Intra-group services disputes in India now turn less on whether services exist and more on whether taxpayers can prove, line by line, why a group charge deserved to survive audit.

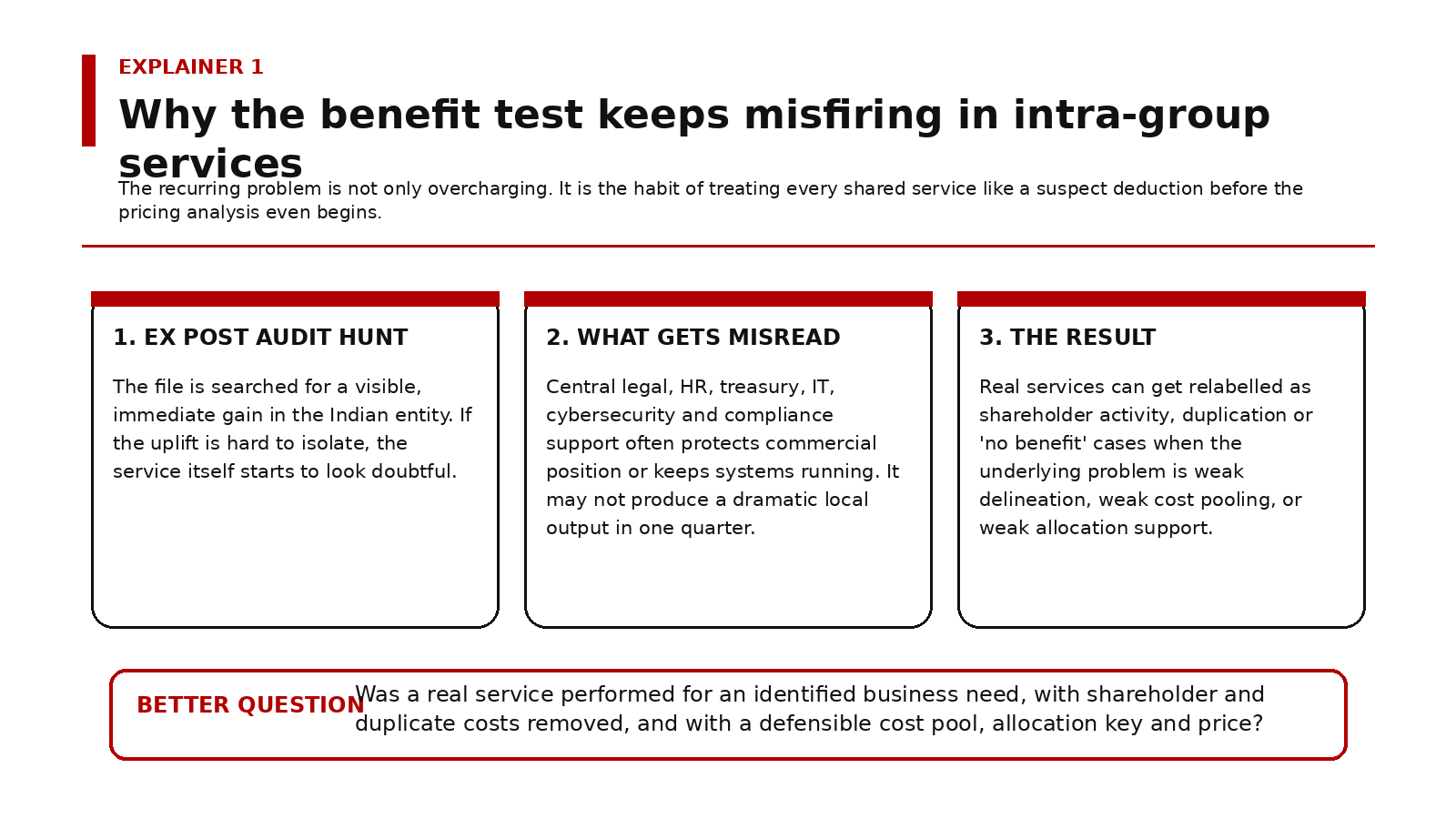

Intra-group services are where multinational groups often meet India’s most suspicious transfer pricing instinct. The charge may be ordinary enough: shared legal support, regional treasury oversight, cybersecurity monitoring, procurement coordination, compliance design, central HR platforms. Yet the audit battle quickly stops being about pricing and starts becoming a trial of legitimacy. Was there any benefit at all? Can the Indian entity show a direct output? Where is the email, the deck, the timesheet, the meeting note, the local profit uplift? That line of questioning is not irrational. India has seen decades of management-fee inflation and loose group allocations. But the marginal utility of turning every service case into a binary benefit test is now falling fast.

That is because the benefit test, used badly, confuses two different jobs. One job is to identify whether a service was actually rendered and whether it served the recipient’s business. The other is to price that service at arm’s length. India’s statute already frames transfer pricing through the arm’s length price and the most appropriate method, not through a standalone anti-deduction veto on vaguely defined “benefit”. When officers collapse delineation, evidentiary sufficiency and pricing into a single sceptical question, the result is rough justice. Charges get attacked not because the economics fail, but because the record does. In a self-assessment architecture that is supposed to reward disclosure, that drift matters.

The deepest flaw is the ex post mindset. Group services are often preventative, enabling or infrastructural. A cyber-monitoring protocol does not prove itself by producing revenue in quarter three. A global sanctions-screening control does not become useless because no violation occurred. A treasury policy may reduce downside volatility rather than lift reported margins. In real business, many central services protect commercial position rather than visibly expand it. That is why the OECD’s service guidance asks a simpler question: would an independent enterprise in comparable circumstances have been willing to pay for the activity, or perform it in-house? India’s disputes too often ask a harsher and less disciplined one: can the taxpayer demonstrate a neat local payoff after the fact?

Why the current lens on intra-group services misfires

The irony is that Indian practice already contains the building blocks of a better system. The Income Tax Department’s transfer pricing framework continues to run through the most appropriate method. Its safe-harbour architecture recognises receipt of low value-adding intra-group services, but only within a narrow corridor: a mark-up not exceeding 5 per cent, an aggregate value ceiling of Rs 10 crore, and accountant-certified cost pooling and allocation keys. That is useful, but small. It helps routine support functions at the edge. It does not solve the bigger terrain of regional management, digital systems, compliance infrastructure or specialised technical support, where the real disputes sit. So the audit habit survives: deny first, classify later.

The 2025-26 policy backdrop makes that habit look increasingly costly. India’s new Income-tax Act, 2025 came into force on 1 April 2026, but the transfer pricing architecture has largely been carried forward in renumbered form, with the transition FAQs explicitly preserving continuity where corresponding provisions exist. At the same time, the Finance Bill, 2026 memorandum had to step in and widen the machinery for giving effect to APAs so that an associated enterprise whose income changes because of an APA can also file or modify its return and claim refund where necessary. That is not a symbolic tweak. It reflects an official recognition that cross-border pricing disputes require workable implementation channels, not just high-principle doctrine.

The current certainty data tells the same story. In India’s latest OECD-reported APA statistics for the 2024 reporting period, 91 APA applications were filed, 65 were granted, the closing inventory stood at 353, and the average time taken to grant APAs was 58.90 months. For attribution and allocation MAP cases, which capture the transfer pricing end of treaty disputes, bilateral closures still took more than 52 months on average. Those are not signs of a jurisdiction that can afford imprecise first-instance disputes on ordinary services. When controversy takes years to unwind, compliance friction becomes part of tax incidence. Corporates build larger buffers. Tax professionals spend more time assembling evidence packs than analysing value creation. And the middle class pays indirectly through slower investment, pricier imported capability and more cautious hiring.

What a better intra-group services test would look like

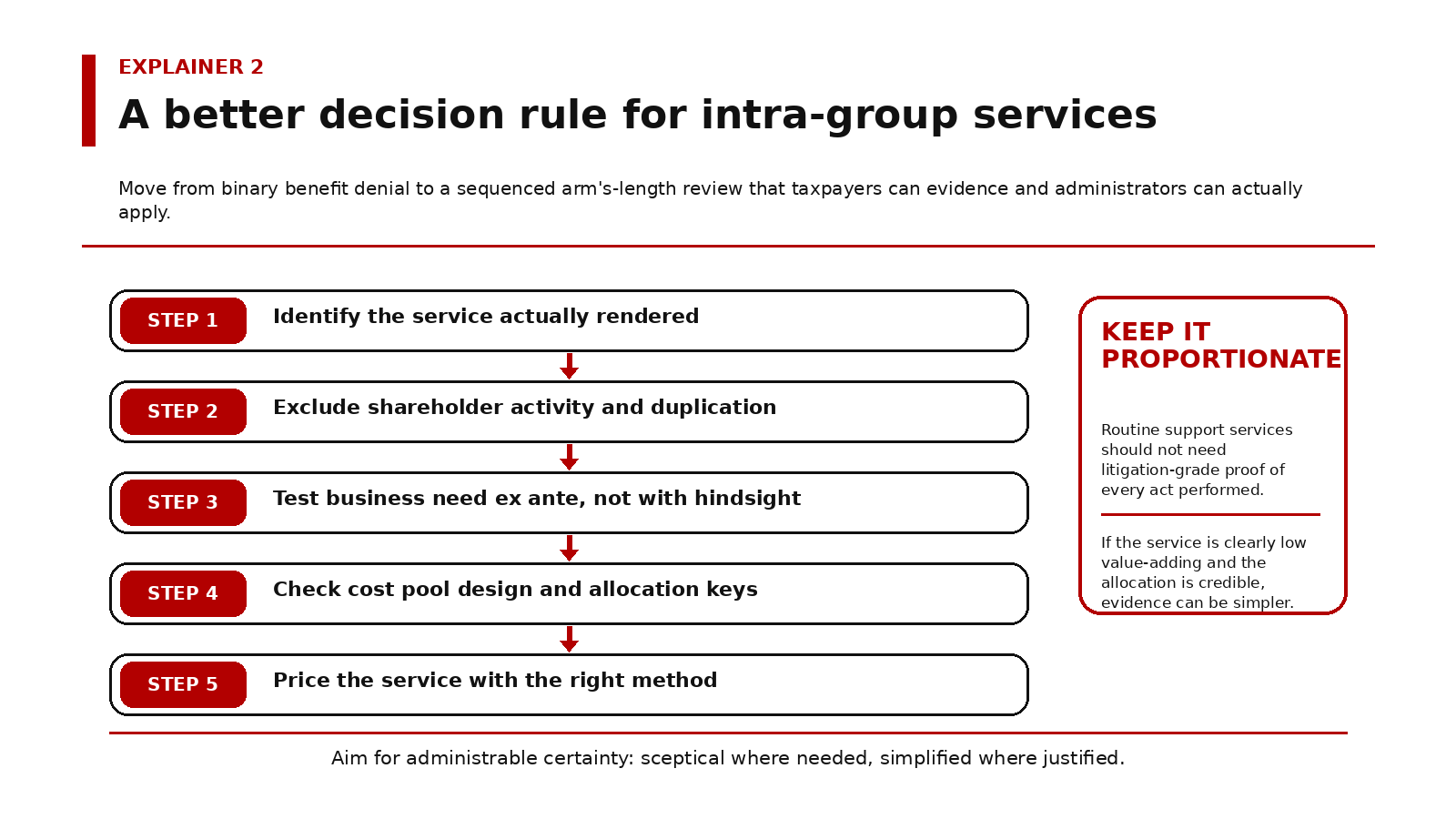

A better Indian test would not abandon scepticism. It would sequence it. Start by accurately delineating the service: what was done, by whom, for which recipient, and under what commercial need? Then strip out what clearly should not be charged: shareholder activity, duplication and stewardship that protects the parent’s investment rather than the subsidiary’s business. After that, examine whether the recipient had an ex ante business reason to obtain the service, including risk control, regulatory compliance, system resilience or access to capabilities it would otherwise have to build. Only then should pricing begin: cost base, cost pool composition, allocation key, mark-up and method. That sequence is more demanding intellectually, but fairer administratively.

It would also allow proportionality. Low-value support services should not require litigation-grade proof of every act performed. Where the service category is plainly supportive, the allocation key is reasonable, shareholder and duplicate costs are filtered out, and the charge sits within a modest mark-up range, the burden of proof should ease rather than intensify. India does not need to import every OECD simplification wholesale. But it should move beyond the ritual of asking for dramatic evidence of benefit from services whose whole point is to keep the business functioning smoothly. The right target is not leniency. It is administrable arm’s-length review. That would improve voluntary compliance more than another cycle of broad-brush disallowance ever will.

Intra-group services will remain contested because the line between real support and disguised profit shifting is genuinely difficult. But India’s next gain will not come from treating every management fee like presumptive erosion. It will come from drawing cleaner distinctions, rewarding contemporaneous documentation, widening practical certainty routes and reserving denial for cases where the service is fictitious, duplicative or badly priced. That is a more serious test than obsession with “benefit”. It is also better economics. A tax system chasing tax buoyancy should want more than aggressive adjustments; it should want rules that strong taxpayers can follow, weak cases cannot game, and honest administrators can apply without turning every shared service into a five-year war.

Sources & Data Points

1.Income Tax Department, Transfer Pricing page – Used for the current official framework on the Most Appropriate Method, safe harbour coverage for low value-adding intra-group services, documentation expectations, and APA mechanics. https://www.incometaxindia.gov.in/transfer-pricing

- Income-tax Act, 2025 [30 of 2025], as amended by Finance Act, 2026 – Used for commencement from 1 April 2026 and continuity of the transfer pricing architecture in the new Act. https://www.incometaxindia.gov.in/documents/d/guest/income_tax_act_2025_as_amended_by_fa_act_2026-pdf

- CBDT, FAQs on Interplay and Transition from the Income-tax Act, 1961 to the Income-tax Act, 2025 – Used for the transition position that earlier provisions, proceedings and mapped options continue where corresponding provisions exist. https://www.incometaxindia.gov.in/documents/81799/11848482/FAQs-on-Interplay-and-Transition.pdf/05f80c1a-073c-a5d7-fb6f-55509242be53?t=1774082865717

- Memorandum Explaining the Provisions in the Finance Bill, 2026 – Used for the 2026 amendment proposal on section 169 so that an associated enterprise affected by an APA can also file or modify a return and claim refund where applicable. https://www.indiabudget.gov.in/doc/memo.pdf

- OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations, 2022 – Used for the benefit test, the treatment of low value-adding intra-group services, the simplified approach, and the 5 per cent mark-up benchmark under that simplified route. https://www.oecd.org/content/dam/oecd/en/publications/reports/2022/01/oecd-transfer-pricing-guidelines-for-multinational-enterprises-and-tax-administrations-2022_57104b3a/0e655865-en.pdf

- OECD, Mutual Agreement Procedure Statistics per jurisdiction – India (2024 reporting period) – Used for India APA and MAP statistics, including filings, grants, closing inventory, average APA grant time and treaty-dispute timelines. https://www.oecd.org/content/dam/oecd/en/topics/policy-issue-focus/map-statistics/map-statistics-india.pdf

7. OECD, Transfer Pricing Country Profile – India – Used to cross-check the absence of specific domestic guidance on intra-group services and the recognition of a simplified route for low value-adding services. https://www.oecd.org/content/dam/oecd/en/topics/policy-sub-issues/transfer-pricing/transfer-pricing-country-profile-india.pdf