AI-generated invoices can look perfect, but scrutiny doesn’t reward polish. It rewards provenance: who created the record, where it lived, what system touched it, and whether the trail still holds.

AI-generated invoices and the law’s starting point

AI-generated invoices are no longer a fringe curiosity in finance departments. They sit inside a wider push toward automation that Indian policy now openly recognises. The IndiaAI Mission carries an outlay of more than ₹10,300 crore, and the Economic Survey 2025-26 notes that the Reserve Bank’s own review found AI adoption in Indian finance has begun, even if it remains concentrated in larger institutions and mostly basic use cases. That is exactly why the evidentiary question matters now. In India’s self-assessment architecture, records are created first and tested later. AI reduces drafting time. It also raises the volume of documents that can be produced with almost no marginal effort. When scrutiny eventually arrives, the question won’t be whether a human typed every line. It will be whether the record can still be tied to a real transaction.

The law’s starting point is not anti-technology. The Bharatiya Sakshya Adhiniyam, 2023 says an electronic or digital record cannot be denied admissibility merely because it is electronic, and gives it the same legal effect as other documents, subject to its admissibility rules. The Information Technology Act, 2000 had already laid that foundation years earlier by recognising electronic records and electronic signatures. It even anticipates automation: section 11 attributes an electronic record to the originator not only when a person sends it personally, but also when an information system programmed by or on behalf of the originator operates automatically. That helps honest automation. It does not confer automatic credibility on every PDF a machine can generate. The legal recognition of electronic records is a threshold benefit. The real contest begins once authorship, authority, timing, integrity or commercial substance are disputed.

Why AI-generated invoices now face a provenance test

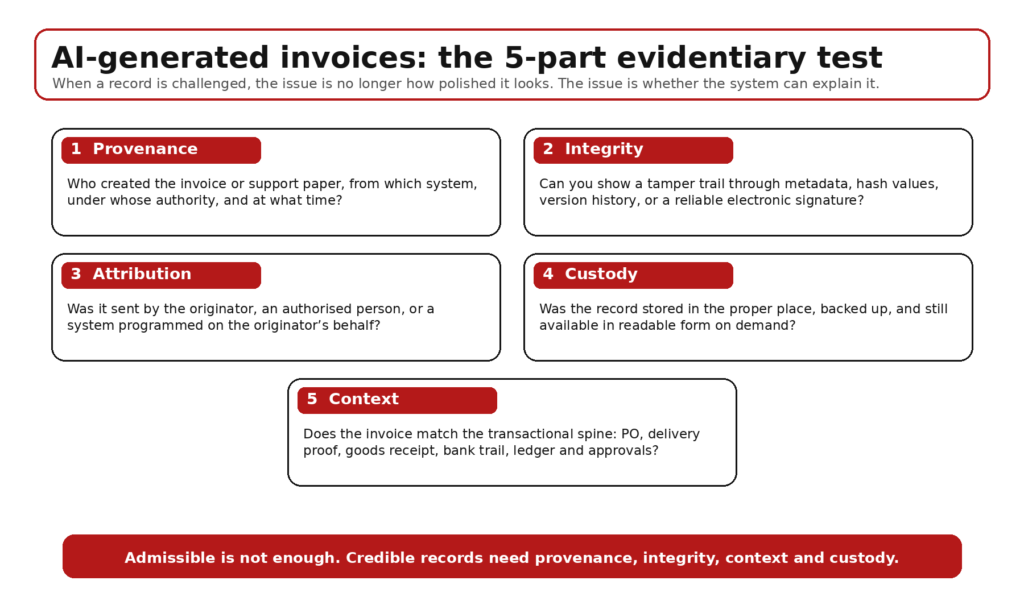

That contest is becoming more demanding, not less. The Bharatiya Sakshya Adhiniyam does something subtle but significant: it shifts attention from the outward appearance of the document to the circumstances of its creation and custody. Its schedule-linked certificate for electronic records asks for the source device or cloud location, lawful control, ordinary-course generation, and the hash value of the electronic record. That is not decorative paperwork. It is a legislative nudge toward forensic discipline. A beautifully drafted AI annexure explaining a transaction may impress a junior team internally. In litigation or hard scrutiny, a rough system export with a clean source trail can be far stronger. India is moving from document-centric proof to system-centric proof, and AI-generated invoices sit squarely inside that shift.

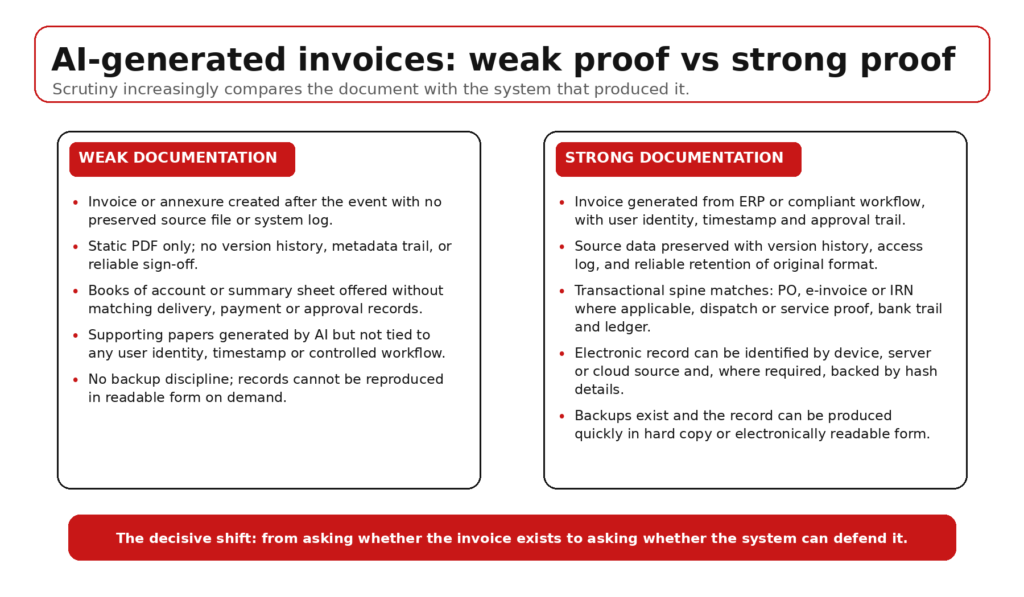

The same logic weakens a common misconception in tax practice: that once an entry appears in books or supporting papers, it has acquired evidentiary heft. The Bharatiya Sakshya Adhiniyam makes entries in books of account, including those maintained electronically, relevant; it also says such entries alone are not sufficient to fasten liability. That matters because AI can cheaply produce the surrounding wrapper of plausibility: narration notes, internal justifications, debtor statements, e-mail summaries, vendor explanations and reconciliation write-ups. The record may look coherent while the transactional spine remains thin. So scrutiny will separate the base event from the explanatory layer. Purchase orders, goods receipts, delivery proofs, bank trails, access logs, approval workflows and system timestamps will matter more than a polished AI memo created after the event to explain why everything supposedly fits.

GST, e-invoicing and the system trail

GST law already points in that direction. Section 35 of the CGST Act permits accounts and records to be kept electronically. The CGST Rules go further. Rule 56 allows digitally maintained records, requires digital authentication, and expects the records and underlying documents to remain accessible. Rule 57 requires proper electronic backups and obliges the registered person to produce, on demand, relevant records in hard copy or electronically readable form, along with file details, passwords and code explanations where necessary. That architecture rewards contemporaneous, system-generated evidence. It punishes reconstruction. GSTN’s March 2025 advisory tightening the 30-day reporting window for e-invoices of taxpayers with annual aggregate turnover of ₹10 crore and above pushes the same discipline. The state is saying, in effect, that records should be born close to the event, not assembled later under pressure.

Still, an IRN is not a universal truth serum. E-invoicing validates structure, format and reporting; it does not, by itself, prove that goods were delivered, services were actually rendered, or valuation is commercially defensible. In other words, e-invoicing is strong compliance infrastructure, not a substitute for substantive evidence. That distinction becomes sharper in an AI environment. A business may have a valid e-invoice, yet generate an AI-written explanation, AI-sorted support schedule, or AI-drafted vendor confirmation that cannot survive challenge because it lacks provenance. For corporate finance teams, the implication is hard but clear: the marginal utility of another drafting tool is now lower than the marginal utility of stronger control architecture. Version history, role-based access, source-data locking, maker-checker workflows, and reliable e-signature use will increasingly decide whether AI-generated invoices survive scrutiny or collapse under it.

What this means for professionals, firms and the middle class

Tax professionals will feel this change before many of their clients do. Their work will move away from merely perfecting the final paper and toward designing an evidence architecture that can survive challenge months later. That means asking uncomfortable questions early: who generated the working, from which system, under whose authority, using what underlying data, and can it be reproduced with the same metadata if called for on appeal? Advisers won’t need to become full-time digital forensics experts. They will, however, need working fluency in retention rules, metadata preservation, e-signature reliability, system export hygiene and when a disputed record must be escalated to an electronic-evidence specialist. In that sense, AI adoption in finance workflows may quietly create a new service line inside traditional tax and accounting practice.

The second-order effects extend beyond large corporates. Middle-class professionals running side businesses, freelancers, online sellers and family-owned exporters are precisely the users most likely to rely on cheap AI tools without any proper audit trail. For them, AI can slash clerical cost upfront and still raise compliance friction later. A reimbursement claim, GST refund issue, working-capital review, income-tax notice or vendor dispute can stall not because the invoice looks fake, but because nobody can explain its origin, edits, attachments or linkage to payment and delivery. That may widen an uncomfortable divide. Sophisticated firms will automate with controls. Smaller users may automate with screenshots and hope. So can AI-generated invoices survive scrutiny as evidence? Yes, often. But only when they are the visible surface of a disciplined record-keeping system rather than the substitute for one. In the coming cycle, provenance will beat polish.

Sources & Data Points

1. Bharatiya Sakshya Adhiniyam, 2023 (India Code PDF) — https://www.indiacode.nic.in/bitstream/123456789/20063/1/aa202347.pdf

2. Bharatiya Sakshya Adhiniyam, 2023 — Schedule certificate under section 63(4)(c) — https://upload.indiacode.nic.in/schedulefile?aid=AC_CEN_5_23_00049_2023-47_1719292804654&rid=1163

3. Information Technology Act, 2000 (updated PDF, India Code) — https://www.indiacode.nic.in/bitstream/123456789/13116/1/it_act_2000_updated.pdf

4. CGST Act, 2017 — Section 35: Accounts and other records — https://taxinformation.cbic.gov.in/content/html/tax_repository/gst/acts/2017_CGST_act/active/chapter8/section35_v1.00.html

5. CGST Rules, 2017 — Rules 56 and 57 on electronic records — https://taxinformation.cbic.gov.in/content/html/tax_repository/gst/rules/cgst_rules/documents/Central_Goods_and_Services_Tax_Rules__2017_26-December-2022.html

6. GSTN Advisory dated 27 March 2025 on 30-day time limit for e-invoice reporting for AATO ₹10 crore and above — https://einvoice2.gst.gov.in/Documents/advisory270325.pdf

7. Economic Survey 2025-26 — Chapter 3: Monetary Management and Financial Intermediation — https://www.indiabudget.gov.in/economicsurvey/doc/eschapter/echap03.pdf

8. Economic Survey 2025-26 — Chapter 14: Evolution of the AI Ecosystem in India — https://www.indiabudget.gov.in/economicsurvey/doc/eschapter/echap14.pdf

9. PIB release dated 7 March 2024 — IndiaAI Mission approval — https://www.pib.gov.in/PressReleasePage.aspx?PRID=2012375

10. Key Features of Budget 2026-27 — https://www.indiabudget.gov.in/doc/bh1.pdf