Blocked credit under GST no longer turns only on a plea for seamless credit. It now turns on statutory wording, engineering facts, and legislative willingness to close drafting gaps.

The judgment opened a door, not a gate

Blocked credit under GST is supposed to be a drafting rule, but it often behaves like an economic policy lever. When tax is paid on steel, cement, fit-outs, lifts, HVAC and contractor bills during construction, denial of input tax credit changes project IRRs, rent negotiations, and the tax incidence ultimately borne by occupiers and consumers. That is why Safari Retreats landed with unusual force. What looked like a dispute about one mall in Odisha exposed something larger: GST’s self-assessment architecture had promised a value-added chain, yet section 17 kept drawing politically and fiscally deliberate breaks in that chain. The real significance of Safari lies not in whether one taxpayer ultimately wins, but in what the case revealed about how courts, administrators and the GST Council now think about blocked credit on immovable property.

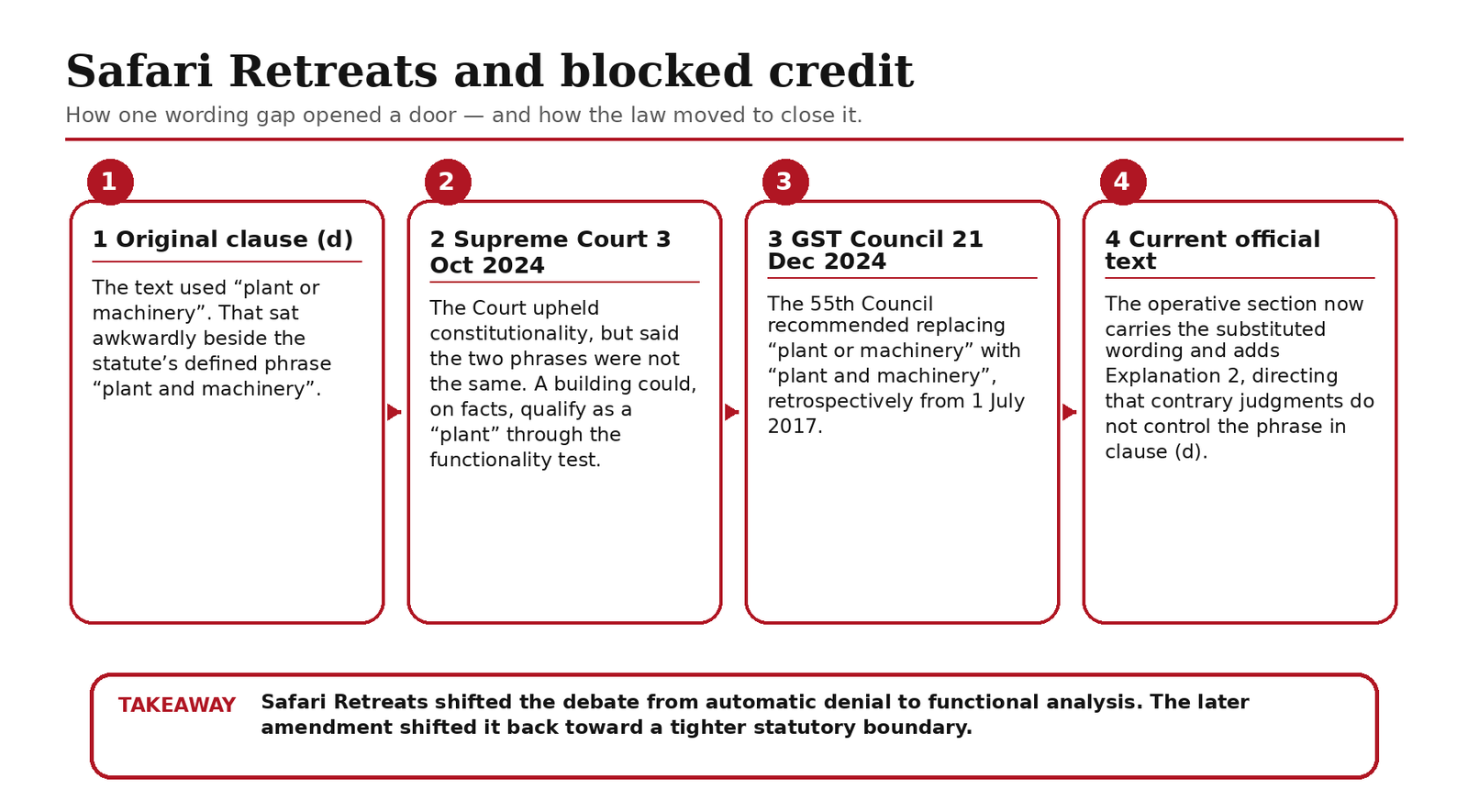

The Orissa High Court had read section 17(5)(d) down because GST was being collected on rental income from the mall while credit on construction inputs was denied. The Supreme Court refused that broader route. In its 3 October 2024 judgment, it upheld the constitutional validity of clauses (c) and (d) of section 17(5) and rejected the argument that courts should rescue the credit chain by rewriting the provision. That part matters. The Court signalled that seamless credit remains a statutory design choice, not a free-standing constitutional entitlement. For taxpayers, that sharply reduces the marginal utility of broad equity arguments. If the text blocks credit, the courtroom will usually ask what Parliament wrote, not what an ideal GST should have delivered.

Yet the Court did not hand Revenue a simple win. It noticed that clause (d) used the phrase “plant or machinery”, while the statute’s explanation elsewhere defined “plant and machinery”. That difference became the hinge. The Court held that the two expressions could not automatically mean the same thing and that, in clause (d), the word “plant” had to be tested on function. A mall, warehouse or other building—other than a hotel or cinema theatre—could, on facts, qualify as a plant if the structure was essential to the taxable supply being made from it. That was a narrow opening, but a real one. Safari Retreats briefly shifted the line from a blunt denial rule to a more fact-intensive inquiry about what a building actually does in the business model.

Why the legislature moved fast

The GST Council moved quickly after the ruling. In its 55th meeting press release of 21 December 2024, it recommended replacing “plant or machinery” in section 17(5)(d) with “plant and machinery”, retrospectively from 1 July 2017. The current official CBIC text now reflects that substituted wording and adds Explanation 2, which says any reference in clause (d) to “plant or machinery” shall be read as “plant and machinery”, notwithstanding contrary judgments, with the amendment reflected from 1 October 2025 and deemed back to GST’s start. That legislative response tells you the state read Safari not as a one-off mall dispute but as a revenue-significant drafting asymmetry. Once the judgment turned a conjunction into a gateway, the political economy of blocked credit changed immediately.

That response also clarifies the deeper policy instinct behind section 17(5). The Supreme Court had already said that immovable property forms a distinct class and that the legislature can carve out exceptions to input tax credit in fiscal statutes. The concern is not merely semantic. Construction of land-linked assets sits close to state taxation powers, capitalization rules and the long-standing fear that credit on embedded real-estate costs can blur tax boundaries. The blocked-credit wall survives because the state prefers a hard separation between general business inputs and capitalised immovable property, even where that raises compliance friction and weakens GST’s claim to purity as a value-added tax. Safari exposed the tension. The 2025 fix shows which side Delhi chose when forced to choose.

What stays difficult after the wording fix

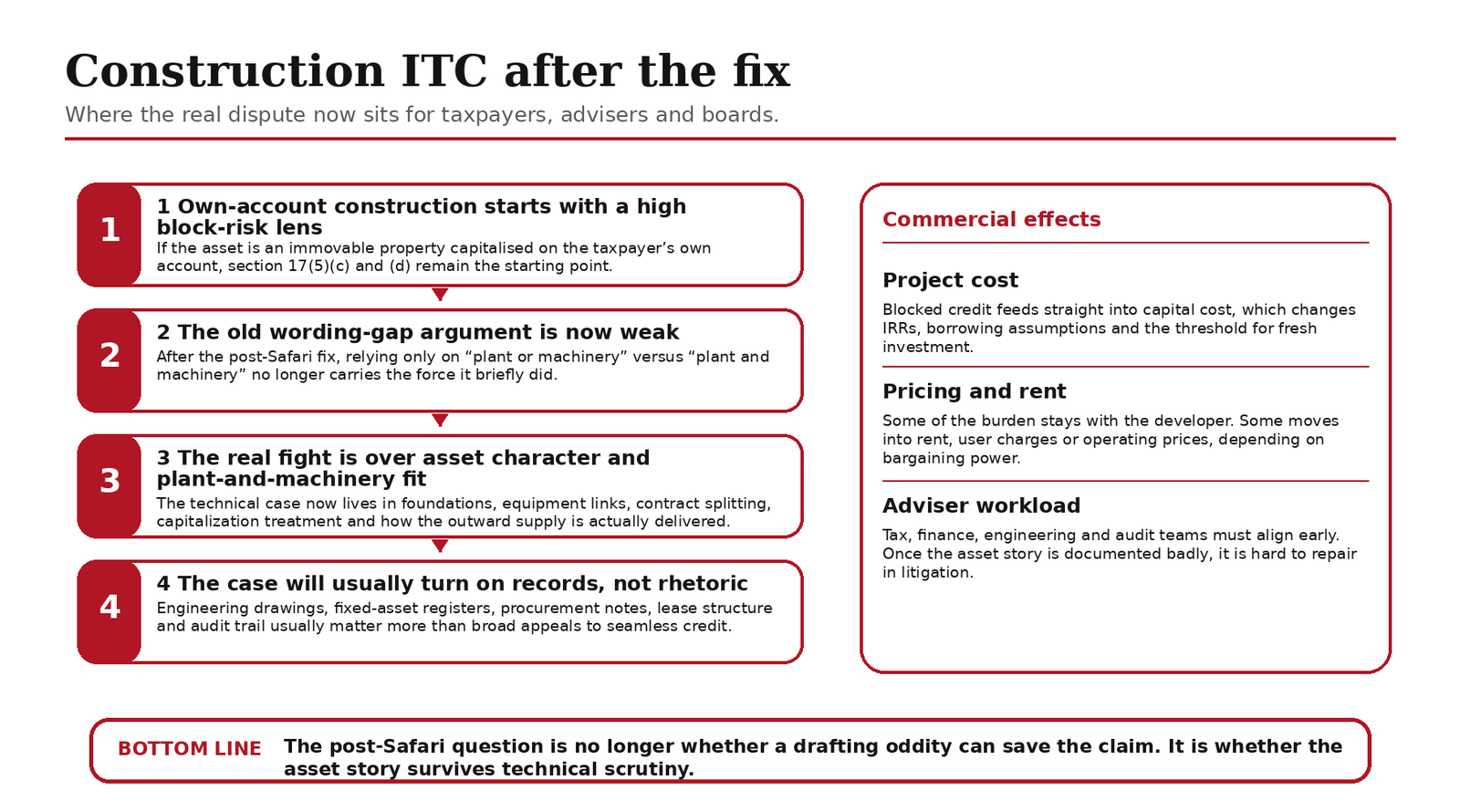

So is the line finally shifting? Yes, but not toward a simple liberalisation of construction ITC. The line is shifting from grammatical litigation to evidentiary litigation. After the 2025 deeming fix, a taxpayer can no longer lean comfortably on the old “or” versus “and” gap. The live questions now sit elsewhere: whether an asset is really civil construction or part of plant and machinery; whether contracts have been bundled or segmented intelligently; whether renovation has been capitalised; whether outward supply character and asset function match the accounting treatment. That pushes the dispute back into engineering drawings, capitalization policies, lease architecture, and fixed-asset registers. For tax professionals, Safari’s practical lesson is brutal: interpretation still matters, but documentation now matters more.

That is especially true for sectors where the built environment is inseparable from the service being sold. Logistics parks, specialised storage, industrial utilities, large-format retail, healthcare infrastructure, and digital infrastructure projects may all argue that structure and function cannot be separated with a straight face. But after the wording correction, those arguments must be grounded in the statutory definition of plant and machinery and in the factual anatomy of the asset, not in the drafting accident that briefly energised Safari. Ordinary commercial buildings held for rental yield will find that much harder. The compliance burden, then, does not disappear; it migrates. Boards now need tax teams, engineers, procurement heads and statutory auditors to speak the same language at capex stage, because by the time a show-cause notice arrives, the evidentiary record is usually already frozen.

Who ultimately pays for blocked credit

For the corporate sector, that means higher pre-investment diligence and a colder view of litigation as a balance-sheet strategy. When credit is blocked on a capital-heavy project, the tax becomes part of project cost and feeds directly into hurdle rates, rent models, user charges and return expectations. Some of that burden stays with promoters. Some gets passed through, depending on bargaining power and market depth. For the middle class, the effect is indirect but real. It can surface in higher retail rentals, costlier warehousing embedded in consumer prices, steeper private-service tariffs, or slower rollout of urban commercial infrastructure. Blocked credit rarely arrives on an invoice labelled as tax pain. It arrives as pricing, delay, or thinner investment appetite.

That is why Safari Retreats still matters, even after the legislative repair. As an outcome case, its taxpayer upside has been narrowed sharply by the post-judgment amendment. As a principles case, it remains vital. It showed that courts will parse fiscal text with unusual discipline, that tiny drafting departures can alter tax incidence at scale, and that the GST Council will close a gap quickly when revenue risk becomes visible. The evolution of blocked credit, then, is not a march toward generosity. It is a shift toward clearer legislative intent, narrower doctrinal escape routes and tougher factual scrutiny at the edges. The line has moved. But it has moved from ambiguity to managed hardness, not from restriction to openness.

Sources & Data Points

Supreme Court judgment: Chief Commissioner of CGST & Ors. v. Safari Retreats Pvt. Ltd. & Ors., judgment dated 03.10.2024 — Open source

Current statutory text: Section 17, CGST Act, 2017 (official CBIC-hosted active text, including current clause (d), Explanation 2 and amendment footnotes) — Open source

Schedule II: Schedule II, CGST Act, 2017 (official text on renting of immovable property and construction as supply of services) — Open source

GST Council: Press Release of the 55th GST Council Meeting dated 21.12.2024 — Open source

CBIC sectoral FAQ: Sectoral FAQs on GST, CBIC — Open source