The old offshore script was simple: hold paper, produce a certificate, claim the rate. In 2026, treaty relief turns on who actually controls, keeps, and bears the income.

Beneficial ownership after the paperwork era

Beneficial ownership has become the treaty question that refuses to stay clerical. For years, many cross-border structures treated it as a paperwork exercise: incorporate a holding company in a treaty jurisdiction, obtain residence documentation, route dividends, interest, or royalties through it, and expect the reduced withholding rate to hold. That script now looks dated. In a post-BEPS treaty environment, Indian withholding files are no longer judged only by where the recipient sits on paper. They are judged by whether that recipient has any real command over the income stream, the risks attached to it, and the decisions that shape it.

A narrower test in a broader anti-abuse world

That distinction matters because treaty beneficial ownership was never designed to mean bare legal title. Nor is it the same as the Companies Act or AML-style search for the ultimate human owner. OECD commentary has long treated an agent, nominee, or conduit with a binding pass-through obligation as outside the concept. Just as important, the commentary also warns against the opposite error: beneficial ownership is not a universal anti-abuse weapon that swallows every treaty-shopping dispute. It is a narrower test. It asks whether the immediate recipient has the right to use and enjoy the income without a contractual or legal obligation to hand it on. Broader cases of abuse are meant to be handled by other tools. In 2026, that separation matters more than ever.

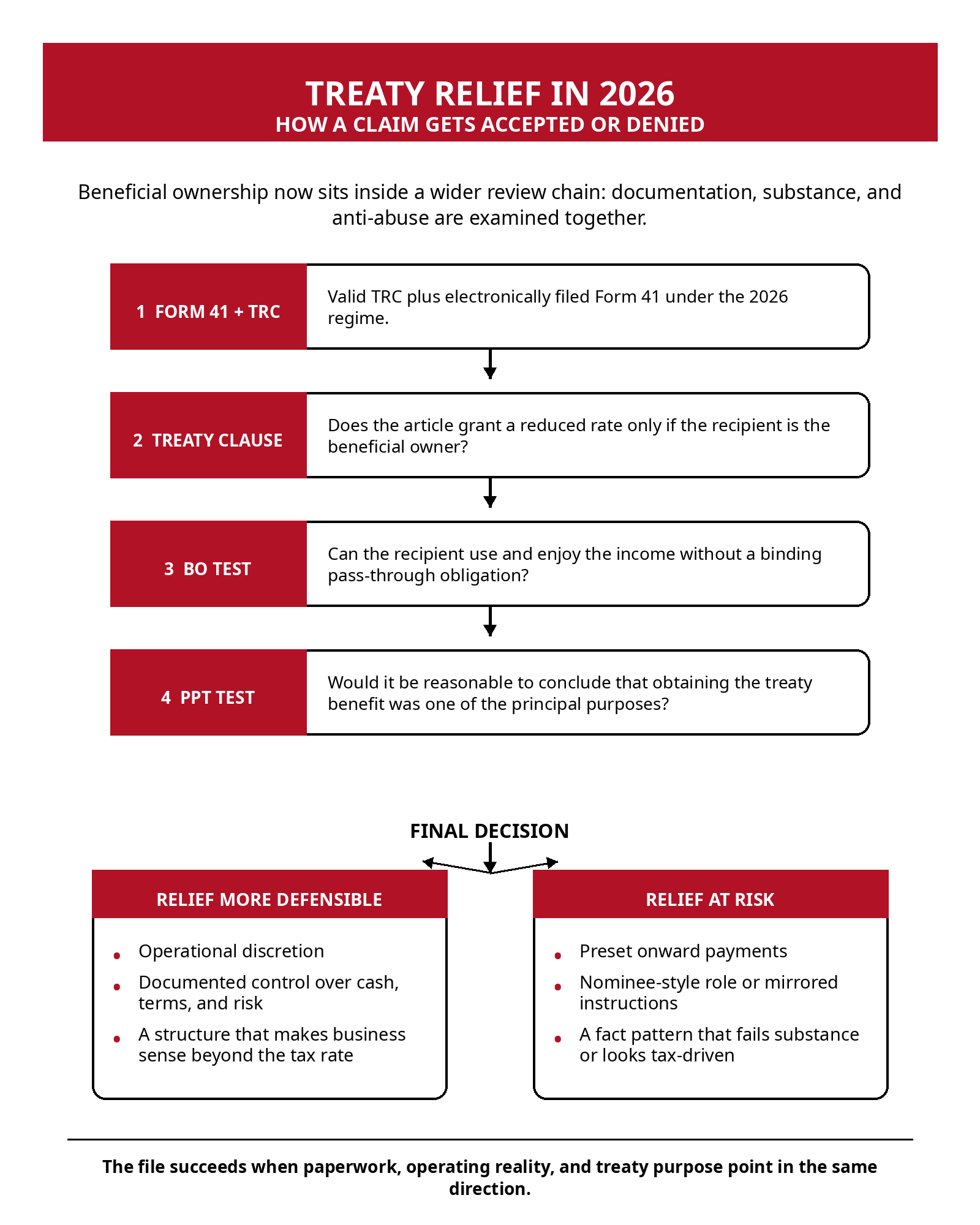

India’s treaty landscape now operates under that layered logic today. The classical dividend, interest, and royalty articles in many treaties still condition reduced source taxation on the recipient being the beneficial owner. But the structure above those clauses has hardened materially. Current synthesised treaty texts posted by the Income Tax Department show the old withholding-rate architecture sitting alongside MLI-inserted anti-abuse language such as the principal purpose test. The OECD’s current MLI materials say the instrument already covers over 100 jurisdictions. In plain English, even a recipient that clears the beneficial ownership hurdle can still lose relief if the arrangement itself looks tax-driven.

The 2026 choke point: evidence, not just forms

The compliance architecture has also tightened at the filing stage. Under the Income-tax Act, 2025 and the Income-tax Rules, 2026, the familiar Form 10F framework has shifted into Form 41 under section 159(8) and rule 75 for non-residents claiming treaty relief. CBDT’s 2026 guidance is explicit: Form 41 is mandatory, it must be filed electronically, it travels with a valid tax residency certificate, and without a valid electronically filed form the DTAA benefit is not available. A departmental note on the form says the average filing count over the last five years is around 23,000. That is a useful signal. Treaty relief remains routine in volume, but it is no longer casual in evidence.

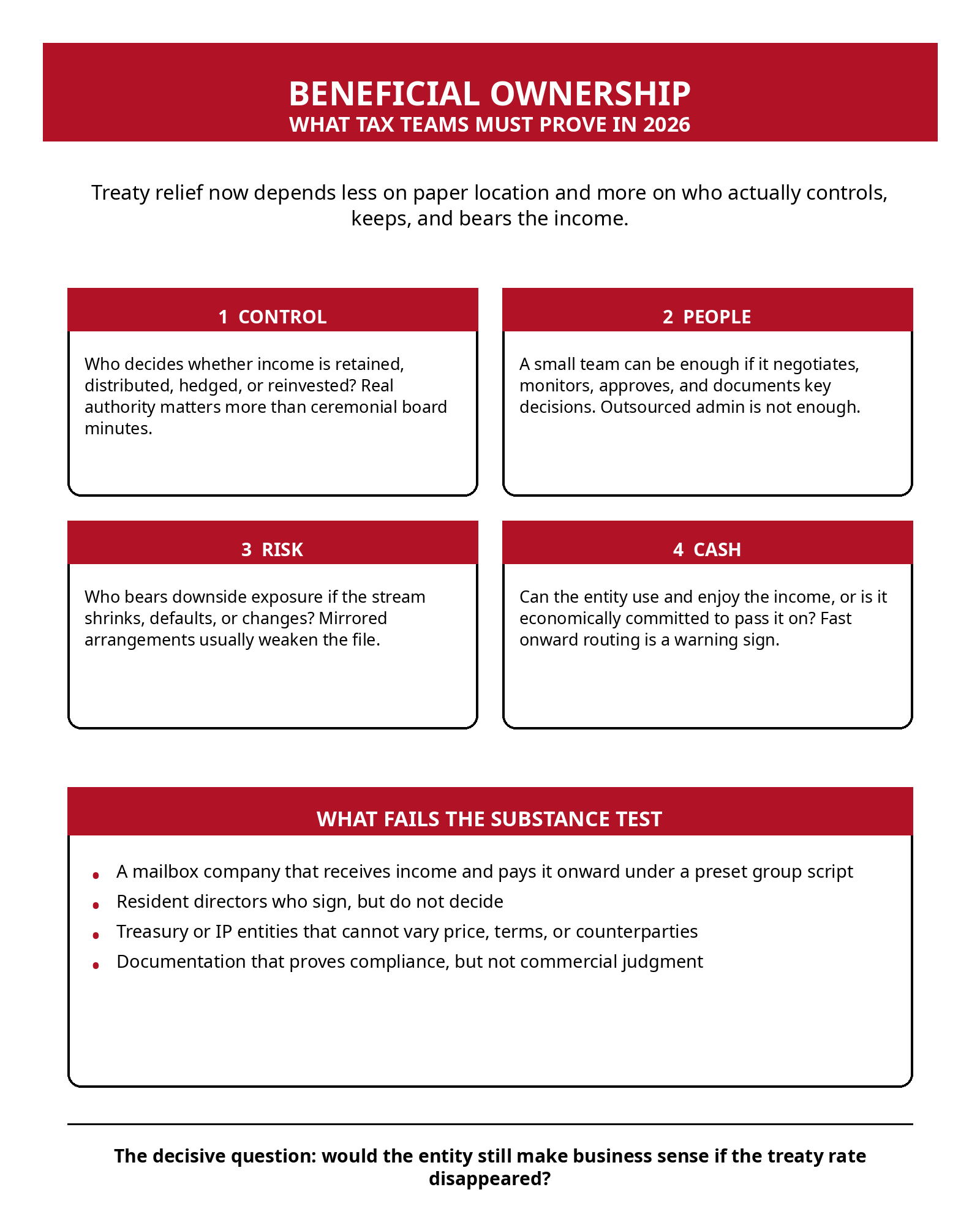

So how much substance is enough? The uncomfortable but honest answer is that there is no statutory headcount, board-meeting quota, or office-size test that settles the issue. Still, the 2026 threshold is not mysterious. A recipient entity starts looking commercially real when it can decide whether to retain or deploy the income, bears at least some economic exposure if the income falls away, and performs functions that are not perfectly mirrored elsewhere in the group. Tax officers and advisers will ask simple questions dressed in technical language: who negotiated the funding or licence terms, who can change them, who controls bank accounts, who evaluates counterparties, who carries downside risk, and who would still exist in a meaningful way if the tax rate were stripped out of the structure.

That is why paper substance now fails faster than it used to. A local address, resident directors, annual board packs, and compliance outsourcing may still be necessary, but they rarely answer the core enquiry. An entity that receives income on Tuesday and is economically committed to paying it onward on Wednesday is still vulnerable, even if its company law housekeeping is immaculate. The same is true of a treasury company that prices nothing, decides nothing, and merely mirrors group instructions, or an IP company that owns contracts but not the commercial strategy around exploitation. Beneficial ownership disputes are increasingly won or lost on operational facts, not on a cabinet full of stamped documents.

What enough substance looks like in practice

The harder cases sit in the middle, especially where groups have genuine regional platforms. A holding company with its own board may still fail if every meaningful capital allocation call is taken elsewhere. By contrast, a recipient with a small team can still be credible if that team actually approves distributions, manages foreign exchange exposure, negotiates third-party debt, monitors licensees, or decides whether to reinvest income. Size matters less than discretion. This is where many taxpayers still overread substance doctrine. They assume the answer lies in creating visible overhead. The better test is whether the entity has enough real authority that a commercially rational group would keep it even if treaty relief became less generous.

That shift carries second-order effects well beyond international tax departments. Indian corporates face more withholding friction, longer onboarding for foreign counterparties, and a stronger need to align legal documentation with treasury, IP, and governance realities. Tax professionals have to build files that read less like form compilations and more like factual narratives of control, people functions, and risk assumption. Even the middle class is not fully insulated. Cross-border capital, technology, and licensing structures absorb compliance cost, and some of that cost eventually shows up in pricing, returns, or the conservatism with which firms invest. None of this means treaty relief is disappearing. It means the access cost has risen.

The 2026 bottom line

The practical lesson for 2026 is not that every intermediate vehicle is doomed. It is that treaty relief now demands a cleaner story. Beneficial ownership still does distinct work: it filters out fiduciary conduits and recipients that never truly own the income in a treaty sense. PPT and related anti-abuse rules do the wider policing. Put together, they push structures toward something many boardrooms once treated as optional—commercial substance that can survive factual scrutiny. In that world, the question is no longer whether there is an entity in the treaty jurisdiction. It is whether that entity can convincingly answer the simplest question in the file: what, exactly, do you do here?

Sources & Data Points

Official and authoritative materials used for the article are listed below.

|

No. |

Source |

Use in article |

|

1 |

Statutory framework for the 2026 income-tax regime and treaty-relief references under section 159. |

|

|

2 |

Prescribed documentation and information for claiming double taxation relief in the new regime. |

|

|

3 |

CBDT guidance on mandatory filing, timing, PAN-optional cases, verification, and the consequence of not filing. |

|

|

4 |

Operational note used for the filing-volume datapoint and document requirements. |

|

|

5 |

Official treaty repository and current treaty-navigation page maintained by the Income Tax Department. |

|

|

6 |

Illustrative current treaty text showing classical beneficial-owner clauses sitting alongside the MLI principal purpose test. |

|

|

7 |

Current OECD overview of the MLI and treaty-abuse architecture. |

|

|

8 |

Commentary used for the treaty meaning of beneficial ownership, including the right-to-use-and-enjoy standard and the distinction from broader anti-abuse analysis. |