Cloud subscriptions were sold as frictionless utilities. Tax law still hears older nouns—copyright, technical service, permanent establishment—and that mismatch is turning ordinary SaaS bills into recurring treaty disputes.

The invoice says subscription. The law hears something else.

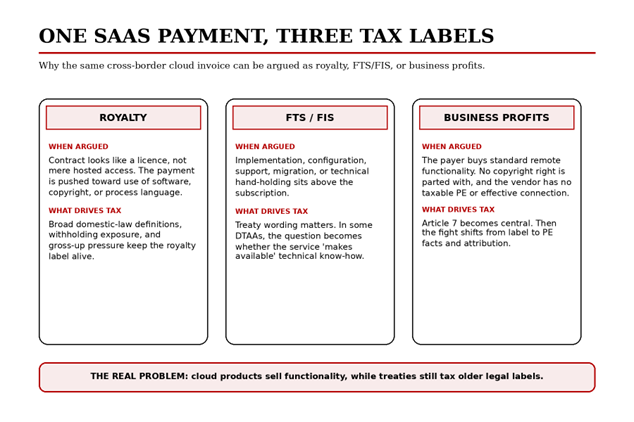

SaaS tax is now less about whether software crosses a border and more about what, exactly, the payer is thought to have bought. An Indian company signs up for cloud accounting, workflow automation, cybersecurity, data analytics, or a vertical compliance stack. Commercially, the deal feels simple: recurring access to remotely hosted functionality. Tax analysis turns it into something else. Is the payer using software in a way that looks like royalty? Is the vendor rendering a technical service that drifts toward fees for technical services, or, under some treaties, fees for included services? Or is this merely ordinary business income that India can tax only if a permanent establishment exists? That gap between commercial reality and tax vocabulary now sits inside procurement, withholding, pricing, and dispute strategy.

Why 2026 sharpens the SaaS tax question

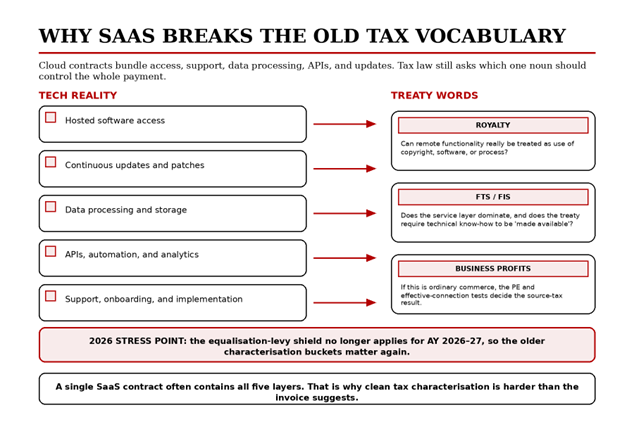

The pressure has increased because the side-routes are narrowing. The Income-tax Act, 2025 came into force on 1 April 2026, and the official transition material makes clear that the rewrite is designed mainly to simplify, consolidate, and renumber rather than rethink the older character buckets. At the same time, the Income Tax Department’s own non-resident benefits compilation records that the section 10(50) exemption for income chargeable to equalisation levy will not apply from assessment year 2026-27. That matters. When the equalisation-levy shelter recedes, cross-border digital receipts are pushed back into the classic treaty buckets with much greater force. Official trade releases place India’s estimated services exports at USD 387.93 billion in April-February 2025-26, up from USD 351.93 billion a year earlier. A larger services economy makes characterisation fights economically larger, not conceptually easier.

Why SaaS tax still gets pulled toward royalty and FTS

Domestic law continues to supply broad hooks. The new Act preserves expansive deeming rules for royalty and fees for technical services. Royalty still reaches payments for rights in software and process language; the definition still says computer software includes a computer programme recorded on any medium and customised electronic data. Fees for technical services remains available as a separate box for managerial, technical, or consultancy services. The law also retains the familiar rule that royalty or FTS effectively connected with a permanent establishment or fixed place in India can shift into business-profits treatment. None of this is accidental. The Indian source-tax architecture was built to catch value before it disappears offshore. But that same architecture encourages category-pushing whenever a cloud contract contains access, support, onboarding, upgrades, analytics, and implementation in one paper bundle.

Treaties narrow the field, but not in a uniform way

The treaty layer is where the clean domestic answer starts to break. In some DTAAs, the service question is tightened by “make available” language. The India-US treaty uses the fees for included services formulation, and the official US technical explanation states that technical or consultancy services must make available technical knowledge, skill, know-how, or processes in specified cases. The India-Singapore treaty also uses a make-available filter for part of Article 12. That narrows source taxation for many SaaS relationships where the customer receives an outcome, not transferrable know-how. Yet treaty protection is not uniform across India’s network. Different wording, different protocols, and different PE facts can produce different answers for contracts that are commercially almost identical.

Where the software royalty precedent helps—and where it stops helping

The Supreme Court’s Engineering Analysis decision remains the most important judicial brake on aggressive software royalty characterisation, and later Supreme Court orders in 2024 and 2025 show that the Court still treats the issue as governed by that precedent. The core lesson was that a payment for use of a copyrighted article is not the same thing as payment for use of copyright itself. That principle still matters in SaaS tax disputes because it restrains the instinct to treat every software-linked payment as royalty. But SaaS is not always a neat descendant of shrink-wrap software or standard distribution contracts. In a pure cloud model, the user may never receive a copy, never control the code, and never obtain reproduction rights. Even so, the contract may include technical support, implementation layers, dashboards, APIs, data processing, or industry-specific configuration. The royalty precedent helps on the copyright side. It does not fully solve the service side.

The taxonomy is breaking because the product is bundled

This is where the older labels begin to look tired. A modern SaaS contract sells functionality, uptime, updates, storage, security, workflow integration, sometimes AI-driven outputs, and often a light consulting layer to make the whole system useful. Tax law, by contrast, still asks whether the payment is mainly for a right, a service, or business income. That worked better when software came in boxes, implementation was separately billed, and infrastructure sat visibly on the customer’s premises. It works less well when the economic substance is a managed digital utility. One invoice can contain a software-access layer that looks non-royalty, an implementation layer that invites an FTS argument, and a platform architecture that raises PE questions at the margins. The result is not just doctrinal untidiness. It is compliance friction embedded in the self-assessment architecture itself.

Who ultimately pays for broken SaaS tax labels

Large corporates feel the first-round impact in withholding disputes, gross-up clauses, deferred procurement, and deal restructuring. The second-round impact is wider. Indian customers often negotiate cloud contracts on a tax-inclusive commercial assumption and discover later that characterisation risk has changed the price. That tax incidence can travel through software spend into audit fees, digital compliance costs, fintech back-office charges, healthcare platforms, logistics tools, and the broader service bills that reach households and small businesses. The middle class is rarely named in treaty litigation, but it still bears part of the cost when business software becomes more expensive to buy, implement, or localise. Tax professionals, meanwhile, are forced into invoice disaggregation exercises that are intellectually neat and commercially artificial.

A better SaaS tax architecture would classify the product before taxing the label

India has a legitimate source-tax interest in a digital economy where value is extracted from its market at scale. The problem is not that the state wants to tax; the problem is that the available nouns are increasingly poor proxies for what cloud businesses actually sell. The cleaner response is not to stretch every subscription toward royalty or FTS by default. It is to develop clearer administrative guidance that separates at least four layers: pure remote access to standard functionality, implementation and migration services, managed or human-assisted service bundles, and contracts that genuinely part with IP rights or embedded know-how. That would reduce opportunistic over-classification without giving up revenue where the facts truly support source taxation.

A better SaaS tax architecture would classify the product before taxing the label

India has a legitimate source-tax interest in a digital economy where value is extracted from its market at scale. The problem is not that the state wants to tax; the problem is that the available nouns are increasingly poor proxies for what cloud businesses actually sell. The cleaner response is not to stretch every subscription toward royalty or FTS by default. It is to develop clearer administrative guidance that separates at least four layers: pure remote access to standard functionality, implementation and migration services, managed or human-assisted service bundles, and contracts that genuinely part with IP rights or embedded know-how. That would reduce opportunistic over-classification without giving up revenue where the facts truly support source taxation.

Until then, disputes will outlive the vocabulary

For now, cross-border SaaS tax in India remains a contest between twentieth-century treaty nouns and twenty-first-century digital products. Domestic law still offers wide entry points. Treaties still narrow them unevenly. Courts still matter, especially where copyright language is stretched beyond its commercial meaning. And the equalisation-levy retreat means the old arguments matter again, not less. The real question, then, is not whether royalty, FTS, or business profits can still classify a SaaS payment. They can, depending on the facts. The harder question is whether a taxonomy built for older forms of software and service delivery can keep producing certainty in a cloud economy. On present evidence, it cannot.

Sources & Data Points

Official and authoritative primary sources used for the article and the data points referenced above.

- Income-tax Act, 2025 as amended by Finance Act, 2026 (official text)

https://www.incometaxindia.gov.in/documents/d/guest/income_tax_act_2025_as_amended_by_fa_act_2026-pdf - CBDT Press Release: Income-tax Act, 2025 comes into force from 1 April 2026

https://www.incometaxindia.gov.in/documents/d/guest/press-release-income-tax-act-2025-comes-into-force-from-01-april-2026-pdf - FAQs on Interplay and Transition under the Income-tax Act, 2025

https://www.incometaxindia.gov.in/documents/81799/11848482/FAQs-on-Interplay-and-Transition.pdf/05f80c1a-073c-a5d7-fb6f-55509242be53?t=1774082865717 - Income Tax Department: Non-resident benefits allowable (updated compilation, 2025)

https://www.incometaxindia.gov.in/documents/20117/42998/Non-resident-Benefits-allowable_2025-12-19_12-46-57_6a9251_en.pdf/71124102-679c-5631-62f4-a40a63a16bbb?t=1774111642847&version=1.0 - Supreme Court order, 20 January 2025, noting the issue is covered by Engineering Analysis Centre of Excellence Pvt. Ltd. v. CIT

https://www.sci.gov.in/sci-get-pdf/?diary_no=490142024&from=latest_judgements_order&order_date=2025-01-20&type=o - Supreme Court order, 20 September 2024, noting Engineering Analysis has been sustained in review

https://api.sci.gov.in/supremecourt/2024/25862/25862_2024_9_13_55874_Order_20-Sep-2024.pdf - India–US Double Taxation Convention (IRS-hosted official text)

https://www.irs.gov/pub/irs-trty/india.pdf - Technical Explanation to the India–US Convention (IRS official)

https://www.irs.gov/pub/irs-trty/inditech.pdf - Protocol amending the Singapore–India DTAA (IRAS official text)

https://www.iras.gov.sg/docs/default-source/archive/protocol-amending-singapore-india-dta%28ratified%29%2812-aug-2011%29.pdf?sfvrsn=9f5e0a70_0 - OECD Model Tax Convention on Income and on Capital: Condensed Version 2017

https://www.oecd.org/content/dam/oecd/en/publications/reports/2017/12/model-tax-convention-on-income-and-on-capital-condensed-version-2017_g1g8769b/mtc_cond-2017-en.pdf - PIB Press Release: India’s overall exports and services-export estimates, 16 March 2026

https://www.pib.gov.in/PressReleasePage.aspx?PRID=2240674®=3&lang=2 - Department of Economic Affairs: Monthly Economic Review, March 2026

https://dea.gov.in/files/monthly_economic_report_documents/File_MER%20March%202026%20%281%29.pdf