Tax certainty in India now turns on the shape of the dispute: domestic or treaty, one-off or recurring, legal or pricing-based. The wrong forum can waste years

Tax certainty India is now a capital-allocation question

Tax certainty India has moved out of the tax department and into the boardroom. Uncertainty now behaves like a hidden financing cost. It distorts provisioning, delays capital allocation and multiplies compliance friction across jurisdictions. India still offers three serious routes for containing that uncertainty – the Board for Advance Rulings, the Mutual Agreement Procedure and the Advance Pricing Agreement programme – but they do not solve the same problem. Choosing badly is no longer a technical error. It is a business error.

The shift in 2025-26 is continuity in law but divergence in administrative depth. The official transition FAQ for the Income-tax Act, 2025 says there is no substantive or procedural change in the advance-ruling framework, while APAs signed under the old Act continue if they are not inconsistent with the new law. The 2025 forms guide also carries forward MAP and APA architecture, including a new form for APA renewal. India has not reinvented certainty routes. It has simply reached a point where one route has become industrial in scale, one remains treaty-driven and useful but slow, and one retains legal relevance without comparable public visibility on throughput.

Board for Advance Rulings still matters, but it is not the old final word

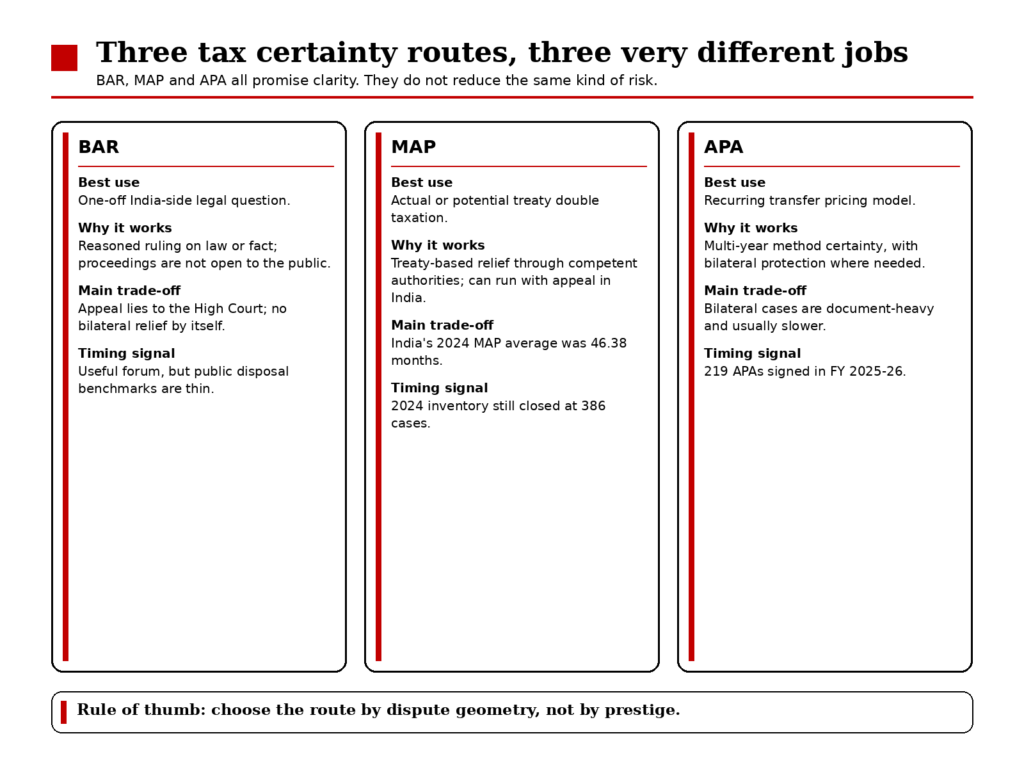

Start with the Board for Advance Rulings, or BAR. The department’s handbook and forms continue to present it as a route for getting a ruling on questions of law or fact relating to proposed or undertaken transactions. Proceedings are expressly not open to the public, hearings can be conducted through video conference, and the 2025 transition FAQ says the framework is materially unchanged. For a taxpayer facing a clean domestic characterization issue – permanent establishment exposure, withholding characterization or a GAAR-entry question – that still matters. BAR is the only one of the three routes designed around a reasoned legal ruling rather than an administrative settlement.

But BAR is no longer the closest thing to a terminal answer. The handbook records a statutory appeal to the High Court within sixty days against a BAR ruling or order. That makes BAR valuable, but not self-sealing. It also does nothing, by itself, to secure correlative relief from the other country in a double-tax case. In practice, BAR is a domestic clarity mechanism. It is strongest where the issue is discrete and India-specific. It is weaker where the real problem is bilateral double taxation or a recurring transfer-pricing methodology. There is also a quieter problem: while the department publishes annual APA reports and OECD-linked MAP statistics, public disposal benchmarking around BAR is much thinner. For boards that care about timeline visibility, that matters.

MAP remains the treaty valve, not a speed tool

MAP is different in kind. The CBDT’s 2022 MAP Guidance describes it as an alternate dispute-resolution mechanism under India’s tax treaties to relieve taxation not in accordance with the DTAA, including double taxation. It can be invoked even where domestic remedies also exist, and India allows taxpayers to pursue appeal and MAP simultaneously, subject to the consequences of later appellate orders. In most Indian treaties, the filing limit is three years from the first notification of the action in question. Once a MAP resolution is reached, the taxpayer has thirty days to accept it and submit evidence of withdrawal of domestic appeals; the Assessing Officer then gets one month to give effect. In design terms, MAP is the treaty system’s pressure valve.

Still, MAP is not the route a corporate should choose because it wants speed. The OECD’s 2024 statistics for India put the average time for all post-2015 MAP cases at 46.38 months. Attribution and allocation cases – the bucket that matters most for transfer pricing – averaged 45.73 months overall, with cases closed in the bilateral stage taking 46.09 months. Other MAP cases averaged 48.07 months overall and 52.38 months at the bilateral stage. The CBDT’s 2024-25 APA annual report shows India’s MAP inventory improving – 421 opening cases in 2024, 96 new invocations, 131 closures and 386 closing cases – but that still does not make MAP quick. It remains the right answer when actual or potential double taxation already exists across treaty partners.

APA has become India’s most institutionalised certainty product

That is where the APA programme has pulled ahead. The CBDT’s annual report for FY 2024-25 says 815 APAs had been entered into by 31 March 2025, giving certainty for more than 4,400 assessment years. It also records more than 2,000 applications over the life of the programme, 174 APAs signed in FY 2024-25, and a record 65 bilateral APAs that year. The PIB release of 31 March 2026 pushes the story further: 219 APAs were signed in FY 2025-26, taking the cumulative total to 1,034, including 284 bilateral APAs. On that test, APA is now the most developed certainty product India offers.

Its strength is not that every case is fast. It is that the taxpayer buys a package: method certainty, multi-year coverage and, in bilateral form, protection against actual or potential double taxation. Indian rules allow an APA period of up to five future years, and rollback can extend certainty to four earlier years. The 2024-25 APA report shows that roughly 40% of UAPAs signed during the year were concluded within two years. It also shows that 71 of the 109 UAPAs signed in FY 2024-25 were renewal cases, and those renewals averaged 35.76 months. Bilateral APAs remain heavier: the same report places the average time to conclude BAPAs in FY 2024-25 at about 50.18 months, and the average for all BAPAs concluded till 31 March 2025 at about 58.90 months. Even so, for a multinational with recurring cross-border transactions, that burden often beats annual transfer-pricing controversy.

What corporates should choose now

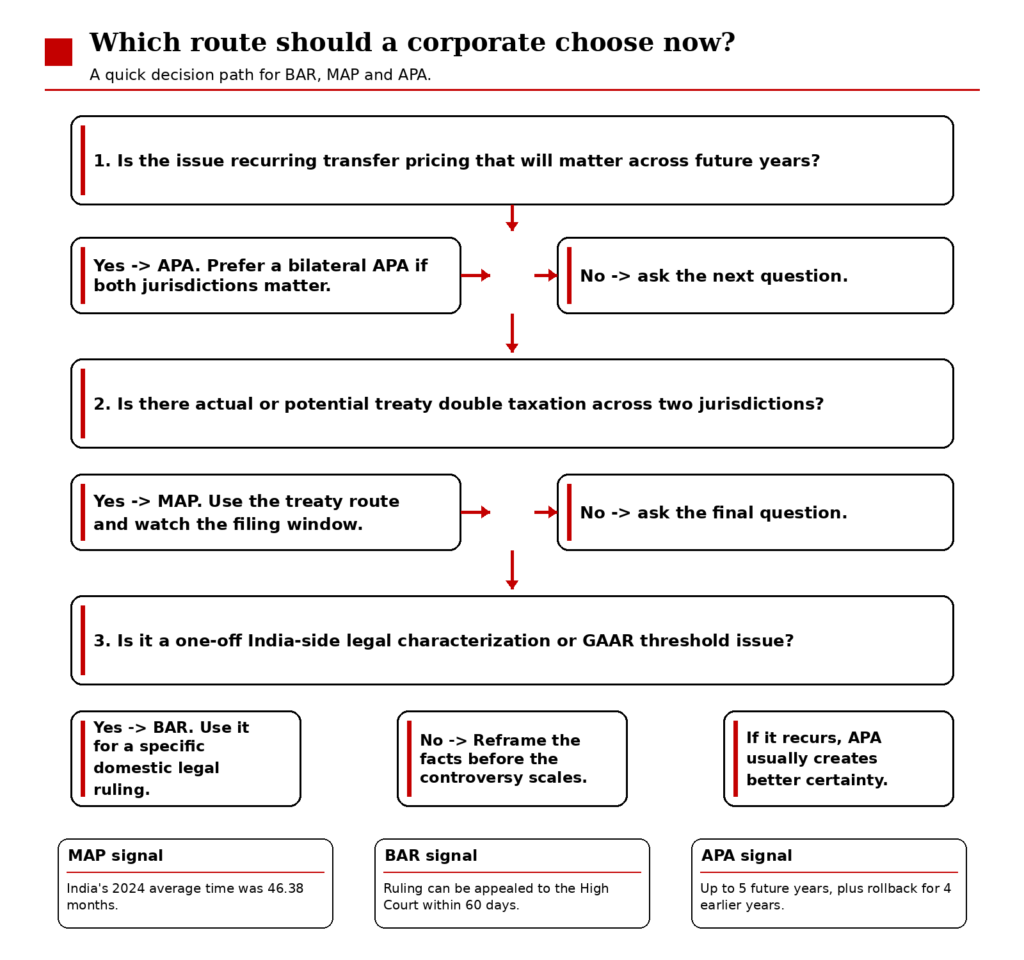

The choice should follow the geometry of the problem. If the issue is transfer pricing and the facts will recur, APA should now be the default instinct, with a bilateral APA preferred where the dispute genuinely spans two jurisdictions. The MAP guidance is explicit that where a bilateral or multilateral APA application on the same issue and years has already been filed and accepted, MAP should not run alongside it; if that APA process fails, MAP can still follow. If the issue is not recurring pricing but an existing treaty double-tax problem, MAP is the natural route because neither BAR nor a unilateral APA can deliver bilateral relief in the same way. And if the issue is a one-off legal characterization question that needs a reasoned India-side answer, BAR still has a place.

The second-order effects are wider than the taxpayer. For tax professionals, the centre of gravity shifts from courtroom advocacy to fact architecture: treaty framing in MAP, comparability design in APA, record discipline in BAR. For the corporate sector, better forum selection lowers tax volatility and trims the risk premium embedded in pricing, supply-chain decisions and internal capital budgeting. For the middle class, the gains are indirect but real. Lower dispute stock and better tax certainty do not create a windfall, but they can reduce the compliance drag and contingency loading that businesses pass through over time. India’s self-assessment architecture works best when disputes enter the right channel early. In 2026, that is the real lesson.

Sources & Data Points

Income Tax Department – Advance Rulings page

Used to confirm the current BAR public-facing framework, handbook access and application materials. https://www.incometaxindia.gov.in/advance-rulings

- Handbook on Advance Rulings (Income Tax Department)

Used for BAR procedure, non-public proceedings, applicant categories and the statutory appeal to the High Court within 60 days. https://www.incometaxindia.gov.in/documents/20117/294610/handbook-advance-rulings.pdf/cf796db7-956f-d230-789c-c7755d37326f?t=1756103887118

- FAQs on Interplay and Transition – Income-tax Act, 2025

Used for the proposition that the advance-ruling framework saw no substantive or procedural change in the 2025 transition, and that existing APAs continue if not inconsistent with the new law. https://www.incometaxindia.gov.in/documents/81799/11848482/FAQs-on-Interplay-and-Transition.pdf/05f80c1a-073c-a5d7-fb6f-55509242be53?t=1774082865717

- Guide to IT Act 2025 forms (Income Tax Department)

Used to confirm continued MAP and APA form architecture in 2025-26, including forms for pre-filing consultation, APA filing, annual compliance reporting and renewal. https://www.incometax.gov.in/iec/foportal/sites/default/files/2026-03/Guide%20to%20IT%20Act%202025%20forms.pdf

- Mutual Agreement Procedure (MAP) Guidance, 2022 (CBDT)

Used for MAP design features: treaty-based relief, ability to invoke MAP even when domestic remedies exist, simultaneous appeal plus MAP, typical three-year filing window, acceptance mechanics and MAP-APA interaction. https://www.incometaxindia.gov.in/documents/20117/43000/mutual-agreement-procedure-map-guidance-2022.pdf/6a391a8f-d528-16a2-6f54-cfc427569e63?download=true&t=1756143974131&version=1.0

- OECD MAP Statistics – India (2024)

Used for India MAP duration benchmarks: 46.38 months average for all post-2015 MAP cases, 45.73 months for attribution/allocation cases and 48.07 months for other cases. https://www.oecd.org/content/dam/oecd/en/topics/policy-issue-focus/map-statistics/map-statistics-india.pdf

- CBDT Annual APA Report for FY 2024-25

Used for APA stock and flow data: 815 cumulative APAs by 31 March 2025, certainty for more than 4,400 assessment years, over 2,000 applications, 174 APAs signed in FY 2024-25, 65 bilateral APAs, MAP inventory data and APA timing metrics. https://www.incometaxindia.gov.in/documents/20117/43010/APA-REPORT-2024-2025.pdf/beea5ac8-ea03-787b-caf8-e76e2f1f9557?t=1763013049210

- PIB press release dated 31 March 2026 on APA outcomes

Used for the latest official data point that 219 APAs were signed in FY 2025-26, taking the cumulative total to 1,034, including 284 bilateral APAs. https://www.pib.gov.in/PressReleasePage.aspx?PRID=2247399&lang=1®=3