GSTAT functioning across India promises faster GST justice, but the real test lies in benches, members, listing discipline and whether digital design can outrun old appellate delay.

GSTAT functioning across India now sits at the sharp end of a question Indian tax policy postponed for too long: when a self-assessment architecture throws up disputes at scale, who absorbs the friction? For eight years, GST improved formalisation, widened the tax base and standardised compliance language, yet its appellate ladder remained lopsided. First appeals moved. The specialised second fact forum did not. That gap turned many disputes into working-capital stress, recovery anxiety and procedural trench warfare rather than a clean argument on tax principle.

From statute to system

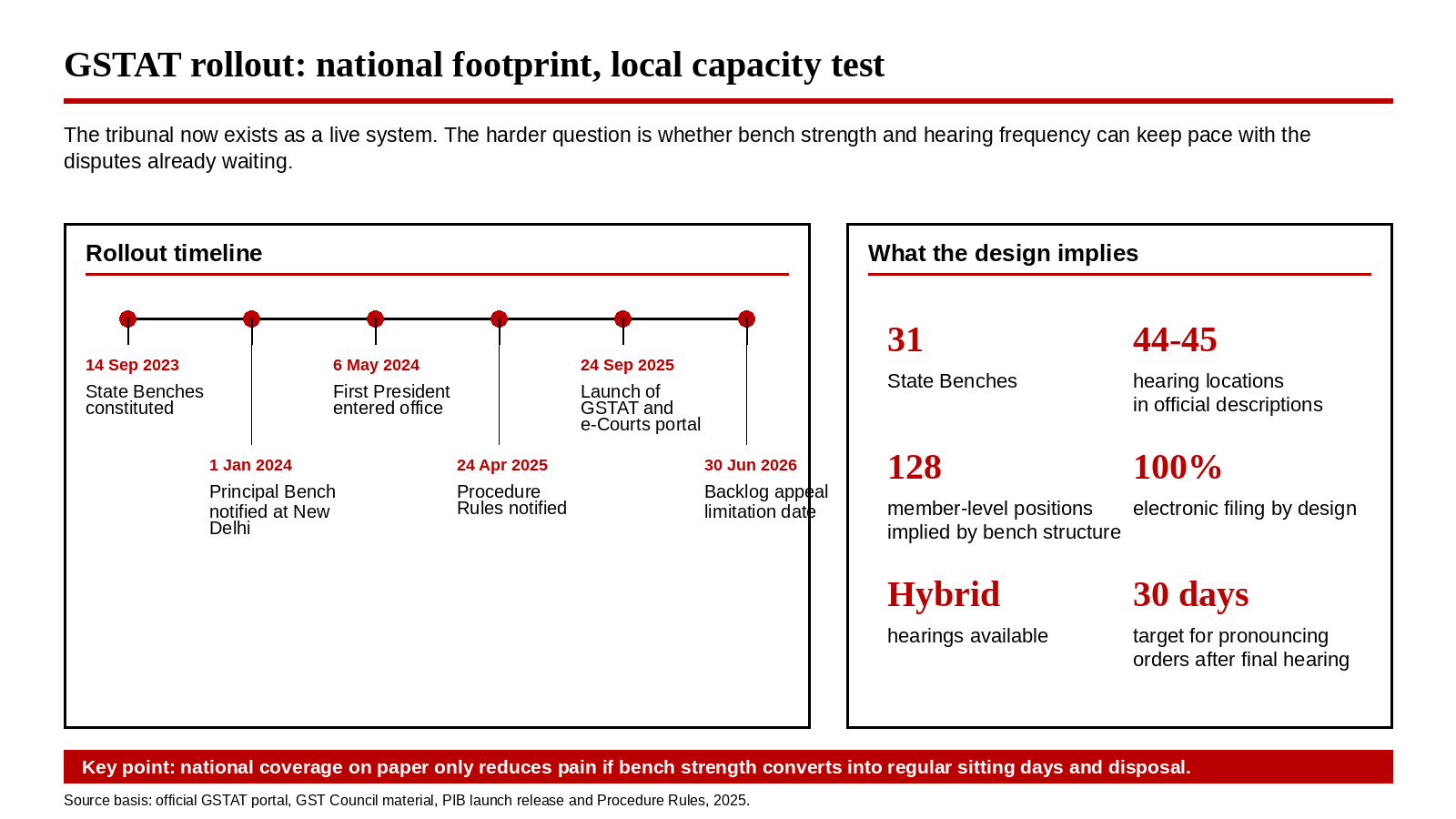

The rollout is no longer theoretical. The Government had already constituted State Benches in September 2023 and notified the Principal Bench at New Delhi from 1 January 2024; Justice (Retd.) Sanjaya Kumar Mishra entered office as GSTAT’s first President on 6 May 2024. The real shift came in 2025. The Procedure Rules issued in April put the tribunal on a digital spine: online institution of appeals, hybrid hearings, electronic records and a rule that orders should ordinarily be pronounced within 30 days of final hearing. When the GST Council met in September 2025, it said GSTAT would begin accepting appeals by the end of that month and start hearings by the end of December. The formal launch followed on 24 September 2025, with the e-Courts portal presented as the operating backbone, not an afterthought.

GSTAT functioning across India isn’t the same as equal capacity

That matters because GSTAT’s design is far larger than the Delhi optics suggest. Official descriptions now point to a Principal Bench, 31 State Benches and sittings across 44 or 45 locations, depending on whether one counts the Principal Bench separately. The same official architecture implies a steep staffing ask: one President, three other members at the Principal Bench and four members at each State Bench. That translates into 128 member-level positions nationwide. India has not built a small appellate chamber; it has attempted a federal litigation grid. The success variable is therefore not notification count. It is whether enough benches sit often enough, with enough registry support, to convert geography into disposal.

Why GSTAT can genuinely reduce litigation pain

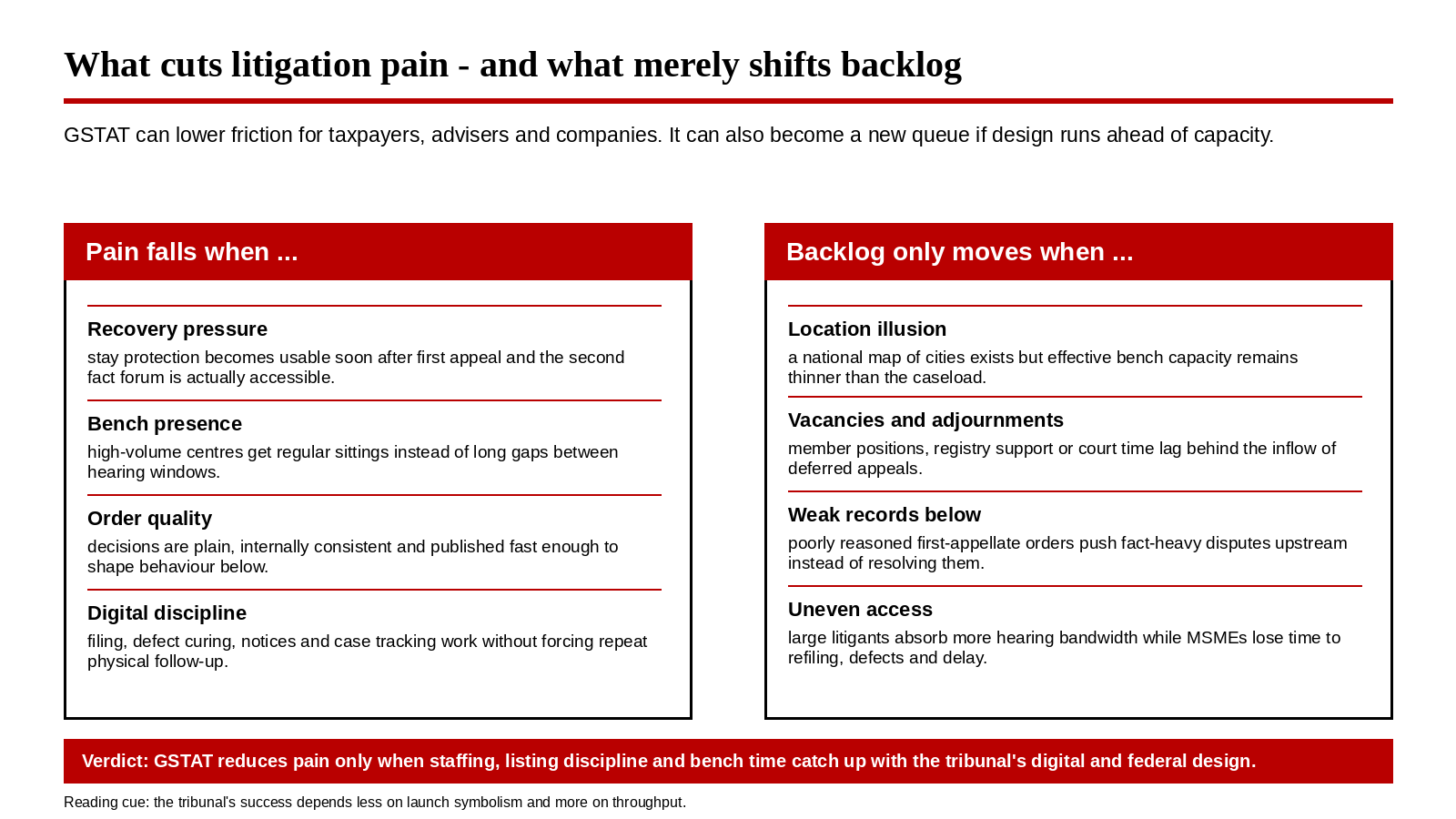

If that grid functions, the gains are real. A live tribunal restores the missing second appeal under section 112 and brings some discipline back into the recovery cycle after first appellate orders. That is not a technical point for lawyers alone. For manufacturers, contractors, exporters and service firms, disputed tax demands tie up cash, distort provisioning and weaken marginal investment decisions. For smaller businesses, the pain is cruder: blocked input credit, bank pressure and a rising compliance bill. A tribunal that hears facts early can stop many cases from reaching High Courts in an inflated, half-developed state.

The digital-by-default model could also compress old frictions. GSTAT’s own portal says all appeals are to be filed electronically, that hearings may be hybrid, and that litigants can track progress online. As of 13 April 2026, the portal displayed 12,680 registered users, 4,923 advocates, 2,892 e-filed appeals and 241 e-filed applications. Those numbers do not prove swift justice. They do show that the pipeline exists and that stakeholders are using it. In a system where tax litigation too often depended on paper movement, physical distance and registry opacity, that alone is a material institutional upgrade.

Why backlog may simply be redistributed

Still, the sceptics have a serious case. Backlog is rarely destroyed by institutional design alone; it is usually redistributed until capacity catches up. The Council itself had to recommend 30 June 2026 as the limitation date for filing backlog appeals. That tells its own story: a large stock of deferred disputes is waiting at the gate. Once those matters begin landing together, tribunalisation may reduce visible pain in one layer while concentrating pressure in another. A portal can smooth filing. It cannot hear arguments. Benches do that.

Backlog at the gate, capacity inside the gate

The second bottleneck is quality below the tribunal. GSTAT can correct first appellate orders, but it cannot cheaply repair an ecosystem where facts were poorly tested, records were thin, and reasoning was formulaic. That has direct consequences for professionals and companies. More appeals are now worth pursuing because the forum exists. But that also means more paper-books, more fact reconstruction, more requests for additional documents, and more contests over stay, condonation and scope. If bench time gets consumed by defective records and serial adjournments, India will not have cured compliance friction. It will have renamed it.

What changes for taxpayers, advisers and corporate India

For the middle class, the tribunal’s effect arrives indirectly but concretely. When working capital is locked in tax disputes, businesses pass some of that cost through prices, slower hiring or postponed projects. Housing, construction, logistics, consumer durables and contract-heavy services all feel that tax incidence in ways that do not show up neatly on an invoice. A cleaner appellate path cannot erase those pressures, but it can reduce the deadweight cost of prolonged uncertainty. The tribunal also matters to salaried households as small proprietors, landlords, professionals and family businesses increasingly fall into GST disputes that are too large to ignore and too technical for ad hoc compromise.

For tax professionals, GSTAT changes the centre of gravity. The winning skill will shift from tactical writ-driven firefighting to disciplined record-building, issue-framing and hearing management. For the corporate sector, the calculus becomes sharper: which cases deserve adjudication, which deserve closure, and which require stronger internal controls so that appeals do not become the default operating model. That is why the Finance Minister’s launch emphasis on plain-language orders, checklists, digital filings and time standards was well judged. GSTAT will reduce litigation pain only if it behaves like an economic institution as much as a judicial one – accessible, predictable and fast enough to matter.

So the honest answer is unsentimental. GSTAT functioning across India should reduce litigation pain, but not because India has finally unveiled a tribunal. It should reduce pain only if bench strength, registry staffing, listing discipline and order quality keep pace with the volume already queued up. The rollout has crossed the threshold from promise to operation. The harder phase begins now. India has built the channel. The question for 2026 is whether it can generate enough throughput to prevent a federal dispute-resolution reform from becoming a more digitised backlog.

Sources & Data Points

Official and authoritative materials used for dates, structure, procedural design, and current operational indicators.

- 53rd GST Council material (background on constitution of benches, President entering office, and section 112 time-limit issues) – https://gstcouncil.gov.in/node/5061

- PIB release dated 6 May 2024 on oath of office to Justice (Retd.) Sanjaya Kumar Mishra as the first President of GSTAT – https://www.pib.gov.in/PressReleseDetailm.aspx?PRID=2019749

- Press Release of the 55th GST Council dated 21 December 2024 (procedural rules and recommended changes relating to appeal pre-deposit and anti-profiteering) – https://cbic-gst.gov.in/pdf/Press-Release%20-55-GST-Council.pdf

- GSTAT Procedure Rules, 2025 notified on 24 April 2025 – https://efiling.gstat.gov.in/downloads/manual/Procedure_Rules.pdf

- Recommendations of the 56th Meeting of the GST Council dated 3 September 2025 (operationalisation timeline and 30 June 2026 backlog-appeal limitation date) – https://gstcouncil.gov.in/sites/default/files/2025-09/press_release_press_information_bureau_0.pdf

- PIB release dated 24 September 2025 on formal launch of GSTAT and unveiling of the GSTAT e-Courts portal – https://www.pib.gov.in/PressReleasePage.aspx?PRID=2170932

- Official GSTAT e-Filing Portal (bench structure, digital-filing model, hybrid hearing description, and portal statistics viewed on 13 April 2026) – https://efiling.gstat.gov.in/mainPage.drt

- Official GSTAT Presidential Order / Advisory / FAQ page (online filing availability at all benches and no offline submission requirement) – https://efiling.gstat.gov.in/presendentialorderscreen.drt

- Official GSTAT Cause List interface (location coverage visible on live cause-list system) – https://e-commcourt.gov.in/gstat/causelist.php

- Official GSTAT Judgement / Orders interface (location coverage visible on live orders system) – https://e-commcourt.gov.in/gstat/judgement.php

- Principal Bench, GSTAT [Antiprofiteering Division] website (live cause lists and final orders visible in April 2026) – https://www.naa.gov.in/