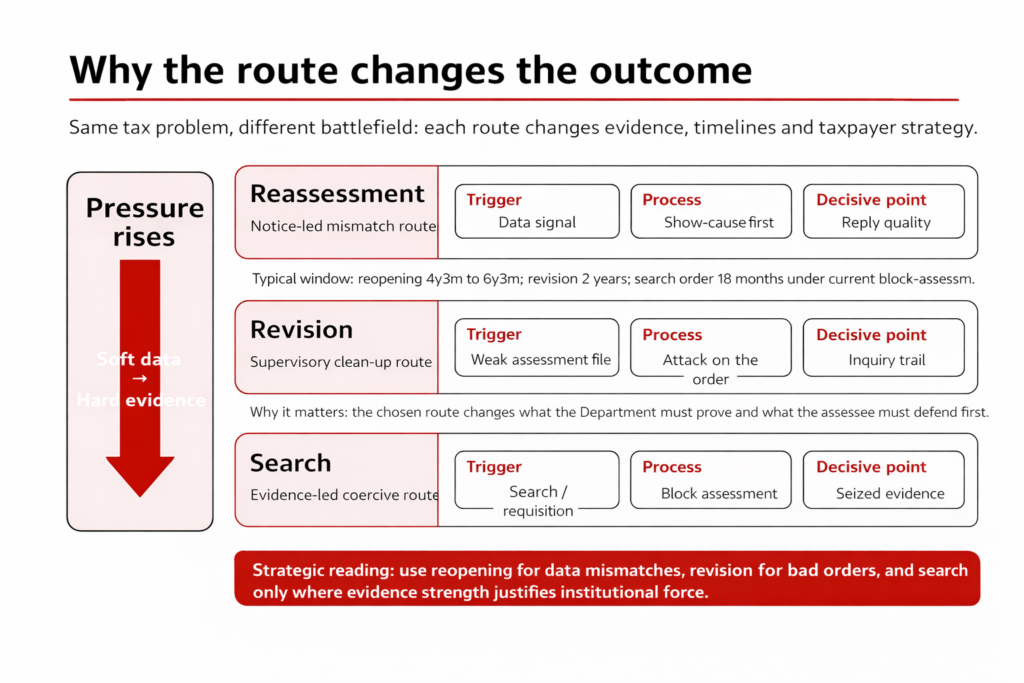

Section 148 is now the mismatch route, revision the supervisory clean-up route, and search the evidence-heavy weapon. For taxpayers, the real risk lies in which forum the Department picks.

The battlefield is the policy

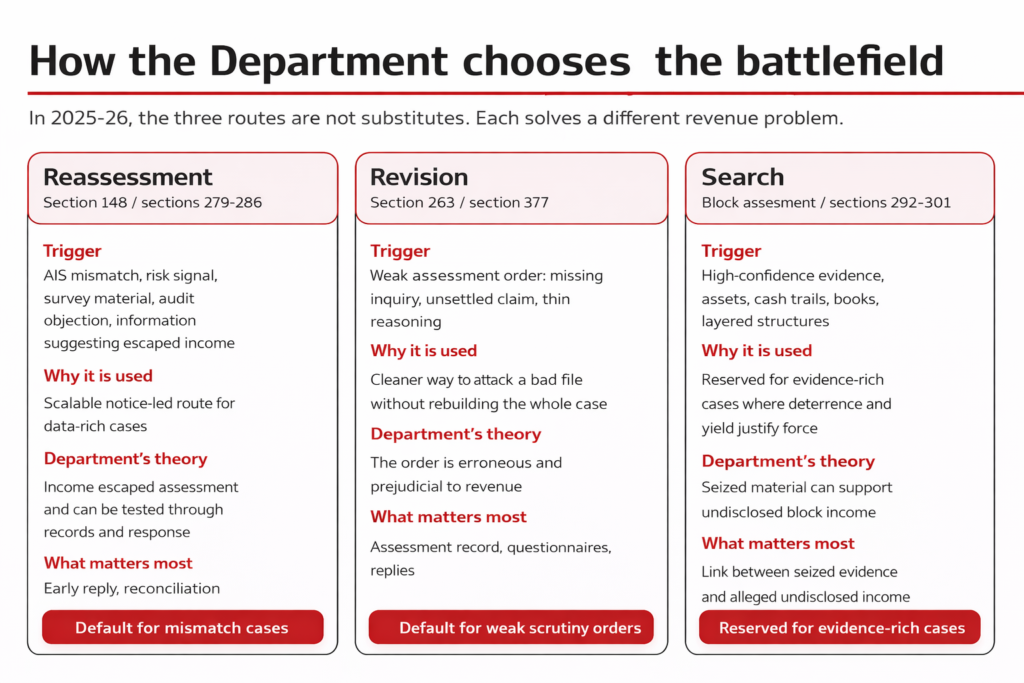

Section 148 is still the phrase most advisers reach for, because in live practice the old labels remain alive even after 1 April 2026. Section 536 of the Income-tax Act, 2025 saves pending proceedings, and even proceedings initiated on or after 1 April 2026 for years beginning before that date, under the repealed 1961 Act. That matters because the Department is not merely collecting more information; it is choosing among three routes. One begins with information suggesting escaped income. Another begins with a superior officer’s view that an assessment is erroneous and prejudicial to the revenue. The third begins with a search warrant. Those choices shape burden, evidence, pressure, and the room available for repair. (Income-tax Act, 2025, section 536; CBDT transition FAQs, March 2026.)

That choice has become more consequential because the tax net is wider and the data fabric is denser. The Receipt Budget 2026–27 says 8,67,67,752 income-tax returns for AY 2024-25 had been filed up to 30 November 2025, reporting aggregate taxable income of ₹1,17,22,177.26 crore. The Economic Survey 2025–26 says return filings rose from 6.9 crore in FY22 to 9.2 crore in FY25. At that scale, the Department cannot treat every mismatch as a raid problem or every weak order as a reopening problem. It has to triage. (Receipt Budget 2026–27; Economic Survey 2025–26.)

Why section 148 remains the default route

Section 148-style reopening, now recast in the 2025 Act through sections 279 to 286, remains the default when the Department has a data trail but not yet a search case. The statute says that information suggesting escaped income can come from the Board’s risk management strategy, audit objections, exchange-of-information material, survey material, Approving Panel directions, and appellate or court findings. The architecture is built for AIS-era administration: the system gathers signals first, then gives a show-cause opportunity, and then decides whether the case is fit for notice. It is scalable, less disruptive than search, and suited to a self-assessment architecture in which mismatches are often digital before they are physical. (Income-tax Act, 2025, sections 279 to 282; Form 168 guidance note on AIS, 2026.)

The Department also has softer tools before it reaches for coercion. In a press release dated 23 December 2025, CBDT said cases for AY 2025-26 had been identified through risk analytics for potentially ineligible deductions and exemptions, that identified taxpayers were being contacted through the NUDGE campaign, and that during FY 2025-26 more than 21 lakh taxpayers had already updated returns for AYs 2021-22 to 2024-25 and paid more than ₹2,500 crore in taxes, while more than 15 lakh returns had already been revised for AY 2025-26. Pair that with the updated-return window now running to 48 months from the end of the relevant assessment year, and the message is clear: the Department would often prefer correction, then reopening, before it escalates. For the middle class, that means more notice-based compliance friction and less cinematic enforcement. For tax professionals, it means responses to section 148A-style show-cause notices are now the first real litigation brief. (CBDT press release, 23 December 2025; Updated Return guidance note, 2026.)

Why revision is the cleaner weapon against weak assessments

Revision is different. Reassessment asks whether income escaped. Revision asks whether the Department’s own order is defective. Section 377 of the 2025 Act, the successor to section 263, keeps the old jurisdictional test intact: the order must be erroneous and prejudicial to the interests of the revenue. It also preserves the deeming logic revenue authorities rely on most. An order may be treated as erroneous if inquiries that should have been made were not made, if relief was allowed without probing the claim, or if the order ignored binding Board directions or controlling court law. That makes revision a sharp instrument. It does not require the Department to build a fresh external case in the way reopening often does. It only has to show that the original assessment file is too thin to deserve finality. (Income-tax Act, 2025, section 377; CBDT transition FAQs, March 2026.)

The 2025 Act also makes revision slightly easier to administer cleanly. The outer two-year limit remains, but the computation is clearer and the statute now gives a 60-day minimum residual period after excluded time is netted out. Limitation disputes are often where aggressive revenue action starts to wobble. A cleaner clock helps the Department defend its revision orders. The second-order effect is plain. Corporate taxpayers, especially in scrutiny-heavy and transfer-pricing matters, face a larger record-quality risk than they sometimes assume. An assessee may be substantively right and still lose time and money if the assessment order does not show the inquiry that should have been made. (Income-tax Act, 2025, section 377(4), (6) and (7).)

Why search is now narrower, but far harsher

Search is no longer just reopening with a louder soundtrack. Effective 1 September 2024, official departmental guidance says search and requisition cases were removed from ordinary reassessment and shifted to the block-assessment framework. Under the 2025 Act, search cases sit in their own track: sections 292 to 301 provide a special procedure, the block period generally covers six preceding tax years plus the stub period up to the search, and pending ordinary assessment or reassessment proceedings for years in the block period abate. The tax cost is blunt. Section 192 taxes total undisclosed block income at 60 percent. This is not the route the Department should prefer for ordinary mismatch cases. It is the route for cases where seized evidence can carry the burden. (Income Tax Department assessment page, March 2026; Income-tax Act, 2025, sections 192, 292, 294 and 301.)

That separation says a lot about administrative preference. Search is operationally expensive, reputationally explosive, and legally unforgiving. The Department’s 2026 directory notes the release of a Search and Seizure Manual, 2025, a reminder that search remains a specialised craft, not a routine substitute for analytics. Finance Act 2026 has also recalibrated the current block-assessment timeline: the order under section 294 is to be passed within eighteen months from the end of the quarter in which the search was initiated or requisition made. That is not the behaviour of a system that wants search to carry the everyday workload. (Departmental Directory 2026; Income-tax Act, 2025, section 296.)

What the Department seems to prefer now

The practical hierarchy is becoming easier to read. For mass compliance issues, the Department increasingly prefers data nudges, revised returns, updated returns, and then reassessment. Where a scrutiny order already exists but looks under-asked, under-reasoned, or mechanically favourable, revision is often the cleaner battlefield because the revenue can attack the file rather than reconstruct the underlying transaction. Search is being reserved for higher-conviction cases involving undisclosed assets, layered books, cash networks, accommodation structures, or evidence that is unlikely to be secured through a notice-based process alone. This is not a softer state. It is a more selective one.

That selectivity changes incentives across the economy. The middle class will experience the tax state less through raids and more through mismatch management. Tax professionals will be judged less by their ability to draft after the fact and more by how well they build files before the fight begins. Corporate India, especially in complex claims, related-party pricing, and large deductions, should worry less about theatrical enforcement and more about supervisory aftershocks from thin assessments. The Department’s preference now is not a single route. It is a sequence: inform, nudge, reopen, revise, and search only when the evidentiary confidence is strong enough to justify the jump. Choosing the battlefield affects outcomes because each route carries a different theory of the case.

Sources and Data Points

Income-tax Act, 2025 [30 of 2025], as amended by the Finance Act, 2026 — especially sections 192, 279 to 286, 292 to 309, 377 to 378 and 536.

Official link: https://www.incometaxindia.gov.in/documents/d/guest/income_tax_act_2025_as_amended_by_fa_act_2026-pdf

• CBDT, FAQs on Interplay and Transition from the Income-tax Act, 1961 to the Income-tax Act, 2025, released in March 2026 — transitional savings, continuing proceedings and route-specific continuity questions.

Official link: https://www.incometaxindia.gov.in/documents/81799/11848482/FAQs-on-Interplay-and-Transition.pdf/05f80c1a-073c-a5d7-fb6f-55509242be53?t=1774082865717

• Receipt Budget 2026–27, Direct Taxes statement — return-filing and aggregate taxable-income data for AY 2024-25 up to 31 December 2025, along with direct-tax receipts.

Official link: https://www.indiabudget.gov.in/doc/rec/allrec.pdf

• Economic Survey 2025–26 — official summary on expansion of the direct-tax base and return-filing growth.

Official link: https://www.indiabudget.gov.in/economicsurvey/doc/Infographics%20English.pdf

• CBDT press release dated 23 December 2025: Initiative to encourage taxpayers to voluntarily review deduction/exemption claims identified through Information Technology and data analytics.

Official link: https://www.incometaxindia.gov.in/documents/20117/6490657/Initiative-to-encourage-taxpayers-to-voluntarily-review-deduction-exemption-claims-identified-PressRelease-23-12-25.pdf/ed3286e0-19a0-1d5d-66d2-457f8bfabdc1?t=1766728295383

• CBDT guidance note, Updated Return of Income, January 2026 — 48-month updated-return framework.

Official link: https://www.incometaxindia.gov.in/documents/20117/42998/Updated-Return-of-Income_2026-01-21_03-31-05_3f6059_en.pdf/e9e280e6-746e-764a-aced-534fdcd9a048?t=1774348252318&version=1.0

• Form 168 – Annual Information Statement (AIS), notified under Rule 245 of the Income-tax Rules, 2026.

Official link: https://www.incometaxindia.gov.in/documents/d/guest/fn-168

• Income Tax Department “Assessment” guidance page, updated March 2026 — including the statement that search and requisition cases from 1 September 2024 are excluded from reassessment and governed under Chapter XIV-B.

Official link: https://www.incometaxindia.gov.in/w/assessment

• Notification No. 18/2022 dated 29 March 2022 — e-Assessment of Income Escaping Assessment Scheme, 2022.

Official link: https://incometaxindia.gov.in/communications/notification/notification-18-2022.pdf

• Departmental Directory 2026 — noting the release of the Search and Seizure Manual, 2025.

Official link: https://www.incometaxindia.gov.in/documents/d/guest/departmental-directory2026-1