In 2026, a tax opinion survives less on elegant citation than on fact discipline, disclosure quality, and a documentary trail that can withstand a digital proceeding.

The tax opinion is now an evidentiary file

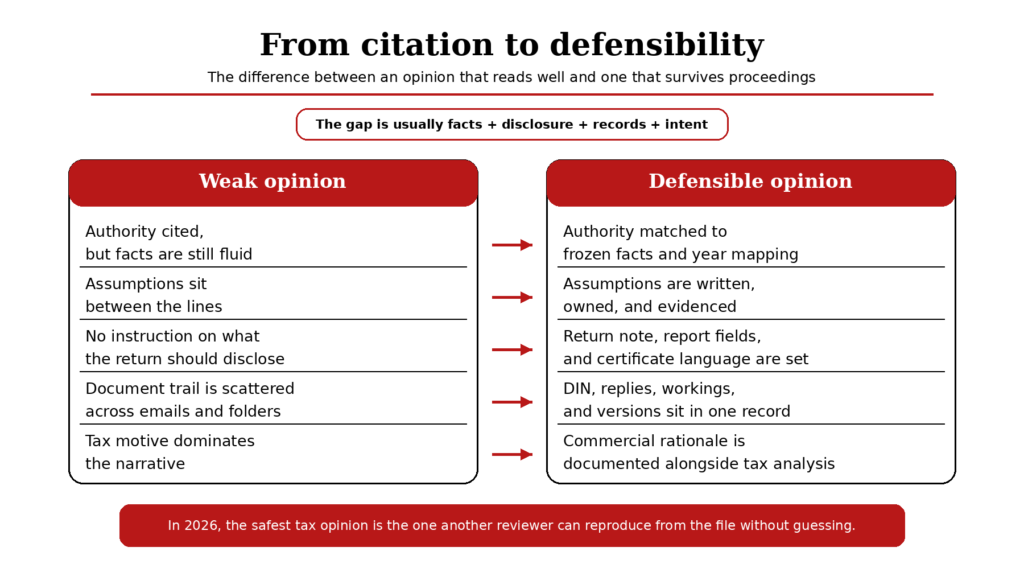

Tax opinion work in India has entered a harsher decade. The old assumption was comforting: find a plausible view, anchor it in a section, add a case note, and the file is ready. That assumption is now expensive. In a system shaped by self-assessment, AIS, specified financial transaction reporting, e-proceedings and expanding digital trails, a tax opinion is no longer judged only by whether the legal proposition is arguable. It is judged by whether the factual record, disclosure posture and internal process can carry that proposition through assessment, penalty and appeal.

Authority still matters. It always will. But in 2026, authority without statute control is a trap. India has moved into the Income-tax Act, 2025 from 1 April 2026, while a wide range of pending and pre-commencement proceedings continue under the 1961 Act through the saving provisions. That means a defensible tax opinion must start with a transition map before it starts with a conclusion. For one tax year, the old law may govern the deduction, the old proceeding may survive repeal, and the new Act may govern later-year utilisation, compliance forms or procedural posture. Opinions that quote the right principle but from the wrong statutory frame will look learned and still fail.

Disclosure, intent and downside

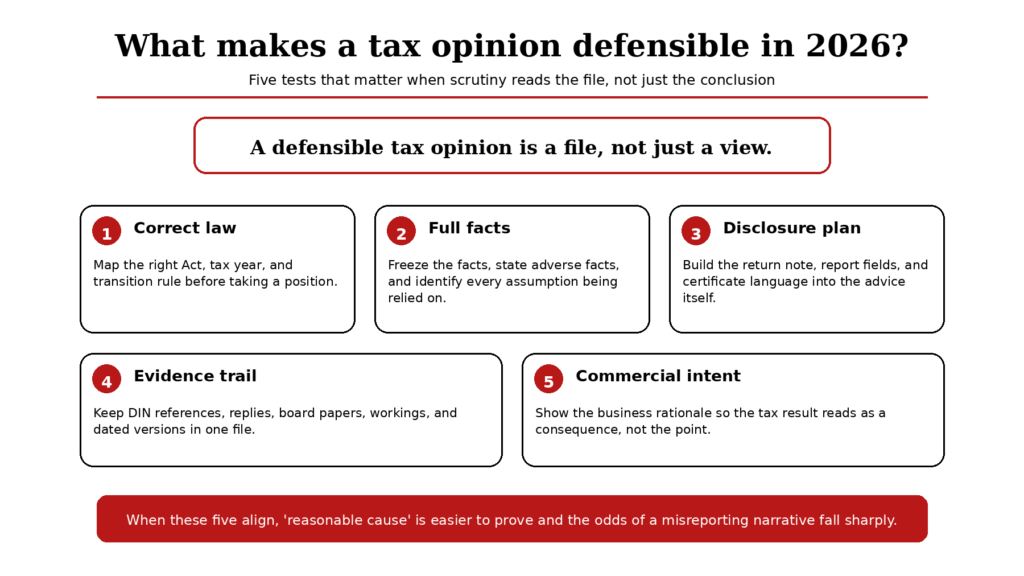

Disclosure now does more work than stylistic cleverness. The penalty architecture under the 2025 Act makes that plain. Under-reported income does not include an item where the assessee offers a bona fide explanation and has disclosed all material facts to substantiate it. The same provision also gives relief where transfer pricing adjustments arise but the taxpayer maintained prescribed information and documents, declared the transaction, and disclosed all material facts. That is not a drafting footnote. It is a design instruction. A serious tax opinion in 2026 must tell the client what has to be disclosed, where it must be disclosed, and what supporting material must sit behind that disclosure. Silence is no longer prudence by default. Often it is the fact pattern that converts a dispute into misreporting.

That distinction matters because intent is now inferred from conduct, not declared in prose. The statute keeps the ordinary penalty on under-reported income at 50% of the tax payable, but pushes misreporting to 200%. The catalogue of misreporting is revealing: misrepresentation or suppression of facts, non-recording of investments, false entries, unsubstantiated expenditure claims, and failure to report international transactions. The practical lesson is severe. A tax opinion cannot be written as a detached legal essay divorced from books, emails, board papers, inter-company agreements, valuation workings and return disclosures. If those materials point one way and the opinion points another, the opinion becomes evidence against the taxpayer rather than protection for the taxpayer.

Process is now part of the legal position

Process, then, is no longer back-office hygiene. It is part of substance. The department’s own e-Proceedings guidance says the system makes it easier to track submissions and maintain records for future reference. The redesigned 2026 return forms are built around traceability: they ask for DIN where a return is filed in response to notices or orders, and they preserve reference points such as APA-linked filings. Official FAQs on forms under the 2026 Rules also note that the UDIN feature introduced in Form 146 enables real-time verification of a chartered accountant’s certificate through the ICAI API. The direction of travel is unmistakable. Authenticity, source tagging and response history are being embedded into compliance architecture itself. A defensible tax opinion therefore needs version control, dated fact memoranda, management representations, document indexes and a clear record of what assumptions counsel or the adviser actually relied on.

Why scrutiny feels harder in 2026

That is one reason higher scrutiny feels different today. Scale has changed. The Receipt Budget for 2026-27 says 8.67 crore income-tax returns for AY 2024-25 had already been filed up to 30 November 2025, reporting aggregate taxable income of Rs 117.22 lakh crore and gross tax payable of Rs 18.70 lakh crore. CBDT’s latest time-series release shows provisional direct tax collections of Rs 22.26 lakh crore in FY 2024-25, with the direct-tax-to-GDP ratio at 6.73% and direct taxes accounting for 58.81% of total tax revenue. When the base is that large, scrutiny is not only about raids or headline litigation. It is about structured mismatch detection, selection, risk filters and cleaner penalty pathways. The state does not need every case. It needs enough cases where the file cannot explain itself.

That has second-order effects across the market. For the Indian middle class, a weak opinion increasingly means practical nuisance rather than abstract doctrinal risk: delayed refunds, repeated explanations, disclosure mismatches and a long trail of portal responses. For tax professionals, the value is shifting from after-the-fact citation to ex-ante file architecture. The best adviser is not merely the one who knows the proposition, but the one who can define the question presented, freeze the facts, isolate assumptions, identify contrary authority, specify return and report disclosures, and create a record that another professional could defend two years later. For corporates, especially those with related-party, cross-border or restructuring positions, defensibility is now a governance issue. Audit committees and boards do not want a clever answer. They want a position that can survive an assessment folder being opened line by line.

Transfer pricing is the clearest template

Transfer pricing shows the future most clearly. Indian law already requires a report from an accountant for international and specified domestic transactions, and the 2026 forms framework continues with dedicated forms for safe harbour, APA applications, annual APA compliance reports and transfer pricing reporting. In the Budget for 2026-27, the government has also signalled faster, more automated certainty mechanisms for information technology services and a quicker APA pathway. The message is not that litigation disappears. It is that the administration is willing to reward contemporaneous structure, standardised disclosure and disciplined benchmarking more than retrospective storytelling. That logic is spilling beyond transfer pricing into mainstream tax practice.

What a defensible tax opinion looks like in 2026

So what makes a tax opinion defensible in 2026? Not authority alone. Not disclosure alone. Not process alone. And not some abstract statement of benign intent. The defensible tax opinion is sequenced properly. It identifies the governing law and transition rule. It sets out all material facts, including adverse ones. It states assumptions that can be verified. It tells the client exactly how the position should appear in the return, report, note or certificate. It preserves the evidence trail. It explains the commercial objective so the tax result is seen as a consequence rather than the whole point. Above all, it is written for the future reader in a proceeding, not for the present client in an email thread. In 2026, that is the difference between a persuasive memo and a position that can actually live through scrutiny.

Sources & Data Points

- Income-tax Act, 2025 [as amended by Finance Act, 2026]

Used for the operative framework on transition, under-reporting, misreporting, transfer pricing reporting, penalty procedure, and reasonable-cause relief. https://www.incometaxindia.gov.in/documents/d/guest/income_tax_act_2025_as_amended_by_fa_act_2026-pdf

- CBDT press release: Income-tax Act, 2025 comes into force from 1 April 2026

Used to anchor the 2026 commencement of the new direct-tax statute. https://www.incometaxindia.gov.in/documents/d/guest/press-release-income-tax-act-2025-comes-into-force-from-01-april-2026-pdf

- Budget Speech 2026-27 – Part B, Direct Taxes

Used for the government’s stated 2026 policy direction on redesigned forms, integrated assessment-penalty architecture, technical defaults being converted into fee, and faster certainty mechanisms. https://www.indiabudget.gov.in/doc/budget_speech.pdf

- Receipt Budget 2026-27

Used for the latest official return-filing and taxable-income figures: 8.67 crore ITRs for AY 2024-25 up to 30 November 2025, aggregate taxable income, and gross tax payable. https://www.indiabudget.gov.in/doc/rec/allrec.pdf

- CBDT Time Series Data: Financial Year 2000-01 to 2024-25

Used for provisional FY 2024-25 direct tax collections, direct-tax-to-GDP ratio, and direct taxes as a share of total tax revenue. https://www.incometaxindia.gov.in/documents/20117/6715095/Final-time-series-data.pdf/99b3f1e8-592e-c841-ee96-b4c3d7c31c25?t=1766702813555

- Income Tax Department – e-Proceedings FAQ

Used for the department’s own articulation that e-Proceedings reduces compliance burden and helps track submissions and maintain records for future reference. https://www.incometax.gov.in/iec/foportal/help/respond-to-e-proceedings-faq

- Income Tax Department – Annual Information Statement (AIS)

Used for the department’s description of AIS as a comprehensive annual tax information statement covering incomes, financial transactions and tax details. https://www.incometaxindia.gov.in/annual-information-statement

- Income Tax Department – Statement of Financial Transaction (SFT)

Used for the department’s explanation of SFT as the reporting mechanism for specified financial transactions. https://www.incometaxindia.gov.in/statement-of-financial-transaction-sft

- FAQs and Guidance Notes on Forms as per Income-tax Rules, 2026

Used for the 2026 forms architecture, including Form 3CEB, APA forms, annual APA compliance reporting, and related transfer pricing forms. https://www.incometaxindia.gov.in/w/faqs-on-forms-as-per-income-tax-rules-2026-1

- FAQs on Interplay and Transition from the Income-tax Act, 1961 to the Income-tax Act, 2025

Used for the official transition reading on saved proceedings, advance rulings and revision continuity after 1 April 2026. https://www.incometaxindia.gov.in/documents/81799/11848482/FAQs-on-Interplay-and-Transition.pdf/05f80c1a-073c-a5d7-fb6f-55509242be53?t=1774082865717