India sells more back-office, technology and advisory capacity to the world than ever, yet one classification dispute can still turn a clean export story into a domestic tax bill.

The export boom, the tax trap

Intermediary services under GST have become one of the sharpest legal fault lines in India’s services economy. That would matter less if services exports were peripheral. They are not. The Department of Commerce’s January 2026 release put India’s estimated services exports at US$43.90 billion for that month and US$354.13 billion for April-January 2025-26, with a services trade surplus of US$180.58 billion. Official budget communication in March 2026 also described software services as the anchor and business and consulting services as key growth drivers. When an economy at this scale keeps arguing over whether a back-office contract is an export or an “intermediary” arrangement, the dispute stops being technical. It starts shaping working capital, pricing power and the credibility of India’s cross-border services proposition.

The trouble lies in the statutory design. Section 2(6) of the IGST Act treats a service as an export only if, among other conditions, the place of supply is outside India. Section 13(2) supplies the default rule: if the recipient is outside India, the place of supply is ordinarily the recipient’s location. But section 13(8)(b) carves out intermediary services and deems the place of supply to be the supplier’s location. That is the hinge. The same Indian entity can look like a zero-rated exporter under one reading and a domestic taxpayer under another. Refund eligibility follows that classification. So does the cash-flow profile of the contract.

Why back-office contracts sit on the fault line

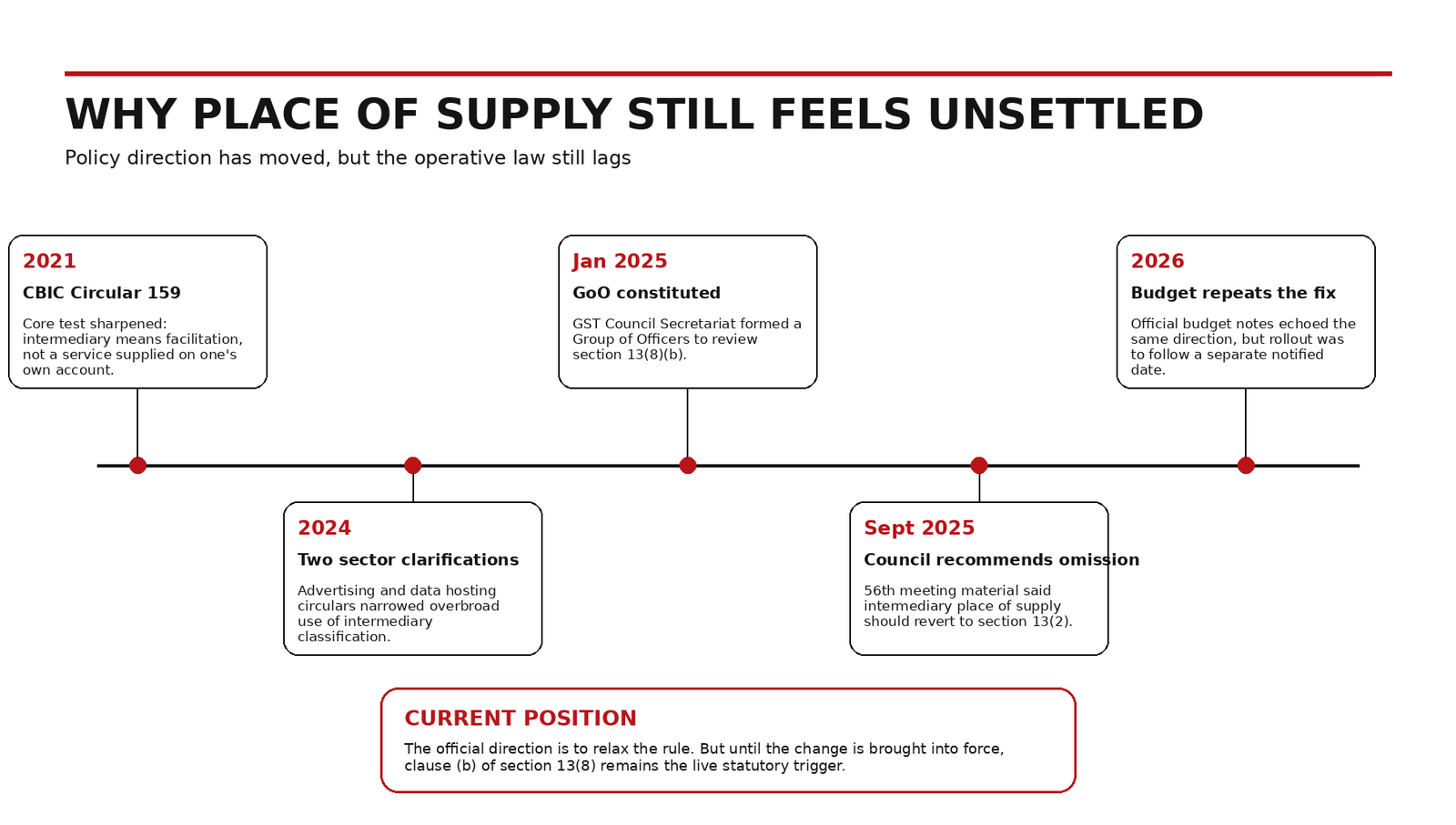

CBIC’s 2021 circular tried to impose discipline on the debate, and its core insight still holds. Intermediary status is not triggered because an Indian supplier sits somewhere in the commercial chain. It turns on whether the supplier is arranging or facilitating a main supply between two or more persons, rather than supplying on its own account. That sounds neat on paper. In practice, modern back-office arrangements blur the line. They mix process management, vendor coordination, analytics, technology layers and client reporting into one commercial package. Labels mislead; substance has to do the work.

That is where recurring place-of-supply disputes begin. A large slice of India’s back-office economy exists to make somebody else’s business run better. Field officers often read that functional proximity as facilitation. Taxpayers read the same contract as a principal-to-principal outsourcing of a defined service. The more the Indian entity interacts with overseas client systems, Indian vendors, media owners, cloud infrastructure or customer touchpoints, the easier it becomes for the classification fight to spill into parallel arguments over recipient, performance-based supply, goods made available, or services linked to immovable property.

The department has narrowed the line, not settled it

The department’s own 2024 clarifications are revealing because they show how unstable the older line had become. In Circular No. 230/24/2024-GST, CBIC clarified that an Indian advertising company providing a comprehensive advertising solution to a foreign client is not, on those facts, an intermediary merely because it also deals with Indian media owners. The Board treated the arrangement as two principal-to-principal supplies and said the place of supply could not be pushed into section 13(8)(b). In Circular No. 232/26/2024-GST, CBIC said an Indian data hosting provider serving an overseas cloud computing company is not an intermediary where it provides the service on its own account, does not deal with end users, and does not fall under the ‘goods made available’ or immovable-property rules. In those cases, the Board said the analysis returns to section 13(2). That is more than sectoral housekeeping. It is an administrative admission that high-value service contracts had been over-read through the intermediary lens.

Yet the instability has not disappeared. It has moved from principle to boundary-drawing. Circulars help where facts resemble the examples; they do not eliminate judgment calls in live assessments, audits and refund scrutiny. The GST Council’s own material for the 47th meeting acknowledged that disputes over intermediary services were leading to rejection of refund claims and demand notices. That acknowledgement matters. It shows that the system was dealing not with a few stray errors but with built-in compliance friction.

2025-26: policy shifted before the law did

The clearest sign of policy discomfort came in 2025. An Office Memorandum dated 30 January 2025 recorded the constitution of a Group of Officers to review section 13(8)(b) after discussion in the 55th GST Council meeting. By September 2025, the Council’s published recommendations had moved beyond review and recommended omission of clause (b) of section 13(8), so that place of supply for intermediary services would revert to the default rule in section 13(2). The 2026 Budget documents repeated that direction. But the same official material also said the change would take effect from a date to be notified in coordination with States. As of 13 April 2026, the active text of section 13 on the CBIC tax information portal still carries clause (b). That gap between policy direction and operative law is the current instability in one sentence.

What the instability really costs

For companies, the second-order effects are immediate. When an export position collapses into a domestic supply position, the damage is not confined to headline tax incidence. Refund claims weaken, input tax credit monetisation slows, pricing assumptions embedded in cross-border service agreements get tested, and treasury teams inherit a working-capital problem that began as a drafting problem. Mid-sized back-office and KPO players feel this most acutely because they cannot absorb prolonged refund friction as easily as global majors can. For professionals, the burden has shifted from arguing broad doctrine to building evidence packs: scope matrices, liability maps, pricing logic and proof that the Indian supplier is not merely connecting two others. For the urban middle class, the effect is indirect but real. Compliance drag in export-oriented services usually appears not as a visible tax line, but as thinner margins, slower hiring and more cautious expansion by firms that employ skilled white-collar labour.

That is why the real issue is not whether every back-office contract should qualify as export. It should not. Some arrangements are genuinely facilitative and should be taxed that way. The issue is whether the current design gives businesses and officers a stable way to distinguish facilitation from substantive service delivery. Right now, it often does not. The best contracts define deliverables, commercial risk, performance responsibility, consideration mechanics and the absence of authority to bind the overseas client with far more precision than many businesses are used to. Tax has forced operational drafting discipline onto commercial teams.

Until notification, the old rule still rules

Intermediary services under GST will remain contentious until law, administration and contract design stop pointing in different directions. The state has already signalled where it wants to go. The 2024 circulars narrowed the misclassification zone; the 2025 Council process acknowledged the design flaw; the 2026 Budget echoed the fix. But until the statutory change is actually brought into force, exporters still live under the old deeming rule and its litigation tail. For India’s back-office and business-services exporters, place of supply remains unstable not because the economy lacks substance, but because the law still hesitates to recognise where substantive service ends and facilitation begins.

Sources & Data Points

- Integrated Goods and Services Tax Act, 2017 – Section 2 (export of services, intermediary definition) – https://taxinformation.cbic.gov.in/content/html/tax_repository/gst/acts/2017_IGST_Act/active/chapteri/section2_v1.00.html

- Integrated Goods and Services Tax Act, 2017 – Section 13 (place of supply where supplier or recipient is outside India) – https://taxinformation.cbic.gov.in/content/html/tax_repository/gst/acts/2017_IGST_Act/active/chapterv/section13_v1.00.html

- Integrated Goods and Services Tax Act, 2017 – Section 16 (zero rated supply) – https://taxinformation.cbic.gov.in/content/html/tax_repository/gst/acts/2017_IGST_Act/active/chaptervii/section16_v1.00.html

- CBIC Circular No. 159/15/2021-GST dated 20.09.2021 – scope of intermediary services – https://cbic-gst.gov.in/pdf/Circular-No-159-14-2021-GST.pdf

- CBIC Circular No. 230/24/2024-GST dated 10.09.2024 – advertising services provided to foreign clients – https://cbic-gst.gov.in/pdf/circular-230.pdf

- CBIC Circular No. 232/26/2024-GST dated 10.09.2024 – place of supply of data hosting services – https://cbic-gst.gov.in/pdf/circular-232.pdf

- GST Council Secretariat Office Memorandum dated 30.01.2025 – constitution of GoO for review of section 13(8)(b) – https://gstcouncil.gov.in/sites/default/files/2025-02/goo_om_dated_30.01.2025_intermediary_service.pdf

- GST Council agenda material for 47th meeting – acknowledgement of disputes, refund rejections and demand notices – https://gstcouncil.gov.in/node/4708

- Recommendations of the 56th GST Council meeting – recommendation to omit section 13(8)(b) – https://gstcouncil.gov.in/sites/default/files/2025-09/press_release_press_information_bureau_0.pdf

- GST Council newsletter, Budget 2026-27 key highlights – change to be brought into effect from a date to be notified – https://gstcouncil.gov.in/sites/default/files/2026-02/newsletter_january_issue_0.pdf

- Union Budget 2026 explanatory notes – omission of clause (b) of section 13(8) proposed – https://www.indiabudget.gov.in/doc/cen/dojstru1.pdf

- Department of Commerce trade release for January 2026 – latest services export and trade surplus numbers used in the article – https://www.commerce.gov.in/wp-content/uploads/2026/02/PIB-Release-4.pdf

- PIB release on India’s services exports and export profile, dated 14.03.2026 – https://www.pib.gov.in/PressReleasePage.aspx?PRID=2240065