporting, notice, explanation and adjudication. Block assessment compresses that chronology into a single search narrative. The Income Tax Department’s updated guidance now describes it as a special procedure for search cases initiated on or after 1 September 2024, with automatic abatement of pending proceedings and one consolidated assessment of total undisclosed income for the block period.[3]

How the block assessment workflow now changes

The operational face of this return is ITR-B. The notified form requires disclosure not only of undisclosed income for the block period, but also earlier return history across the covered years, the DIN and date of the section 158BC notice, and taxes paid on the undisclosed income.[4] The procedural edges are equally sharp. The Assessing Officer may require the block return within a period not exceeding 60 days, with only a narrow 30-day extension in audit-linked cases; no revised return is permitted; and the DRP route under section 144C does not apply.[3][5] Search defence, in other words, becomes more centralised, more documentary and more front-loaded.

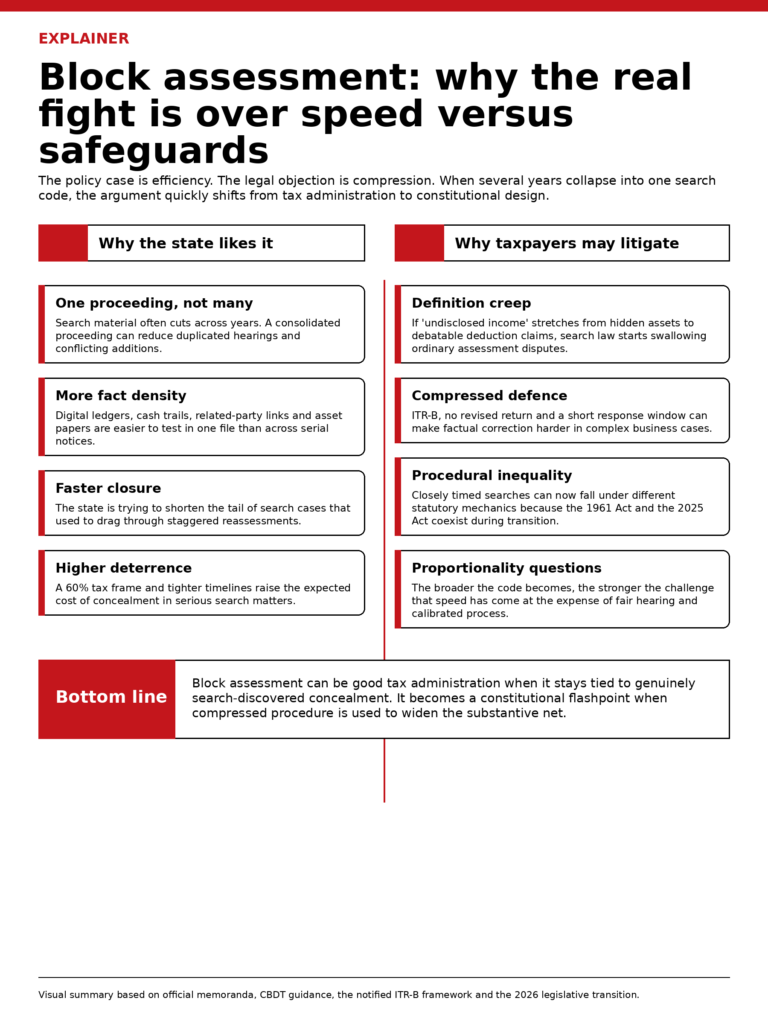

That gives the regime a real administrative advantage. A single proceeding can cut duplicated hearings, inconsistent additions and repeated use of the same seized material across multiple years. For businesses, that may actually reduce compliance friction in the aggregate. A coordinated assessment is often better suited to cash trails, property links, digital ledgers and related-party patterns than a serial procession of notices. From the revenue side, block assessment is a design for density: more facts in one file, fewer files for the same search.

Why the block assessment fight may intensify

But block assessment is also a concentration of state power. Once pending proceedings abate, the taxpayer loses the relative comfort of year-specific contests and enters a higher-stakes code built around “undisclosed income”, a flat 60% rate and a constrained return process. The department’s own explainer makes the consequences plain: no revised return, no section 143(1) processing, 5% monthly interest if the block return is not furnished in time, and a 50% penalty on the portion of undisclosed income ultimately determined above what the taxpayer declared.[3] A regime this compressed will inevitably invite arguments about fair hearing, proportionality and the limits of administrative discretion.

The definitional issue is even more important. The official guidance says undisclosed income is not limited to cash, bullion, jewellery or unrecorded assets; it also includes incorrect claims of expenditure, exemption, deduction or allowance.[3] That is where the next battleground sits. In policy terms, the state wants to capture not just hidden receipts but also concealed tax incidence created through false claims. In legal terms, the broader the concept becomes, the greater the risk that ordinary interpretation disputes get pulled into a search code designed for more serious concealment. The line between evasion and an arguable claim matters far more when block assessment replaces ordinary assessment mechanics.

The 2026 transition complicates block assessment again

The story became more complicated on 1 April 2026. The Income-tax Act, 2025 carries the block assessment framework forward in renumbered form, and the Finance Act, 2026 adjusts its mechanics again. For searches under the new Act, section 296 now measures the primary limitation from the quarter in which the search was initiated and extends that period to eighteen months; the official memorandum says this change was made because group searches produced mismatched limitation dates when the clock ran from the last authorisation.[5][6] The 2026 amendments also narrow the block period for an “other person” in certain cases where the undisclosed income relates only to a limited period or a single earlier tax year.[5][6]

That may improve coordination, but it also creates transition friction. The official FAQs on interplay and transition say that if a search was initiated before 1 April 2026, the entire proceeding, including assessment, penalty and appeal, continues under the repealed 1961 Act as if the new Act had not been enacted.[7] So two search codes now coexist, depending on when the trigger event occurred. That is fertile ground for litigation over limitation, carry-through of procedural rights and unequal treatment between closely timed cases.

What block assessment means for taxpayers and advisers

For the middle class, block assessment is not a mass-filing issue. For promoters, family businesses, real-estate players and cash-sensitive sectors, it is a serious change in risk. Better books, cleaner banking trails, tighter reconciliations and disciplined return history now matter more because one search can recast several years at once. For tax professionals, the work shifts from year-by-year defence to integrated fact architecture. ITR-B reinforces that shift because it forces the taxpayer to present the block story in one instrument.[4] Corporate groups, meanwhile, must pay extra attention to cross-border and transfer-pricing segregation, because the department’s guidance says income relating to international or specified domestic transactions for the relevant stub period is assessed separately under other provisions, not folded into the block computation.[3]

Block assessment is therefore neither a crude revenue grab nor a clean administrative triumph. It is a serious anti-evasion redesign built to trade procedural spread for procedural concentration. If it stays anchored to genuinely undisclosed income arising from search material, it could reduce litigation and improve enforcement quality. If it turns into a broad device for converting every disputed claim into search income under a compressed code, the efficiency story will not last. The constitutional one will.

Sources & Data Points

- [1] Union Budget 2024-25, Memorandum Explaining the Provisions in the Finance (No. 2) Bill, 2024, section C on the introduction of block assessment. Used for the policy rationale, the six-year block structure, abatement, and the restored Chapter XIV-B framework. Official link

- [2] Income Tax Department, “Assessment” page, Block Assessment explainer, updated 30 March 2026. Used for current official procedure, definition of undisclosed income, ITR-B filing mechanics, exclusion of revised returns, DRP inapplicability, and filing deadlines. Official link

- [3] Form ITR-B (Income Tax Department PDF, 2025), return for block assessment under section 158BC read with Rule 12AE of the Income-tax Rules, 1962. Used for DIN capture, return-history disclosure and the structure of the notified block return. Official link

- [4] Income-tax Act, 2025, as amended by the Finance Act, 2026, especially sections 292 to 296. Used for the renumbered block assessment code, the eighteen-month completion timeline, and the treatment of searches initiated on or after 1 April 2026. Official link

- [5] Finance Bill, 2026 / Memorandum explaining the provisions, clauses 64 and 65. Used for the official rationale behind narrowing certain “other person” block periods and shifting the limitation trigger from the financial year-end model to the end of the quarter. Official links: Finance Bill | Memorandum

- [6] FAQs on Interplay and Transition from the Income-tax Act, 1961 to the Income-tax Act, 2025, updated April 2026, especially Q8.22. Used for the rule that searches initiated before 1 April 2026 continue under the repealed 1961 Act despite post-commencement proceedings. Official link